To read the full report, please download the PDF above.

Oversold commodities to withstand macro fears

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

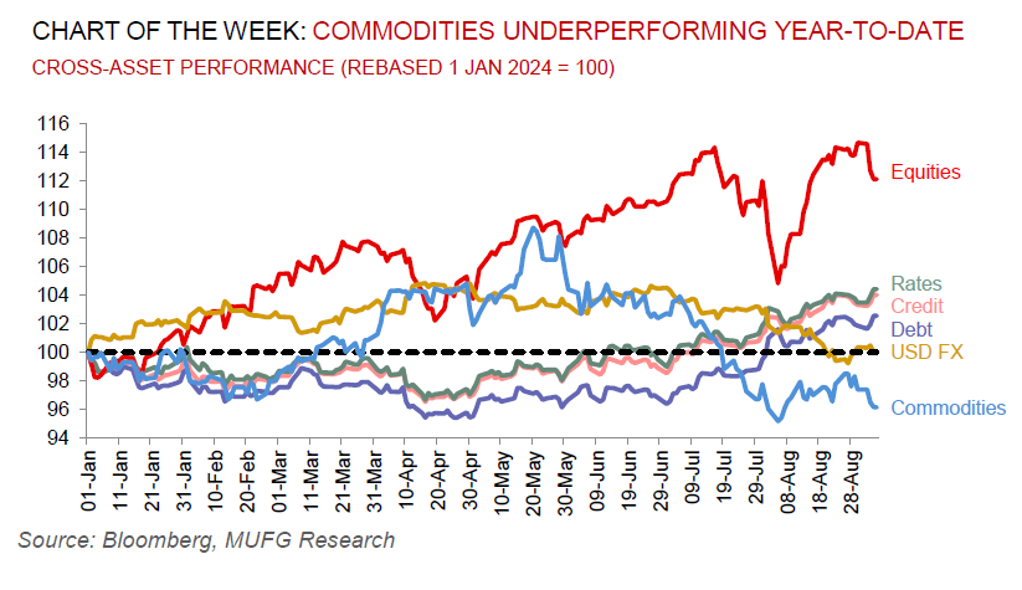

Global commodities

Commodities are flashing warning signs for the global economy. Crude oil has tanked to the lowest since June 2023. Copper’s ballooning inventories and weakness in China’s property sector is delaying the green transition demand induced structural deficits (and scarcity pricing). Diesel – the workhorse fuel of the global economy – has sank to the lowest in more than a year in Europe. Iron ore – the most China centric industrial commodity – has tumbled with a fresh torrent of down-arrow developments. Whilst investor attention is laser focused on demand-side fears, we hold conviction that macro recessionary angst – that has been driving the bulk of the selloff in recent trading sessions across the commodities complex – is overdone. Granted, the commonality in the bearish signs all point by-and-large to China, and its malaise is screaming louder following a slew of data that is raising fresh doubts whether the commodities leviathan consumer can meet its economic growth target this year. Yet, our house view calls for limited global recession risks with the macro picture still supportive of a backdrop where major central banks are laser focused on soft landing the global economy – a trajectory wherein commodities historically have proven to enjoy positive returns. With this, a softening in cyclical support to commodities leads us towards a more selective tactical approach to commodity investing. Our highest conviction views in the current uncertain environment remains long gold, short long-dated European gas, higher implied volatility in crude oil and a delay (not derailment) in copper’s scarcity pricing.

Energy

Oil bears continue to have it their way – crude prices have plummeted to near 14 month lows with concerns predominantly threefold. First, a reported truce in Libya may see its barrels come back online sooner than expected. Second, disappointments (albeit modest) in manufacturing surveys for the US ISM and the China NBS PMI are headwinds for crude demand. Third, supply heading into the final months of the year appear ample – OPEC+ is weighing the partial unwind of its production curbs from October and there are upside risks to non-OPEC+ output when assessing producers’ latest earnings reports (particularly in Canada). Whilst we acknowledge downside risks to our USD87/b year-end Brent call given heightened recession risks, elevated spare capacity, ongoing (China-led) demand apprehensions and potential trade tariffs post US elections, we believe the acute selloff is overdone with Brent crude’s 14 relative strength index (RSI) signalling a reversal from its near oversold territory.

Base metals

Base metals – led by copper, aluminium and nickel – remain well down from the May peaks owing to elevated inventories and China’s ongoing growth malaise (led by its ailing property sector). Yet, we believe that worst of the correction in base metals is now behind us and the latest uplift in prices has further room to run as the Fed embarks on its easing cycle – historically, the median price change in base metals 12 months after the first Fed cut is ~14 in non-recessionary episodes.

Precious metals

Gold remains tucked in just beneath its record with all the stars aligned for a quantum leap higher. We hold conviction in our above-consensus call for gold and forecast prices to rise to USD2,750/oz by year-end and breach the USD3,000/oz threshold in 2025, owing to its role as a geopolitical hedge of first resort in an uncertain operating environment, imminent Fed rate cuts, unprecedented central bank demand for gold, bullion-backed ETFs expanding, the risk of inflationary US policies after the elections from shocks including tariffs and rising debt apprehensions.

Bulk commodities

Iron ore is one of the largest laggards on the commodities scoreboard this week, with factory activity in China – the bulk metals biggest purchaser – contracting for a fourth consecutive month, while the latest sales readings signal a deteriorating residential tumble. This epitomises a material challenge for the country’s steel industry, wherein the Chairman of the world’s largest producer – China Baowu Steel Group – stating that conditions are like a “harsh winter” that will be “longer, colder and more difficult to endure than expected”.

Agriculture

Raw sugar is extending its gains as fires in Brazil are hampering cane crops amid the country’s worst drought in four decades that is putting fundamentals in a larger deficit than anticipated. A heat wave hitting Brazil is also adding to below-average rains that are damaging the cane and limiting mills’ ability to produce sugar.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.