To read the full report, please download the PDF above.

Oil markets remain on tenterhooks with uncertainties abound

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

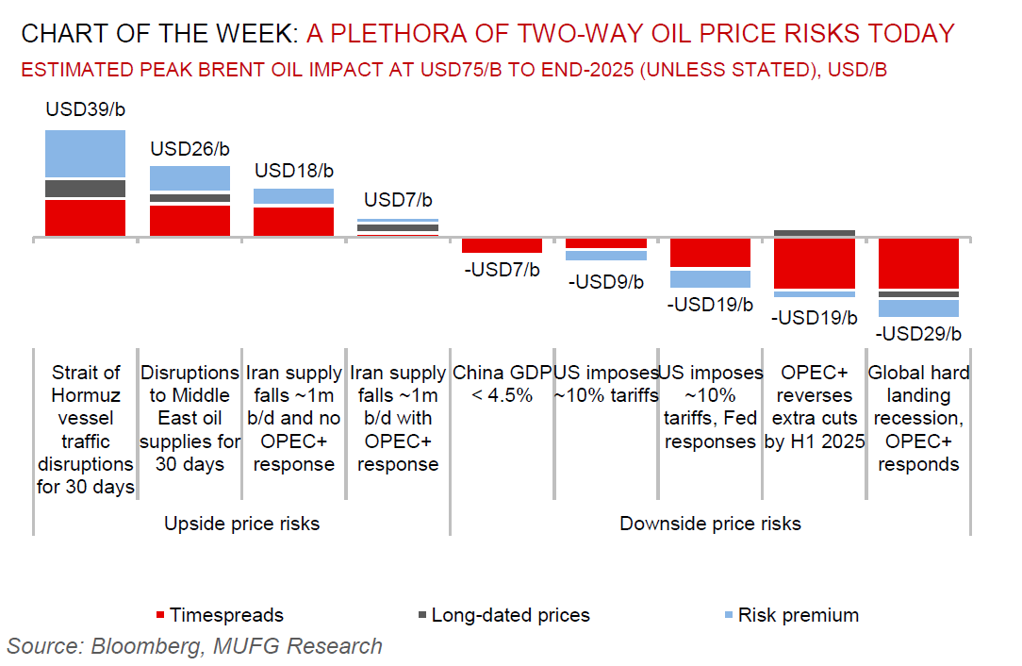

Seldom has the degree of uncertainties surrounding the oil market been as extensive as it is today. In one extreme tail risk scenario, the crisis in the Middle East may disrupt ~30% of the world’s seaborne crude oil flows and ~20% of global LNG supply – causing energy prices to skyrocket. In another scenario, OPEC+ may decide to pivot its strategy in 2025 towards a long-run equilibrium focused on strategically disciplining non-OPEC+ supply (and fortifying internal cohesion), through ramping up its barrels in what is already to be a surplus market next year – causing energy prices to plummet. Needless to state that this backdrop has caused Brent crude’s 3 month implied volatility index to spike to the highest levels in 10 months. In the immediate term, whilst the sizable ~7% advance in Brent crude following the 1 October Iranian attacks on Israel may appear significant, geopolitical risk premium gauges remain negligible for four reasons, in our view. First, OPEC+ is sitting on a substantial ~6m b/d of spare capacity that can withstand potential supply-side tightening shocks. Second, should core OPEC+ producers have an inability to export their barrels due to potential disruptions to tanker traffic in the Strait of Hormuz, there will likely be a significant and coordinated release of Strategic Petroleum Reserves (SPR) by the US, Europe and Japan to prevent a much larger sustained price spike and ensure the security of supply. Third, enhanced visibility of commercial satellite imagery allows traders to monitor risks in real-time (rather than speculating) to trade more on information – and the latest signals suggest Iran is still shipping crude oil from its highly concentrated Kharg Island export terminal. Fourth, the financial oil market is more liquid (than in the past), offering traders the optionality to purchase insurance at a rational premium, instead of taking outright directional positioning. All in, zooming out, and the recent leg-up in prices does not appear striking, but uncertainties abound.

Energy

Global oil markets are contending with competing forces. On the one hand, Middle East driven geopolitical supply-side risks is supporting prices. On the other hand, apprehensions surrounding the tepid physical market threatens to drag prices lower. Near-term, should Israel’s reprisal target Iran’s mid/upstream energy infrastructure (more significant to global markets), than its downstream assets (more significant for the domestic Iranian market), then prospects of another tit-for-tat retaliatory move by Iran may witness oil prices leapfrog higher. Meanwhile, any disruptions in gas flows from key exporters in the Middle East (Qatar, Azerbaijan, Iran, Oman, UAE, or even Israel) remains a very low likelihood but could leave European markets susceptible to price spikes more marked than that observed during the Russian invasion of Ukraine back in 2022.

Base metals

China’s largest stimulus package in years has given base metals a shot in the arm with copper, aluminium, zinc and nickel, retaining price gains over China’s Golden Week holiday, with the authorities measures being directed to reviving the property market. Looking ahead, we view that the sharp rates unwind in a soft landing environment offers good entry given late cycle driven scarcity, a tentative revival in global manufacturing and attractive returns – which now is further reinforced by a plethora of Chinese stimulus measures.

Precious metals

Gold is mildly edging lower as rhetoric from Fed policymakers reinforces the narrative that US rate cuts will not be as aggressive as previously thought. Having said that, gold’s structural strength continues to be buoyed by its role as a geopolitical hedge of first resort in an uncertain operating environment, unprecedented central bank demand for gold, surging net speculative investor positioning, an expansion in bullion-backed ETFs, the risk of inflationary US policies after the elections from shocks including tariffs and rising debt apprehensions. We hold conviction in our above-consensus call for gold and forecast prices to rise to USD2,750/oz by year-end and to breach the USD3,000/oz threshold in 2025.

Bulk commodities

Iron ore – the most China centric industrial commodity – is finding lost ground after China’s Ministry of Finance announced that it is set to hold a briefing session on 12 October which may witness a sizable fiscal stimulus package (which matters profoundly for accelerating capex spending), and in-turn supporting physical assets, like iron ore.

Agriculture

Hurricane Milton has churned towards Florida’s west coast as a Category 5 storm, with flooding and high winds expected to inflict widespread damage to the state’s citrus crops, alongside potential passthrough effects to supply chain bottlenecks.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.