To read the full report, please download the PDF above.

Tariffs, trade tensions and the outperformance of commodities

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

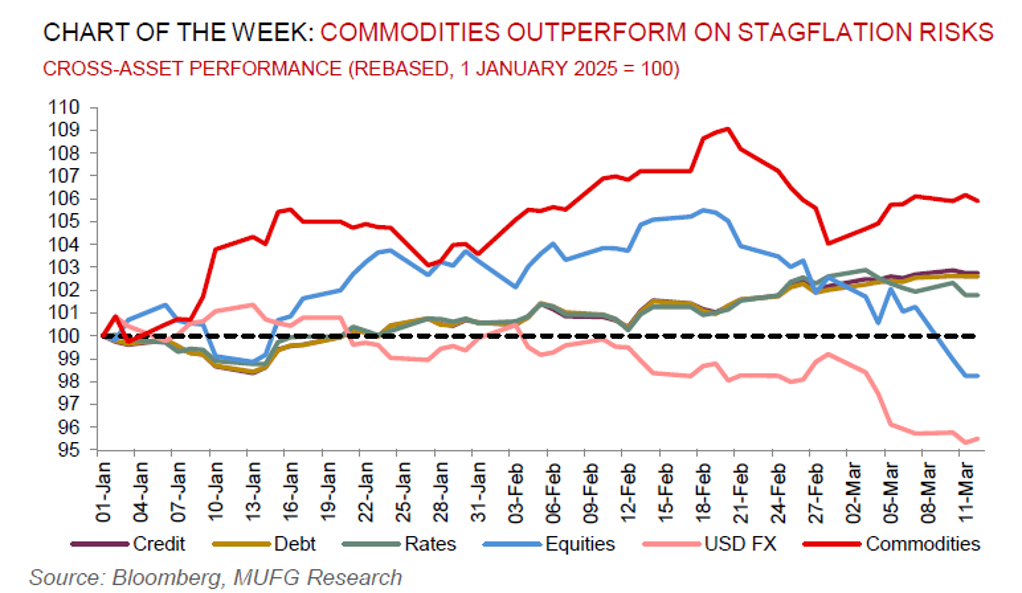

Commodity markets comprise of a multitude of overlapping narratives about where prices are going, why, and when. At the heart of the paradigm shift in the new US administration’s trade and foreign policies has been the metals complex with tariffs (and associated risks) on aluminium, steel and copper. The US’s 25% tariffs on steel and aluminium imports came into force on 12 March (after a tumultuous day on 11 March with President Trump threatened to double the metals tariffs on Canada to 50%, only to walk back when Canada agreed to drop plans to impose a surcharge on electricity sent to the US). The US tariffs has in-turned triggered a reprisal from the European Union, which launched “swift and proportionate countermeasures” on US imports, targeting goods worth up to EUR26bn. Taken together, President Trump’s move to widen his trade offensive in an effort to rewire the US economy as a global manufacturing powerhouse has rattled financial markets, startled consumers still unnerved by COVID-era inflation and fuelling recessionary angst amid mounting uncertainty for US corporates. Granted, the moves in aluminium and steel prices have been broadly muted since the 25% tariffs came into effect on 12 March (given the telegraphed tariff imposition) but the longer run consequences may breed further volatility. Looking ahead, as we have recently catalogued, as tariff threats, inflation expectations and inflation uncertainty rise further, commodities act as a critical inflation hedge as physical assets historically deliver strong real returns when inflation rises, while equity and bond real returns tend to be negative. Indeed, the US administration’s attempts to remodel the global trade order, with commodities at the centre of the doctrine, is witnessing the Bloomberg Commodities (BCOM) index outperform all major asset classes year-to-date.

Energy

After recently trading down to levels last seen in 2021, oil prices are extending recent (mild) gains on the broad risk-on sentiment post a weaker-than-expected US inflation reading as well as on the US Energy Information Administration (EIA) cutting its forecast for a global oversupply, citing the prospect of diminished flows from Iran and Venezuela – following a similar move by the International Energy Agency (IEA). Yet, today’s bearish forces in oil markets remain unresolved as trade war concerns has met recessionary angst, while OPEC+ has opted pivot strategy to defending market share by releasing additional barrels from April (in an oversupplied market) and the US administration is pushing for a Ukraine war resolution that may change the calculus on Russian sanctions (and with it higher energy flows).

Base metals

The new US administration’s 25% levies on all US imports of steel and aluminium came into effect on 12 March as part of the strategy to reshape US trade ties with the rest of the world. As we had previously documented, a shortage of domestic production in aluminium is witnessing higher physical premiums while US steel producers may gain from higher steel tariffs though low capacity utilisation could cap gains.

Precious metals

Gold and oil – two of the largest traded commodities – are usually considered in silo, but the interplay between the pair offers guidance into the global macro environment. At the current juncture, as the global trade war stacks up, it takes more barrels of crude to pay for a single ounce of gold in a disconcerting signal for global growth. The gold/oil ratio has climbed north of 41 – returning to levels last experienced during height of COVID in 2020 – with risks that the trend has further to run.

Bulk commodities

US Interior Secretary Burgum has stated that the US is contemplating emergency measures to bring back coal-fired plants that have closed and stop others from shutting. Since 2000, more than 770 individual coal-fired units have retired with coal now accounting for ~15% of US power generation today (down more than half in 2000), with an additional 120 coal-fired power plants scheduled to shut down by 2030.

Agriculture

The BCOM agri index continues to claw back losses, amid a slump in the broad US dollar and weaker oil prices. Meanwhile, the US Department of Agriculture (USDA) kept its supply and demand outlooks unchanged, trimming its projection for Brazil’s corn exports but keeping US’s shipments steady, with President Trump’s tariffs on goods from top US corn purchasers Mexico and Canada suspended until 2 April for products covered under the North America Free Trade Agreement (NAFTA).

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.