To read the full report, please download the PDF above.

Commodities’ slide signifies dual risks of a tepid China and strong dollar

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

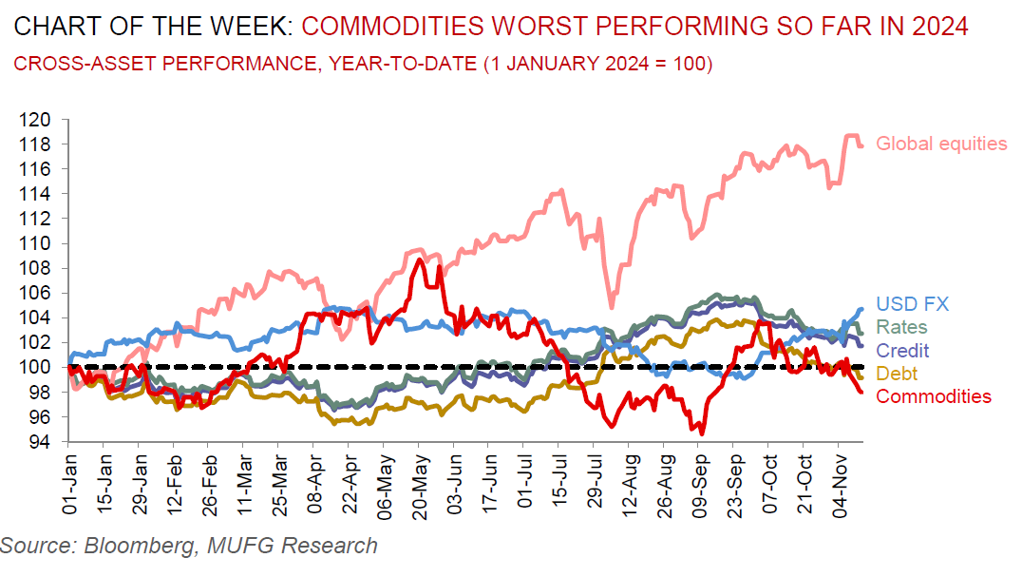

Global commodities

The destructive mood music across the commodities complex continues. Concerns about renewed US tariffs, disappointing Chinese stimulus and the surge in the US dollar, are collectively casting a long shadow, with the Bloomberg Commodities (BCOM) index down ~3% since the US elections. A lot can still change from here, likely driving volatile price action in the weeks ahead as investor expectations on growth, key macro factors and policies adjust. Specifically, we envisage two-side risks in oil (geopolitics vs looming oversupply into 2025), European natural gas (ample inventories vs LNG competition) and base metals (Chinese fiscal stimulus vs US-driven tariffs). Into year-end, we lean short oil rallies, wait to go long near-term dips in gold and await the scale as well as timing of tariffs on China to determine base metals positioning. Given such elevated volatility levels today, we reiterate our year-long constructive conviction for precious metals, led by gold, as a barometer for “fear” (geopolitical hedge of first resort in a challenged confidence era of the US dollar backed international monetary system) and “wealth” (accelerated gold accumulation by EM central banks and Asian retail demand, led by China, over concerns over economic stability and currency depreciation). Going forward, any changes to real demand and supply from trade policy measures are likely to take longer to materialise, but sentiment shifts appear to be dominating price action for now.

Energy

With apprehensions surrounding the Middle East and US elections now past their peaks, investor attention is swiftly returning to the looming 2025 oversupply in oil markets. The biggest unknown in today’s oil markets is what price level will prevent (or propel) OPEC+ from increasing (or further lowering) oil production. Whilst our base case is that the group gradually brings back a total 0.6m b/d of supply in 2025, there is a risk that OPEC+ pivots its strategy in 2025 towards a long-run equilibrium focused on strategically disciplining non-OPEC+ supply (and fortifying internal cohesion), through bringing all its 2.2m b/d barrels back to market next year. Having said that, it is equally plausible to assume further OPEC+ delays beyond its now three month production cut extension given the group’s agility and data dependent approach.

Base metals

Base metals have extended their slump on sluggish demand in China as well as the surge in the US dollar. Significant tariff escalation risks undercutting bullish fundamental base metals set up in 2025 under Trump 2.0 but sequencing of policy priorities (tax cut extensions, deregulation vs tariffs) would become much more important under a Red Wave. While a bearish reckoning on Chinese tariffs would still remain a major risk throughout a Trump 2.0 presidency, a Red Wave majority that prioritises other growth supportive initiatives first could still present a wider runway for further base metals outperformance in 2025.

Precious metals

The S&P 500 index has overtaken gold as the leading year-to-date performer, and this momentum is likely to continue as Trump-inspired US exceptionalism gains traction. The combination of higher yields and a higher US dollar is typically anathema to gold, and sure enough bullion is printing at near two month lows. Looking through the noise, gold is a natural Trump trade to hedge against bear steepening that reflects restoked inflation pressures, fiscal deficit spending concerns as well as tariff-driven geopolitical tensions. More broadly, we believe gold’s unshakable bull market remains intact, reinforced by a combination of “fear” and “wealth” dimensions into 2025.

Bulk commodities

Iron ore prices are flirting ~USD100/MT following China's policy pivot in late September, as subsequent policy announcements have supported a degree of optimism around an improvement in economic growth, while physical demand is also now on a firmer footing.

Agriculture

Soybean prices have fallen the most in more than three months as traders weighed the outlook for biofuels after US president-elect Trump announced he selected Lee Zeldin, to lead the Environmental Protection Agency (EPA) – Zeldin has declared that he will roll back regulations, raising risks surrounding the Renewable Fuel Standard (RFS) that mandates the use of biofuels made from grains.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.