To read the full report, please download the PDF above.

Policy risks reinforce gold’s status as the geopolitical hedge of first resort

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

Paradigm pivots in US policy on trade, regulation, the energy transition, migration and foreign affairs are fragmenting commodity supply chains and reinforcing gold’s safe haven demand status as the geopolitical hedge of first resort. Gold – one of the best performing commodities year-to-date, up ~15% – continues to remain our most constructive commodities conviction for the second consecutive year, serving as both a debasement hedge (where investors are looking to hedge inflation with real physical assets), and in its more traditional role as a non-yielding competitor to US treasuries and money market funds. With gold prices now surpassing our above-consensus forecasts, we mark-to-market our price levels materially higher to USD3,450/oz (from USD3,080/oz) by year-end and raise our 2026 average price level to USD3,600/oz (from USD3,280/oz). This bullish narrative is centred on our conviction of (1) a confluence of US policy uncertainty that will continue supporting investor demand, (2) fears surrounding US sovereign debt sustainability, as well as (3) central bank bullion remaining structurally higher than before the freezing of the Central Bank of Russia’s bank reserves in 2022.

Energy

Brent oil prices are oscillating in a narrow range ~USD70/b, with bullish geopolitical risk premia stemming from fading prospects for a Israel-Hamas ceasefire in the Middle East, being offset by bearish news that Russia has backed the notion to not hit energy infrastructure in Ukraine for 30 days with talks for a full ceasefire starting immediately. Meanwhile, European gas markets remain wedged between a tight prompt physical market – with European storage at ~35% full currently, less than half the fill 12 months ago – and the possibility of increased Russian gas supplies from a potential Ukraine peace deal.

Base metals

Copper is holding onto near five month highs (~USD10,000/MT) amid signals that supplies in China – the largest copper consumer – are tightening. The shortfall in Chinese supplies has witnessed copper futures pivot from contango to backwardation (signalling supply tightness).

Precious metals

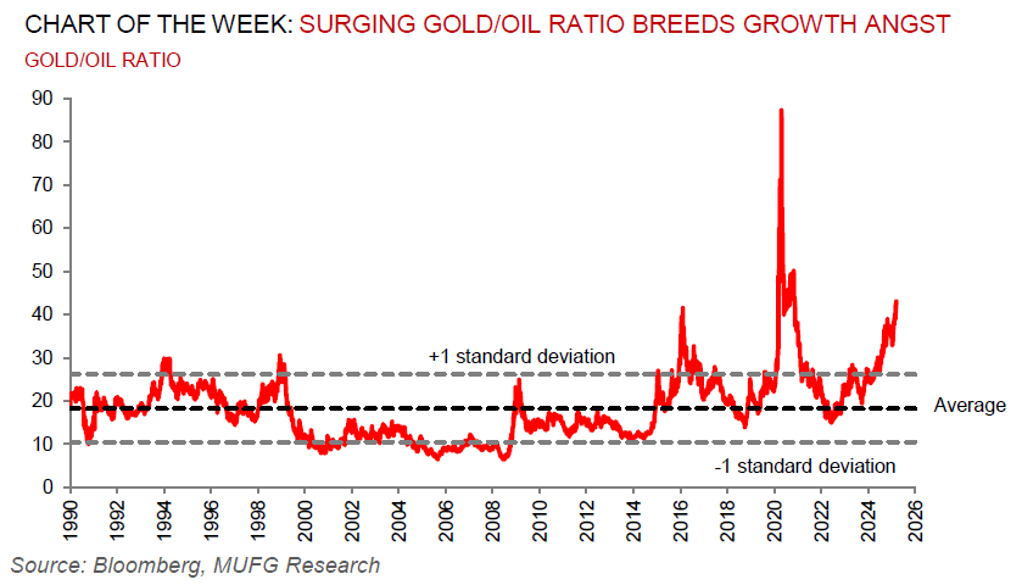

Gold continues to break record highs (see Global Commodities section), driven by haven demand amid geopolitical tensions as well as concerns over a US economic slowdown. In a disconcerting sign, the gold/oil ratio – representing the number of barrels of crude oil equivalent in price to one troy ounce of gold, with a higher ratio presaging slower global economic growth – is currently above 43, returning to levels seen during the height of COVID in 2020.

Bulk commodities

Iron ore is moving lower as China’s steel industry remains anaemic ahead of potential production cuts and as India proposes a 12% duty on some steel imports. Meanwhile, President Trump has pledged to reverse the US’s anti-fossil fuel policy and open hundreds more coal-fired power plants in a bid to make the US coal industry more competitive with China.

Agriculture

Corn spreads are extending losses as President Trump’s trade wars are clouding demand prospects even as US grain was cheaper than shipments out of Brazil and Argentina. US rainfall also supported replenish drought-sapped soils, around a month before farmers are expected to boost corn sowings from a year ago.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.