To read the full report, please download the PDF above.

Commodities riding high on Chinese stimulus but is it enough?

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

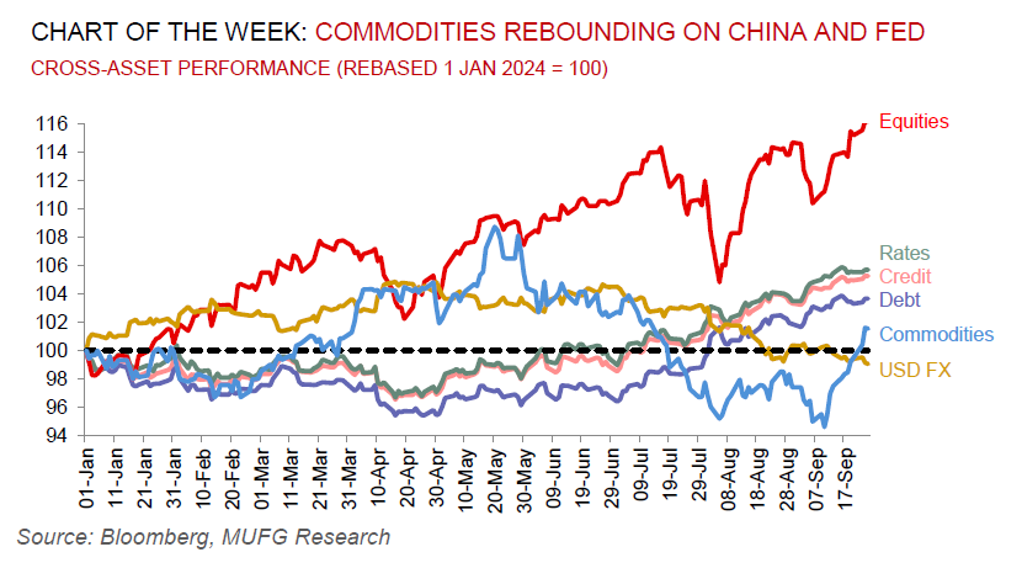

The constructive mood music in the commodities complex continues. On 24 September, the People’s Bank of China (PBoC), the National Financial Regulatory Administration (NFRA) and the China Securities Regulatory Commission (CSRC) announced a slew of stimulus measures covering three areas – monetary policy, property policy and capital markets policy. The most pertinent included a 20bp primary policy rate cut, a 50bp RRR cut and a 50bp interest rate cut on existing mortgages. The rare, simultaneous, and sizable cut of policy rates and RRR, rather unorthodox policy initiatives to support the domestic stock market, and unusual guidance on further policy easing indicates policymakers’ rising concerns about downside risks to China growth, including from the ongoing property downturn. Yet, taken together, the package seemingly does not address the large challenge facing China which at its core is malinvestment financed with excessive leverage, that creates legacy problems for the balance sheet, which is typically addressed by writing off the assets and loans. With this, there are merits in assuming that a new round of policy easing ahead to support the real economy may be on the table. Specifically from a commodities perspective, more demand-side easing measures – predominantly fiscal easing – are needed to boost domestic demand for physical assets, in our view. The +7% rally in the Bloomberg Commodities (BCOM) index since the trough on 10 September may look impressive, but global markets will await for tangible fiscal-led consumption-boosting measures from the Chinese authorities to seek further comfort that the demand-side of the equation is sustainably being addressed.

Energy

Oil is in trouble. Notwithstanding demand-side support from China’s credit bazooka, higher supply is coming into sharp focus. Easing Libyan production disruption, reports that Saudi Arabia is planning to pivot strategy from price support to regain market share by boosting output, as well as de-escalatory rhetoric from Iran amidst a flare-up in geopolitical tensions in the Middle East, is collectively pushing Brent crude to the low USD70s/b handle. Looking ahead, we stick to our constructive USD84/b Q4 2024 Brent call, with tightening in the physical market (deficits in October and November led by OPEC+ production extensions and Kazakhstan maintenance shutdowns) alongside a normalisation in the paper market (normalisation from the current depressed speculative positioning and sizable undervaluations of timespreads), driving prices higher into year-end.

Base metals

The ongoing rally in base metals – led by copper, aluminium, zinc and nickel – is now at a two month high, with the complex highly correlated to China and thus relishing in the latest raft of easing measures by the authorities. As we have frequently catalogued, we view that the sharp rates unwind in a soft landing environment offers good entry given late cycle driven scarcity, a tentative revival in global manufacturing and attractive returns – which now is further reinforced by a plethora of Chinese stimulus measures.

Precious metals

Gold is on track to accomplish a fourth quarterly rally, and there seems little on the horizon to stop its unshakable bull market. Gold’s structural strength continues to be buoyed by its role as a geopolitical hedge of first resort in an uncertain operating environment, Fed rate cuts, unprecedented central bank demand for gold, an expansion in bullion-backed ETFs, the risk of inflationary US policies after the elections from shocks including tariffs and rising debt apprehensions. We hold conviction in our above-consensus call for gold and forecast prices to rise to USD2,750/oz by year-end and to breach the USD3,000/oz threshold in 2025.

Bulk commodities

Iron ore is enjoying an acute rebound as China’s policymakers shored up efforts to address the ailing property sector this week – and may continue to find support as prices hover close to the cost curve whilst gains may also be realised from seasonal support via the steel restock cycle.

Agriculture

Palm oil is headed for the largest run of gains in more than eight months on expectations for higher demand as supply tightens with certain central Asian countries looking to boost stockpiles ahead of the upcoming festive season.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.