To read the full report, please download the PDF above.

Commodity investors are losing patience on the Fed’s snail pace rates move

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

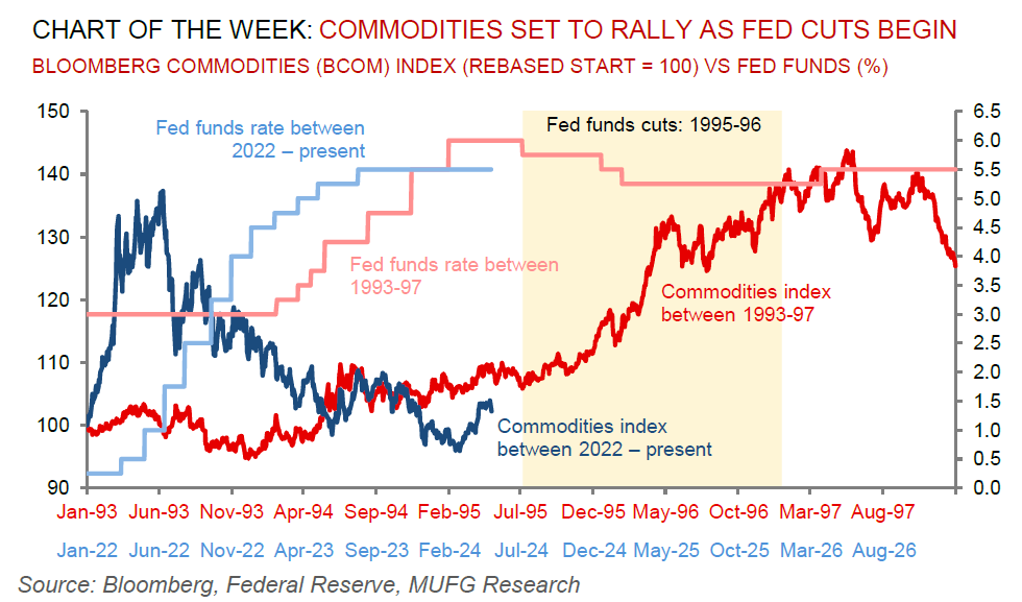

Impatient commodity investors have begun to cut their risk appetite despite the Fed’s calls for patience on rate cuts. Outflows from commodity ETFs, underperforming energy equities and falling net long futures positions in oil are implying apprehensions over the impact of higher-for-longer rates on commodities demand. Outflows of USD2.1bn from commodities were recorded over the last three months to 26 June – a clear signal that traders are distancing themselves from the energy, metals and agricultural complex. Yet, commodities have historically proven to generate positive returns going into the first Fed cut and after. With our US rates strategist pricing in the first Fed cut in September, we hold conviction that the recent pullback in commodity investor flows is just that – a pullback. As we enter the third quarter on 2024 and draw closer to Fed cuts, investor appetite for the commodities complex is set to rebound, with the strongest gains primed to be within energy (high cyclicality) and precious metals (correlation between gold prices and US real yields).

Energy

Brent oil remains in a tight USD84-86/b range but looks primed to challenge USD90/b in Q3 2024 as the market mood music gravitationally turns constructive, underscored by fundamentals mired in deficit (demand above supply), that’s reinforced by a backwardated futures curve (signalling supply tightness). US-led robust summer travelling demand continues to support Brent crude, and with it, both (i) US gasoline that’s edging closer to the USD4/gallon threshold (hampering the incumbent president ahead of US elections in November); and (ii) global jet demand which has now reached a post-COVID high. What’s more, geopolitical supply-side tensions continue to remain on the market’s radar, given an intensification of Houthi attacks on Red Sea vessels as well as drone attacks on Russia oil infrastructure. Meanwhile, the reverberations of the latest EU and UK package of sanctions on the transhipment (re-exports) ban of Russian LNG may be muted for global gas markets given such volumes are negligible in quantum (~4% of total European LNG imports).

Base metals

Copper prices have fallen to the lowest level in more than two months – extending a slide from May’s all-time high – as traders digest a slew of tepid Chinese data. We continue to expect copper to remain supportive (copper is our most bullish long-term structural conviction), as the market remains in a structural deficit on the back of an improvement in global manufacturing activity, rapid decarbonisation and a constrained mine supply environment.

Precious metals

Gold prices are under pressure following hawkish comments from Fed governor Bowman who said she sees a number of upside risks to the inflation outlook, and reiterated the need to keep borrowing costs elevated for some time (higher rates are negative for non-interest bearing bullion). We maintain our 2024 commodities outlook call that gold is our most favourite trade this year on a trifecta of (eventual) Fed cuts, (still) supportive central bank demand and bullion’s role as the geopolitical hedge of last resort.

Bulk commodities

Iron ore – the most China centric industrial commodity – is steadying as traders assess gradual progress in China’s efforts to ease the property market crisis. The steel-making staple is close to ending what’s been a dismal H1 2024 on a fittingly sombre note, with prices just north of USD100/MT (down -26% year-to-date), driven by a seaborne market that’s in surplus.

Agriculture

Corn prices have climbed to a seven month high in China as heavy rain (in parts of Heilonggjian province – top producer of corn and soybeans), as well as drier conditions (in wheat-intensive provinces of Henan and Shandong) prompts concerns over supply. Elsewhere, corn prices in Chicago are easing on a strengthening outlook for US stockpiles and improving weather in the Midwest.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.