To read the full report, please download the PDF above.

(Gold)en hedge for US elections

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

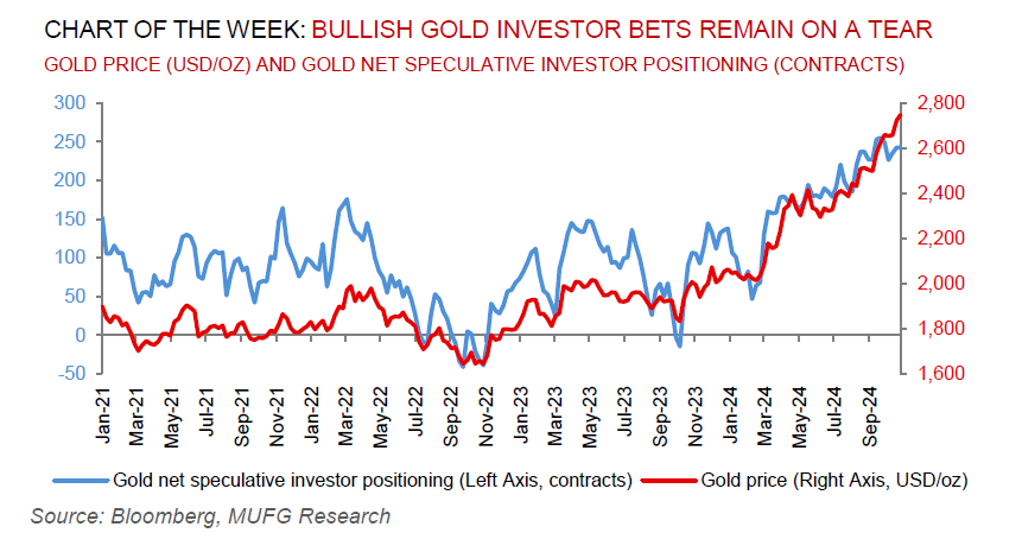

The unshakable bull market in gold – up more than 30% year-to-date – remains our most favoured hedge against volatility-driven shifts in fiscal, regulatory, trade, monetary and foreign policy of US presidential election outcomes. Gold is a natural Trump trade to hedge against bear steepening that reflects persistent inflation, persistent high debt and deficit spending concerns. Meanwhile, a Harris administration will see increase government spending on social programmes, infrastructure and energy transition initiative which risks widening the deficit, weakening the US dollar and increase inflation expectations. Looking ahead, the breakdown in gold’s usual catalysts – real rates, growth expectations and the US dollar – to flows and the prices, suggests that a new framework is needed to understand the path from here. In this context, we believe viewing gold as a barometer for “fear” (short-to-medium term driver) and “wealth” (long-term driver) is useful. The fear component can be cyclical (2008 Great Financial Crisis and 2020 COVID) – or more structural, where confidence in the US dollar backed international monetary system is challenged. The wealth component captures accelerated gold accumulation by both (i) EM central banks that has been catalysed by sanctions apprehensions; and (ii) Asian retail demand, led by China, over concerns over economic stability and currency depreciation. Succinctly, it is resolutely hard to come up with a bearish view to gold’s “all-weather” characteristics being a central beneficiary of the Fed cutting cycle, central bank buying, debt concerns, and its role the geopolitical hedge of first resort. We bring forward our already above-consensus gold forecasts levels by one quarter, to breach the USD3,000/oz threshold by Q3 2025.

Energy

Brent crude has collapsed ~5% thus far this week with Israel’s targeted strikes on 26 October avoiding Iran’s energy infrastructure – ebbing what has been left in the geopolitical risk premium built in prices since the Iranian strikes on Israeli territory on 1 October. Whilst there may be value in long oil positions given portfolio hedging benefits against lingering geopolitical shocks – especially during the lame duck US presidential period (between US election day in November and inauguration day in January 2025) – investor attention has markedly shifted back to the bearish prices risks of significant oversupply in 2025. Meanwhile, European natural gas (TTF) prices are hovering near 10 month highs, owing to an increasing call on LNG imports over the winter period given stronger Asian competition as well as delays in US LNG supply coming online.

Base metals

Base metals are finding moderate support with reports that China is considering approving the issuance of CNY10tn (USD1.4tn) in fresh debt via special treasury and local government bonds – a fiscal package that may be further bolstered if candidate Trump is re-elected. We see some upside risks to our fundamental price impact estimates based on the historical sensitivity of base metals demand to GDP as some stimulus measures may aim to accelerate the energy transition.

Precious metals

The Bloomberg precious metals (BCOMPR) index has continued its year-to-date rally in October, gaining ~6% despite higher US yields and a stronger US dollar. The continued outperformance in gold and silver comes as markets price in greater odds of a Trump presidency and possible Republican sweep, fuelling precious metals length as a hedge against the potential for amplified US shifts in fiscal, regulatory, trade, monetary and foreign policy.

Bulk commodities

Iron ore has retreated from the highest in two weeks on rising port inventories in China that remain ~40% higher than this time last year, driven by elevated arrivals. With surging shipments from India and Australian volumes in recovery, we expect port stocks to rise further unless prices drop below USD90/MT, in our view, which could remove some Indian supply from the market, and allow fundamentals to start rebalancing.

Agriculture

Wheat prices have risen after the US Department of Agriculture (USDA) rated the American crop at historically low levels due to drought. The USDA stated that only 38% of US winter wheat was rated “good or excellent” – the lowest since 2022 and second worst level in USDA data back to 1987.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.