Please download PDF using the link above for the full report

Our macroeconomic baseline for Asia FXs in Q3 and the rest of 2024 is largely unchanged from Q2, with GDP growth for most Asian economies slightly higher in 2024 than in 2023. We continue to expect growth divergence across Asia economies in the second half of the year. India, Indonesia, Thailand, and Vietnam, will experience moderately stronger growth rates in H2 compared with H1 2024, while economies, such as China, South Korea, Malaysia and Taiwan will likely experience modest deceleration in GDP growth in H2.

Broadly speaking, most Asian economies’ GDP growth in H2 will be below their respective long-term average (2015-2019), except India and Thailand. India’s economic growth is likely to accelerate in H2 after a modest election-driven slowdown in H1, benefiting from policy continuity post the elections with a relatively strong coalition government in power. We expect the Thai economy to accelerate to 3.9%yoy in H2 after a slow growth of 1.9%yoy in H1, due to normalisation of fiscal disbursement, tourism, and a better outlook for goods exports. We continue to expect 5.0%yoy China GDP in 2024, with high sequential growth in Q1 and gradual recovery in property activity and domestic demand implying a slower H2 yoy GDP growth compared with H1.

While Asia’s inflation is projected to decline further, a later-than-expected start of Fed’s policy rate cut will contribute to slower monetary policy rate normalization in some Asian economies. China, Philippines, South Korea and Taiwan are projected to start rate cuts in H2 2024, together with India and Indonesia from Q1 2025. In addition to macro background of domestic and external economy, country-specific idiosyncratic factors also play key roles in Asian FX movements, along with key themes like the Fed’s policy, US dollar, geopolitical risks, AI-investment and etc.

For H2, the start and anticipation of Fed’s policy cut in September is likely to provide marginal help on Asia’s yield spread with US. We expect the happening of a turning point for Asia FXs in H2, with a potential weakness of US dollar (after its sustained period of strength) to eventually give some breather room for Asia currencies.

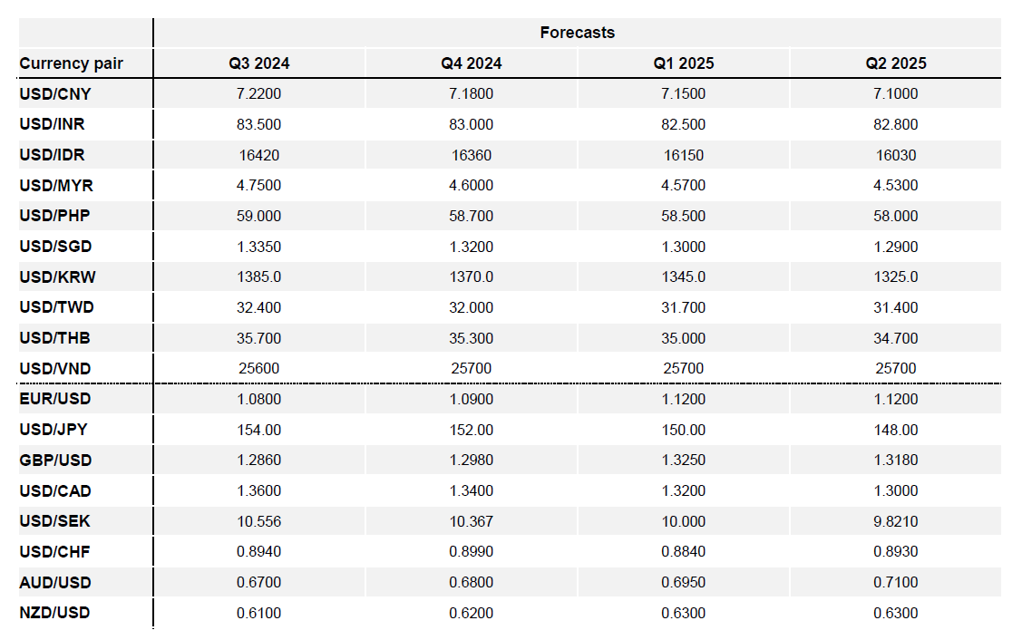

For H2, our top picks are THB, SGD and MYR, benefitting respectively from improving outlook for Thai growth and current account, Singapore’s tight MAS policy, and Malaysia’s current account surplus and a prolonged BNM pause. Among Asian peers, KRW and TWD are likely to benefit most from continued AI-investment theme. We expect USD/CNY to reach 7.18 by year-end, due to potentially improving sentiment on a clearer picture of China’s gradual and more stable economic recovery ahead, while INR is expected to strengthen mildly in H2 as well, with strong capital inflows, policy continuity, and good macro stability helping to fund a wider current account deficit.

More details are enclosed in this file.

Hope it helps,

GMR Asia