Ahead Today

G3: US initial jobless claims

Asia: Philippines Q1 GDP, BNM policy rate decision, Taiwan CPI

Market Highlights

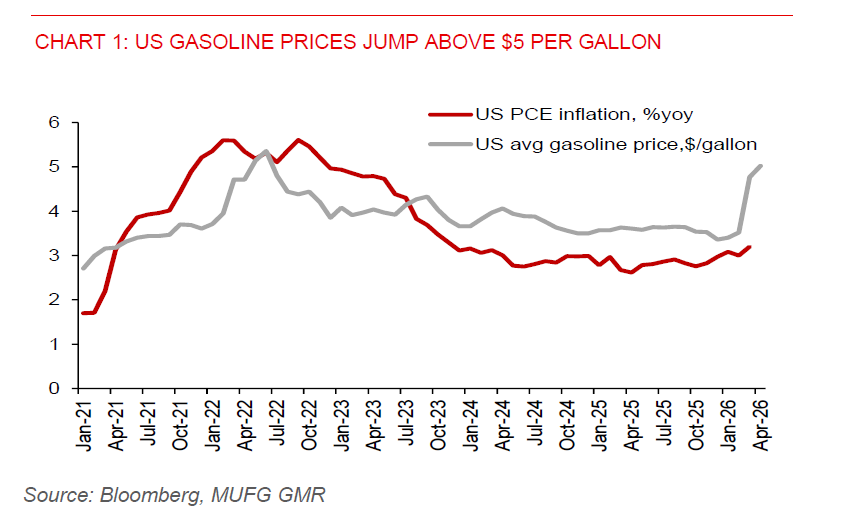

Signs continue to point to limited appetite for further escalation in the Middle East. The US has reportedly presented Iran with a memorandum of understanding aimed at de escalating tensions and gradually reopening the Strait of Hormuz. The proposed deal would involve Iran committing to a moratorium on nuclear enrichment in exchange for US sanctions relief. Domestic constraints matter: with US midterm elections approaching, average gasoline prices having surged above USD5/gallon, and US 2-year yields near 3.9% raising debt servicing costs, the US appears to have incentives to contain the Iran conflict.

The dollar softened, with DXY retesting support near 97.60, while US 10-year yields fell around 8bp to 4.35%. Brent prices have fallen back to around the $100/bbl level and is down nearly 20% from its 30 April intraday high of USD126.41/bbl. Meanwhile, the S&P 500 pushed to new highs, helping to contain the dollar decline.

On the data front, April ADP employment rose to +109k from +61k in March. But the latest ISM services survey is more concerning. Prices paid rose to a three year high, while services employment stayed in contraction. From a policy standpoint, this creates a dilemma for policymakers. We think the Fed is more likely to delay on rate cuts rather than to pivot back to rate hikes. And should there be meaningful deterioration in labour market conditions, monetary policy may err on the side of easing over the next 12 months – an outcome that remains underpriced by markets.

Asian currencies strengthened against the dollar, led by KRW (+1.8%) and THB (+1.5%). Further de-escalation in the Middle East, such as Iran accepting the US proposed deal and a gradual reopening of the Strait of Hormuz, could continue to support gains in Asia FX. We maintain a constructive view on CNY, MYR, and SGD, where both fundamentals and technicals point to further upside against the dollar.

The ringgit should continue to play catch up with CNY strength. Today’s BNM policy meeting is likely to be a non-event, with the central bank expected to keep the policy rate unchanged at 2.75%.

By contrast, we remain cautious on further USDIDR upside. Bank Indonesia has stepped up stabilisation efforts, including tightening limits on USD purchases without underlying documents to $25,000 from $50,000 previously. This will help to curb speculative activity. In addition, we see markets underpricing the upswing in non- energy commodity prices, which should provide an additional tailwind for Indonesia’s terms of trade.