Ahead Today

G3: US Richmond Fed Index

Asia: China FDI YTD

Market Highlights

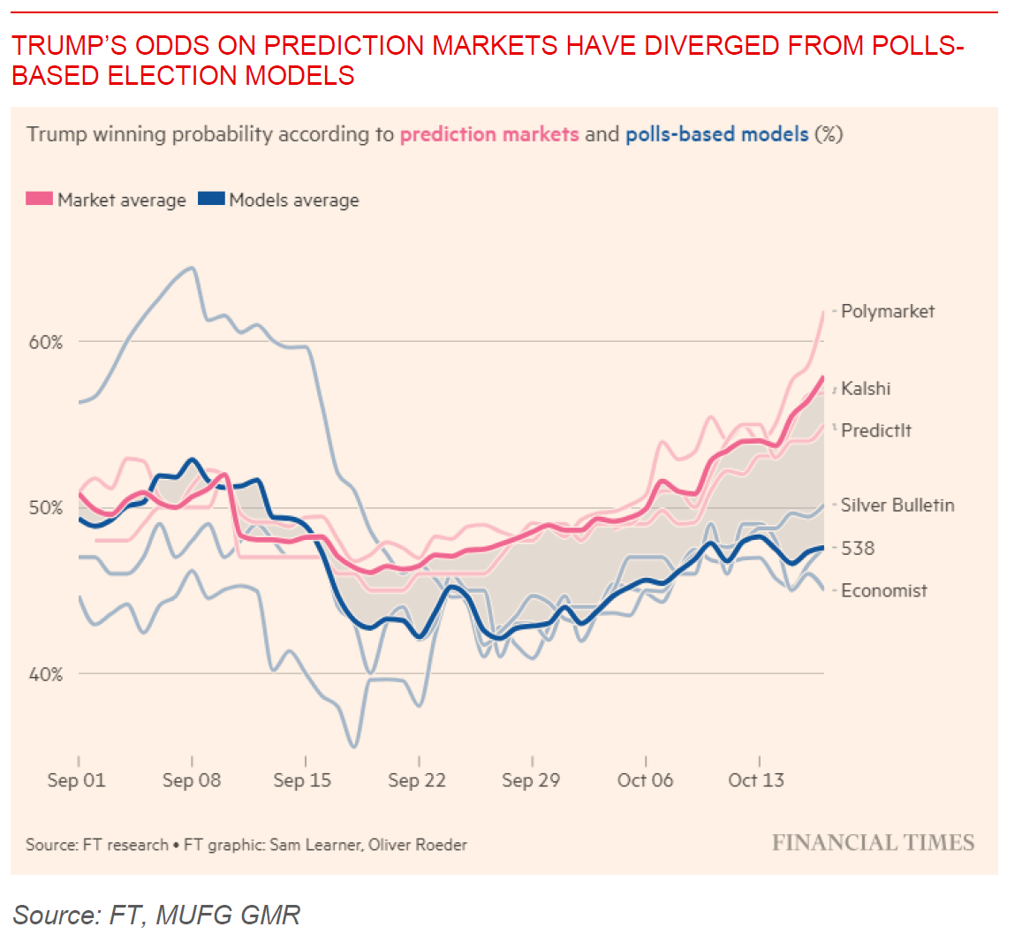

The Dollar strengthened, US 10-year yields rose, while risk sentiment took a beating as election risks dominated markets. US Prediction Markets including Polymarket, Kalshi, and PredictIt have further raised the implied probability of Trump winning to more than 60%, while also raising the probability of a Red Sweep further as well. All developments had a clear effect on US rates with the 10-year yield rising closer to 4.18% coupled with a steeper yield curve as markets tried to look forward towards possible policy shifts from a 2nd Trump administration. While the trend especially in swing states have been clearly in Trump’s favour since September, the magnitude is still clouded with significant uncertainty. In particular, polls-based election models have diverged from prediction markets assigning a lower even if rising probability of a Trump victory, with the Financial Times reporting that a small group of anonymous traders have propelled the dramatic surge in Trump’s perceived chances in prediction markets.

Regional FX

Asian FX markets were mixed to weaker with a stronger Dollar overnight. KRW (-0.9%), THB (-0.6%) and SGD (-0.5%) underperforming. Beyond US rates and Fed speak, Asian currencies were to some extent impacted by the weakness in the Japanese Yen. JPY has been weighed down by latest election polls showing support for Japanese Prime Minister Ishiba’s ruling coalition softening further, indicating the possibility that the vote may result in a weakened and unstable administration. Failure to win a clear mandate could complicate both the path of policy initiatives and also perhaps the government’s support for further BOJ rate hikes. Meanwhile, Chinese authorities cut both the 1-year and 5-year loan prime rate by a larger than expected 25bps. Nonetheless, these moves should be viewed in context of the 20bps 7-day reverse repo rate cut that was already announced in September, and as such is not signaling incremental further monetary policy easing. Malaysia’s 3Q GDP came in stronger than expected at 5.3%yoy (from 5.9%yoy the previous quarter) and compared with consensus expectations for a 5.1%yoy rise. The preliminary details suggest that growth was boosted in particular by the manufacturing sector and presumably in the semiconductor and electronics space.