Ahead Today

G3: US initial jobless claims

Asia: BSP and BI policy rate decisions

Market Highlights

Oil prices have declined, but US yields have not, with the higher-for-longer US rate backdrop remaining a constraint on regional FX performance.

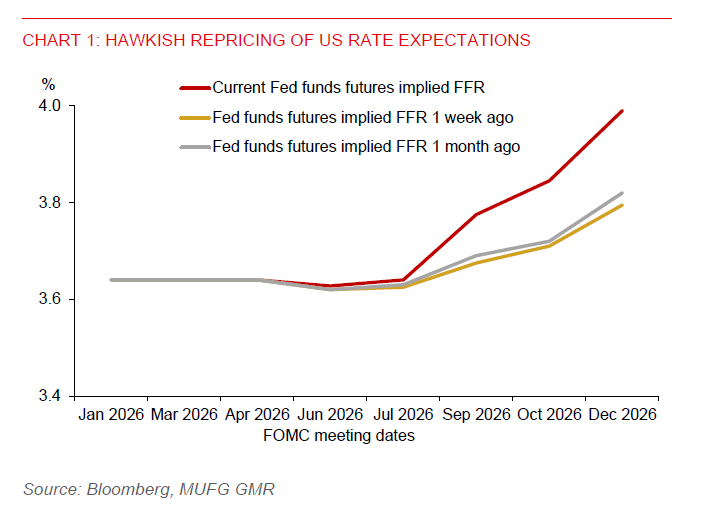

As widely expected, the Fed held the policy rate. However, new Fed Chair Kevin Warsh delivered a hawkish message, emphasizing that the Fed will not tolerate elevated inflation. This effectively takes rate cuts off the table for now. Fed funds futures have repriced further in a hawkish direction and now fully price in a rate hike by October. Reflecting this shift, US 2-year yields rose 13bps to 4.18%. The DXY gained 0.6% to test the 100 level, with momentum indicators continuing to favour USD strength.

Incoming US data has also supported the higher-for-longer narrative. Retail sales rose 0.9%mom in May (vs. 0.6% market consensus), accelerating from 0.5% in April. Core retail sales (ex-autos and gas) held firm at 0.5%mom, exceeding expectations of 0.3%. The resilience in US consumption further underpins the Fed’s reluctance to ease policy.

In FX markets, the yen weakened modestly as higher US yields reinforced its structural carry disadvantage. USDSGD rose 0.5% to around 1.29, tracking broader USD strength. For Asia FX, the decline in oil prices provides partial relief. A higher-for-longer US rates environment is a headwind, particularly for low-yielding currencies.

While the carry appeal of the Indonesian rupiah and Philippine peso has improved following recent policy rate hikes, upside is likely to remain capped by global uncertainties and USD strength. For IDR specifically, near-term risks are elevated ahead of key MSCI events, including the market accessibility review on 18 June and classification review on 23 June, following earlier concerns about investability in Indonesian equities.

While momentum broadly favours further upside in USD/Asia pairs, CNY stands out as an exception. USDCNY momentum remains biased towards further CNY appreciation, supported by a fresh set of financial policy measures. These include adjustments to the operational policy rate framework (centered on the 7-day reverse repo ±25bps), the introduction of overnight reverse repos in the open market operation tools, the creation of a repo facility for foreign central banks, and a pilot scheme for CNH trading in the Shanghai Free Trade Zone.

Key highlights today focus on BSP and BI policy decisions.

In Indonesia, Bank Indonesia already delivered an off-cycle rate hike earlier this month. We expect BI to pause at today’s meeting to assess the effectiveness of its recent FX support measures. That said, the policy bias remains tilted toward further tightening, with a clear focus on stabilizing the rupiah.

In the Philippines, the policy stance is similarly skewed toward additional tightening, as BSP is likely to respond to inflation pressures.