Ahead Today

G3: University of Michigan sentiment index, Germany IFO business climate

Asia: Indonesia Q1 BOP, Malaysia foreign reserves

Market Highlights

Talks between the US and Iran remain ongoing, with Iran’s uranium stockpile and control over the Strait of Hormuz emerging as key sticking points. Iran appears to be insisting on retaining its uranium stockpile domestically, while also proposing a toll system for transit through the Hormuz strait. It remains unclear whether a breakthrough is imminent. Nonetheless, tentative optimism around a potential agreement has supported risk sentiment, with the S&P 500 closing higher and Brent crude edging lower.

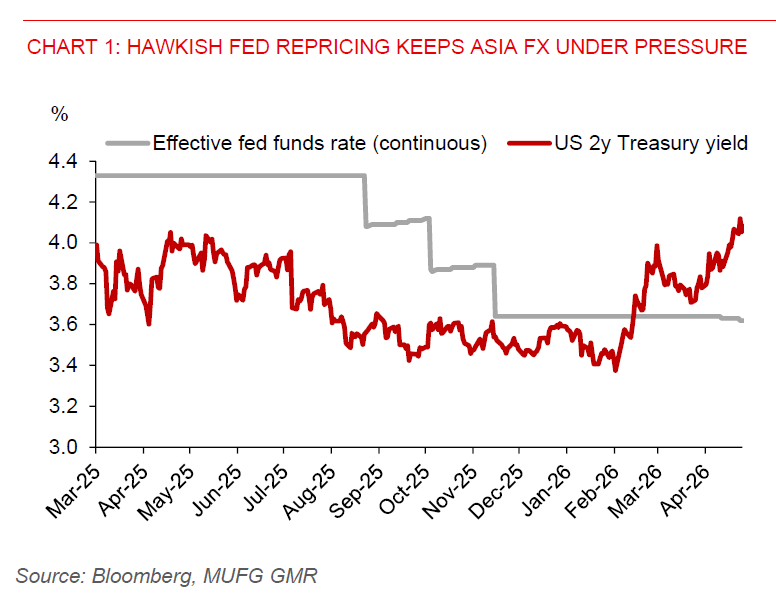

That said, US yields stay elevated. The 2-year is holding above 4%, while the 10-year has risen by nearly 20bps to around 4.57% month-to-date. Markets have also shifted towards pricing a higher probability of Fed tightening by year-end. This yield backdrop continues to underpin a carry-driven bid for the USD, with DXY firming above the 99.00 level. US macro data also remains supportive of the dollar. The 4-week average of initial jobless claims stayed low at around 202.5k as of mid-May, while the S&P Global US composite PMI steadied at 51.7 in May, remaining in expansion territory.

Meanwhile, Japan’s core inflation rate was 1.4%yoy in April, down from 1.8%yoy in March and below market consensus of 1.7%. This suggests a slow BOJ rate normalization path, while elevated US yields continue to keep the yen under pressure.

Across the rest of Asia, elevated US yields and hawkish Fed repricing are likely to continue weighing on regional FX in the near term. While Brent has eased, prices remain above $100/bbl, keeping pressure on oil import bills and sustaining inflation risks. Policy measures may provide intermittent support, but global uncertainties and higher US yields remain the dominant drivers of regional FX weakness.

INR gained 0.6% against the US dollar yesterday on the back of RBI support, with policymakers reportedly considering rate hikes to stabilize the currency, though the rupee remains significantly weaker year-to-date. The Indonesian rupiah is also drawing policy support following the recent 50bps BI rate hike. However, sentiment remains fragile amid persistent concerns over government policy direction, including recent moves to assert greater control over commodity exports. External headwinds and domestic policy uncertainty continue to cloud the outlook for the rupiah, although USDIDR appears to be in overbought territory in the near term.