Ahead Today

G3: US Non-Farm Payrolls

Asia: South Korea Impeachment Trial

Market Highlights

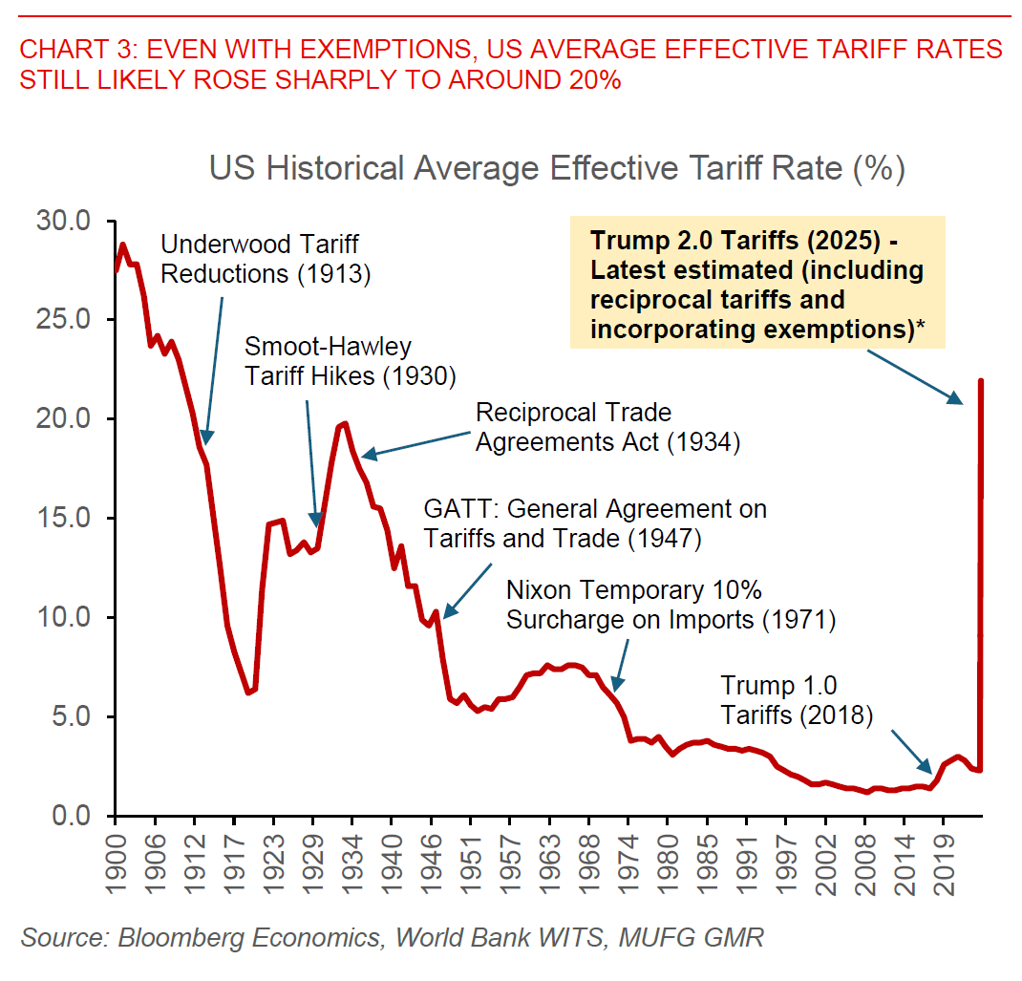

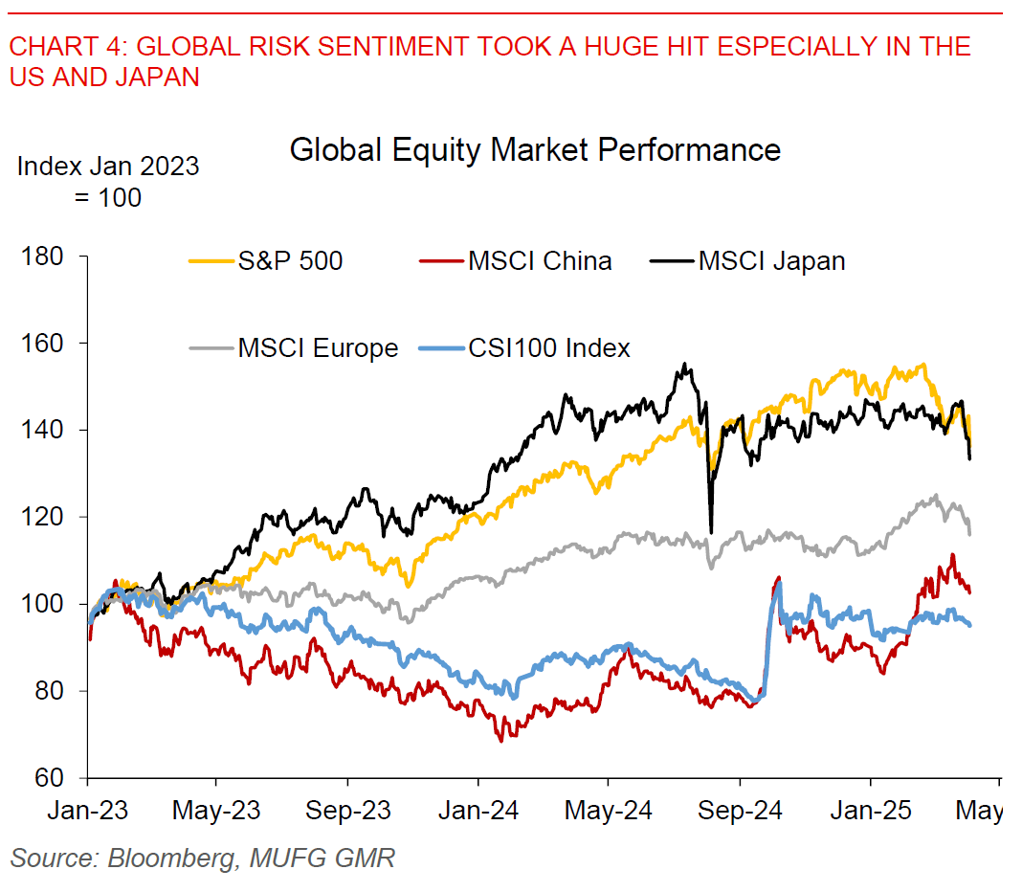

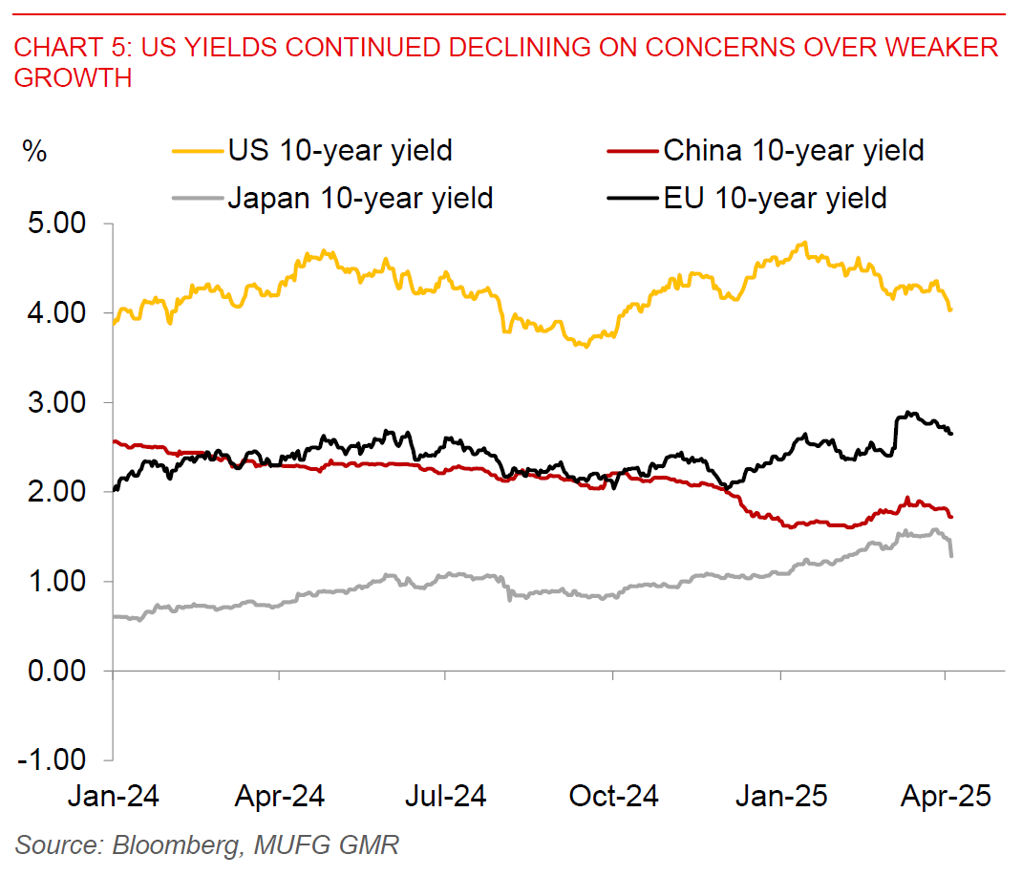

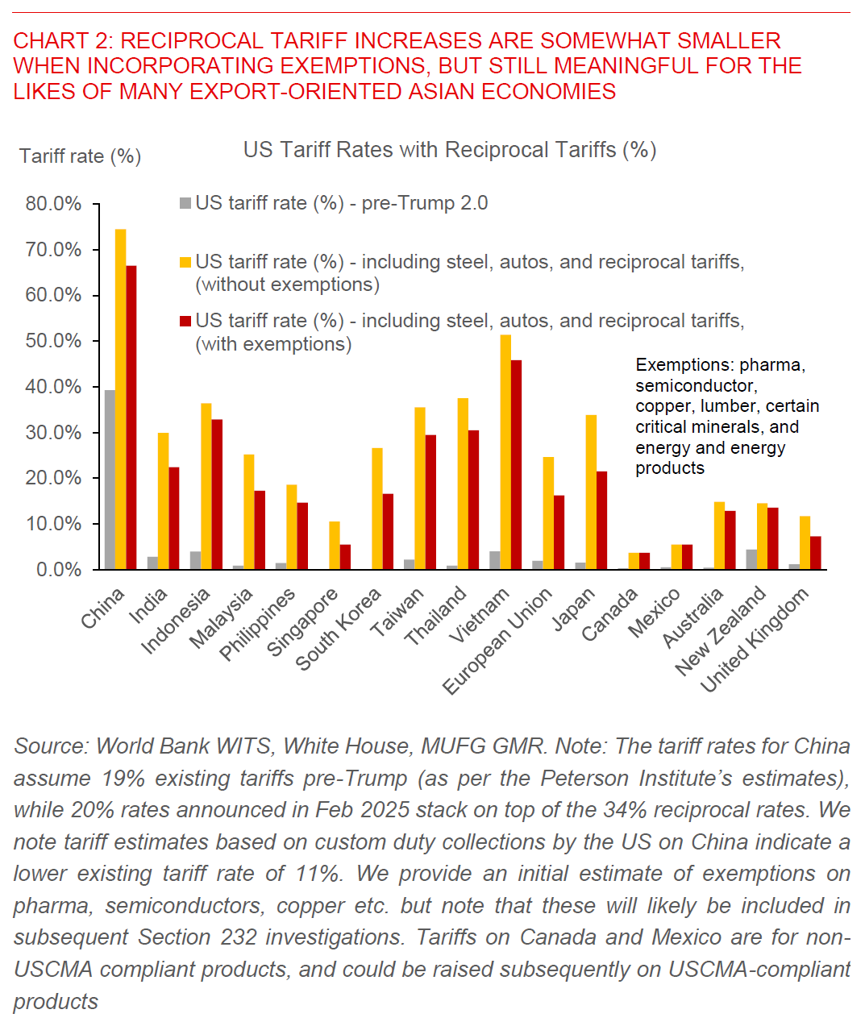

Post what was the largest tariff hike by the US since the 1930s Smoot-Hawley tariffs, markets made massive moves across the board including in FX (see Asia FX Talk – Reciprocal tariffs – largest tariff hikes since 1930s). Risk sentiment took a significant hit with the S&P500 down close to 5%, the NASDAQ down 6%, while European and Asian equities all fell more than 3%. In Asia, equity sentiment was the worst in Vietnam, and for good reasons given the much sharper than expected reciprocal tariff increase of 46%. Meanwhile, US 10-year yields fell further by 10bps to 4% with growth concerns dominating, while Asia local currency rates were generally dragged lower as well. Markets moved to price close to 4 Fed rate cuts by the end of 2025 from 3 previously.

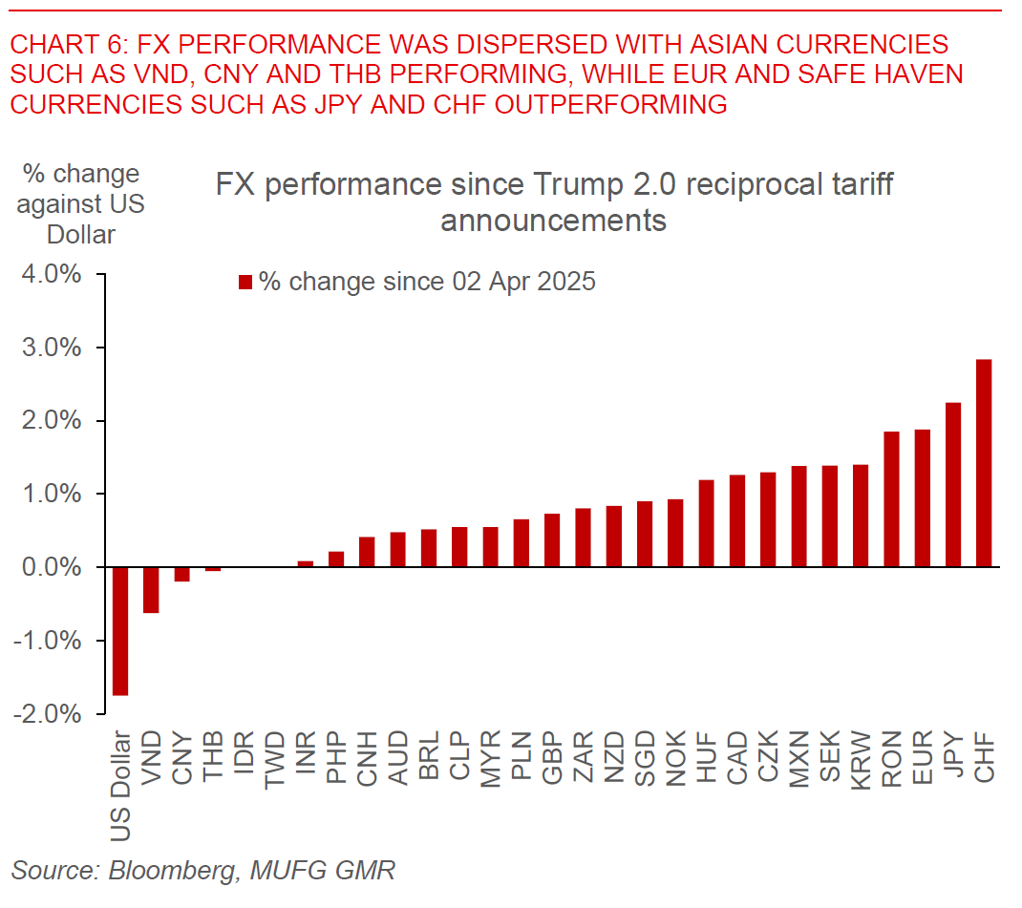

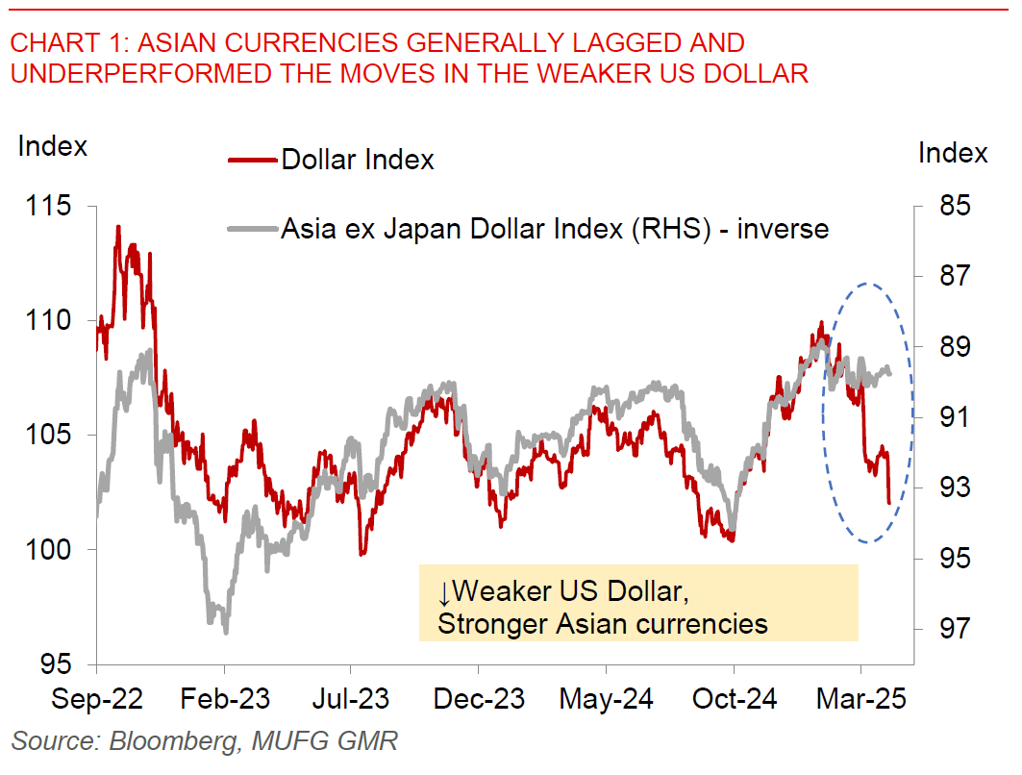

In FX, the moves were equally big, although we note dispersion of outcomes with Asia generally underperforming G10 and to some extent Latam. The Dollar weakened by 1.7% led by EUR, and strength in safe haven currencies such as JPY and CHF. Asian currencies generally lagged the moves in G10 with VND, CNH, THB underperforming, but eventually the weaker Dollar trend helped to cap losses in Asian FX.

These moves together with the underperformance in Asia FX were certainly for good reasons. As we pointed out in our report, and also in line with our G10 team’s longer-term view on Dollar weakness (see Asia FX Talk – Reciprocal tariffs – largest tariff hikes since 1930s), FX is a relative price and certainly concerns around US exceptionalism and weaker US growth is dominating right now. The key for us in Asia moving forward is whether the left hand-side of the US Dollar smile – in other words concerns around global growth spilling over significantly to Asia – starts to dominate yield differentials between the US and Asia (see our framework here on drivers of Asia currencies: Asia FX – The impact of Fed’s easing cycle and more). With the way equity markets are moving, and more importantly the significant tariff increases by the US especially on Asia (even after taking exemptions into account), we do think that Asia’s growth will most certainly take a hit moving forward.

Regional FX

Looking ahead, markets will focus on the US non-farm payrolls print to gauge whether the US labour market managed to dodge any negative impact from DOGE job cuts. Meanwhile, we will also have the South Korea’s Constitutional Court ruling on president Yoon Suk Yeol’s impeachment later today. If the Court upholds the impeachment, this will likely trigger a snap presidential election likely in early June.