Ahead Today

G3: Eurozone Manufacturing PMI, US Jolts Job Openings, US ISM Manufacturing, US ISM Prices Paid

Asia: Asia PMIs, China Caixin Manufacturing PMI

Market Highlights

President Trump is slated to announce his signature reciprocal tariff plan on 2 April (3 April Asia time), in what could shape up to be the biggest tariff hike by the United States since the 1930s Smoot-Hawley tariff increases. The announcement – on what’s termed as “Liberation Day” - will feature “country-based” tariffs with “no exemptions at this time”, according to comments yesterday from the White House Press Secretary. Meanwhile, sector-based duties such as on for pharmaceuticals and semiconductors will not feature, at least for the time being.

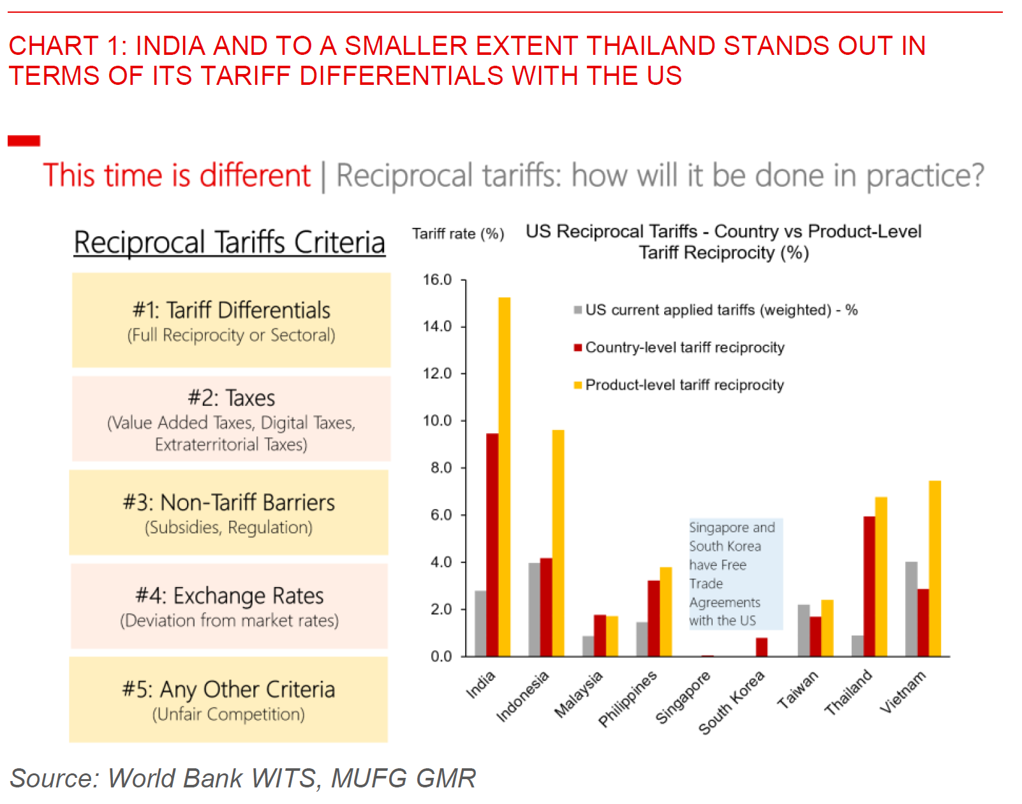

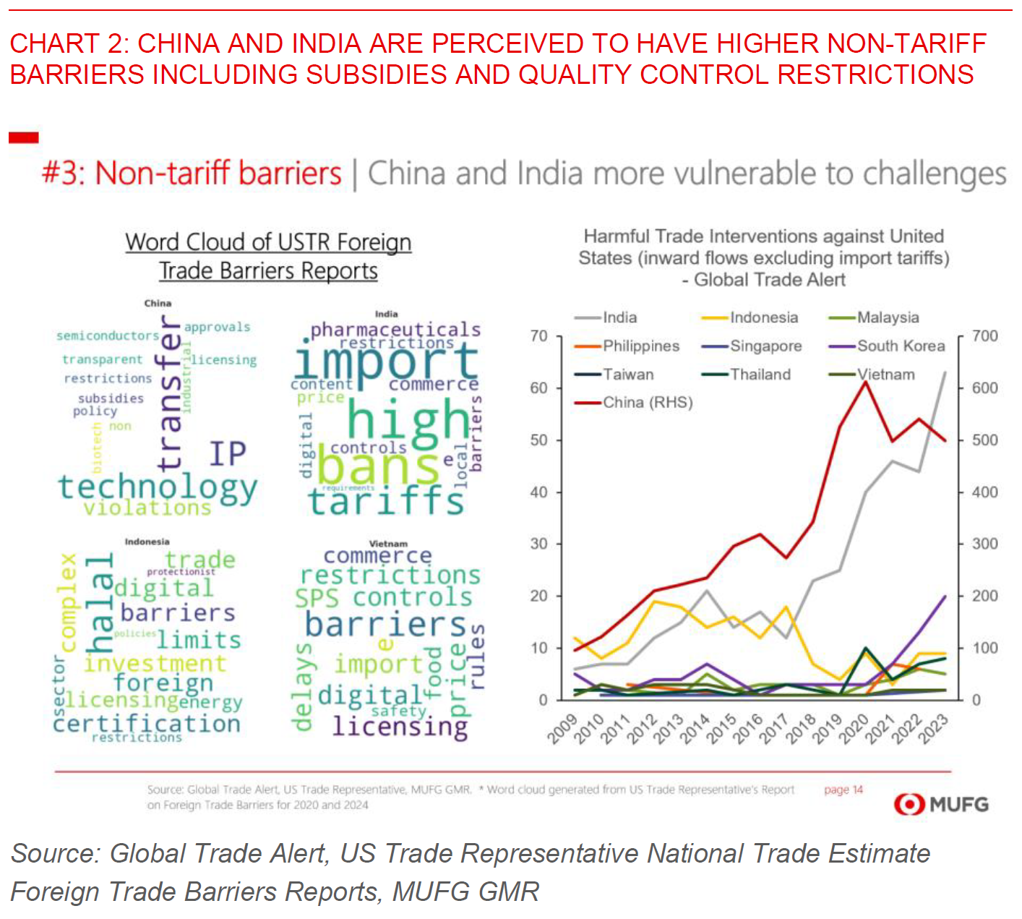

How these tariffs are implemented including in magnitude and breath across jurisdictions will certainly matter greatly for Asia. While initial news reports point to a select 15 or so countries being targeted (the so-called “dirty 15”), President Trump himself dismissed this notion and said these tariffs will start with “all countries”. Meanwhile, the Wall Street Journal reported Trump was pushing his team to be more aggressive in their proposals including revisiting a universal tariff of up to 20% (presumably in combination with reciprocal tariffs). With the official criteria for determining these tariffs encompassing a multitude of factors beyond tariff differentials such as non-tariff barriers, subsidies, value added taxes, exchange rate misalignments, among others, the dispersion of outcomes remains very wide.

Ultimately, we continue to think that markets including Asia FX are underpricing the magnitude of these tariffs, and our North Star is for Trump to be more aggressive than many think possible in a significant structural change to the post-World War II global order, beyond the day-to-day policy whiplash and uncertainty.

Within Asia, the likes of India, Thailand, Vietnam, and China are more vulnerable to reciprocal tariffs, while uniform tariff increases will likely also hit the export-oriented economies such as Singapore, Malaysia and South Korea. For India and to a smaller extent Thailand, they have relatively high tariff differentials with the US, while China and India are perceived to have high non-tariff barriers including subsidies and other key barriers to trade. Vietnam would most certainly stand out in terms of its high trade surplus with the United States and also its strong linkages with the Chinese supply chains. Of course not all things are equal in practice, and the net impact will depend among other things on the country’s export exposure, the US’ dependence on the country on manufacturing and whether there is credible domestic manufacturing capacity (think footwear and toys), and whether tariff differentials change meaningfully with China (substituting China’s exports) and also with other Asian economies.

Regional FX

Asia FX were on the back foot yesterday with the global risk off sentiment and the sharp 4% correction in the Nikkei. The Japanese Yen received an initial bid with its safe haven status, with KRW (-0.3%), TWD (-0.25%) and MYR (-0.2%) underperforming. The Bank of Thailand said on Monday that it is “too soon” to assess the exact economic impact of the recent earthquake. The BOT expects the impact on tourism and private consumption to be short-term, while the property sector may face some pressure from safety concerns. The Thailand central bank has also instructed financial institutions to extend special debt relief for disaster-affected borrowers, similar to measures implemented due to floods a year ago. Meanwhile, South Korea’s exports for March disappointed slightly to 3%yoy (vs consensus of 5%), while the PMIs out of Asia indicated a softening outlook for the likes of South Korea, Taiwan, and Thailand (even before the recent earthquake). Looking ahead, markets will focus on US ISM Manufacturing and ISM Prices Paid, the latter of which may show some increase following tariff increases.