Ahead Today

G3: US mortgage applications, Germany industrial production, Japan leading index

Asia: Thailand inflation, China trade

Market Highlights

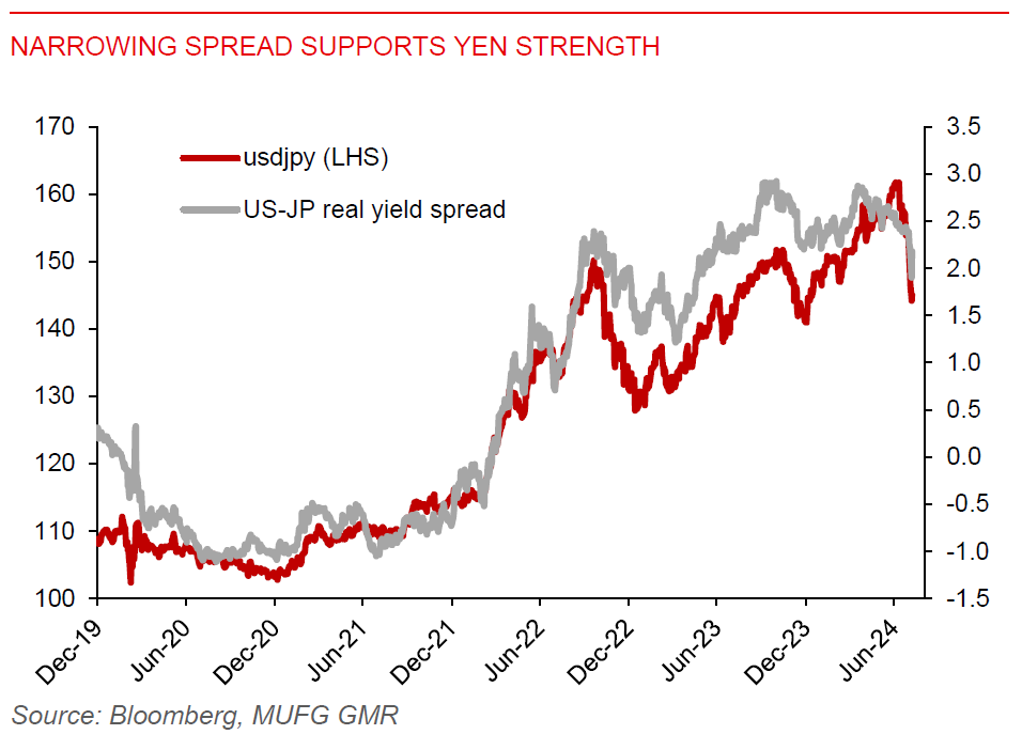

The broad US dollar weakness and an unwinding of the yen carry trade have taken a breather. The US dollar rose 0.3% yesterday vs -0.5% on Monday, while USDJPY rose modestly to the 145.00-level after falling below 142.00 on Monday. Equity volatility has also eased after an initial spike higher.

There could still be room for the yen carry trade to unwind, but for that to happen, we may also need US long term yields to drop sharply. The divergence in monetary policy between the Fed and the BoJ also means there is still scope for the yen to appreciate. Moreover, Japan's real wages rose 1.1%yoy in June, marking the first expansion in more than 2 years, while nominal wages (ex-sampling, bonus and overtime pay) rose 2.7%yoy, supporting further rate normalization in Japan.

We think market volatility could fade after the initial spike higher. But a return to a low macro and FX volatility regime may not be possible, given the risk of a broader slowdown in the US economy, monetary policy divergence, and geopolitical tensions in the Middle East. Miscalculations by either party in the Middle East conflict could risk a full-blown regional war, potentially posing an upside risk to oil prices, which would have implications for inflation globally.

Regional FX

Asian currencies have reversed some of their recent gains against the US dollar, as markets pared back some of their aggressive US rate-cut expectation. Big movers were MYR and THB, which fell about 1% following their recent regional outperformance. But the Philippine peso extended gains to trade below 58.00 per US dollar, as odds of an August rate cut (which would have front-run the Fed in cutting rates) have been reduced after CPI inflation jumped to 4.4%yoy in July on higher utility cost, breaching the central bank’s 4% upper-bound target. Meanwhile, the TWD has been at around the weakest level against the US dollar since 2016. But downward pressure on the Taiwan dollar could start to ease, with the Fed set to lower interest rates as soon as September, seasonal capital outflows pressures have passed, while exports have stayed solid (+23.5%yoy in June).