Ahead Today

G3: Fed’s Goolsbee speaks, US Leading index

Asia: China Loan Prime rate, Indonesia Trade, Thailand Trade

Market Highlights

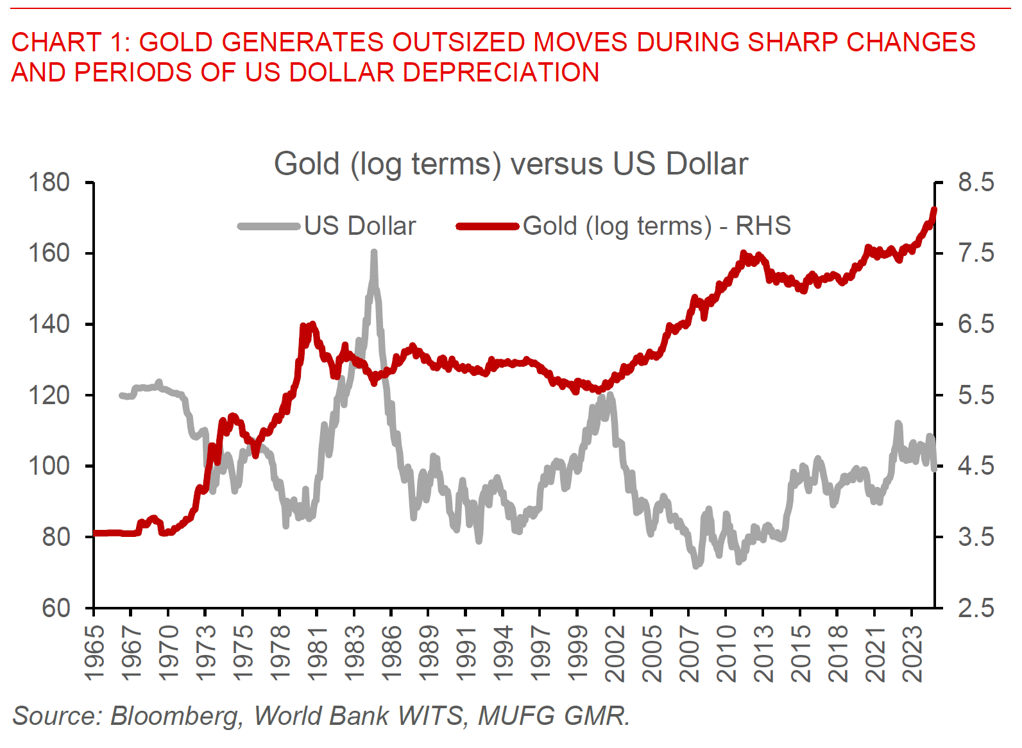

The US Dollar weakened sharply at Asia open, amidst a shortened trading week last week and with several markets still out on holidays. It’s important however to note that the Dollar is not homogenous with Asia FX still underperforming the move stronger in G10 currencies (at least so far) certainly with respect to the likes of EUR and JPY.

What’s driving this further move lower in the Dollar is perhaps the continued theme of the decline of US exceptionalism, with some concerning signs last week that the Trump administration is looking for ways to fire Fed Chair Powell. This came on the back of Chair Powell’s hawkish comments last week when he focused more on making sure second round effects from one-off price increases from tariffs do not result in persistently higher inflation expectations. While we think it is unlikely the Trump administration will be able to remove the Fed Chair outright given the lack of legal authority, any moves on this front will likely create an outsized market move including in FX and is something to watch closely for moving forward. Meanwhile, the US administration’s increasing policy changes against US universities including Harvard could certainly have longer-term impact to the US, including on the spillovers of research and development, attracting international students and perhaps even on existing university endowment investments in assets such as private equities.

Regional FX

Overall, Asian currencies strengthened as the Dollar weakened at the start of the week, with the likes of KRW (+0.3%), MYR (+0.4%), SGD (0.4%) outperforming. South Korea released export data for the first 20 days of April, which showed a 5%yoy decline from a 4%yoy rise the previous month, providing the first indication of an export slowdown post tariff related front-loading in the first quarter of this year. China will release its loan prime rate decision today. We expect PBOC to keep rates unchanged with Chinese authorities keeping some bullets at least for now given the better than expected data out in the month of March and 1Q. Meanwhile, both Indonesia and Thailand will release its trade balance numbers for March, which are expected to show some narrowing to US$2.9bn and US$1.1bn respectively. Looking further ahead this week, we will have Bank Indonesia’s policy decision, where we expect BI to remain on hold for now given the volatile IDR. We think the BI ultimately remains dovish and should cut rates at some point this year, but IDR weakness is constraining the central bank at this point in time