Ahead Today

G3: Eurozone Services PMI, US ISM Services PMI

Asia: China Caixin Services PMI

Market Highlights

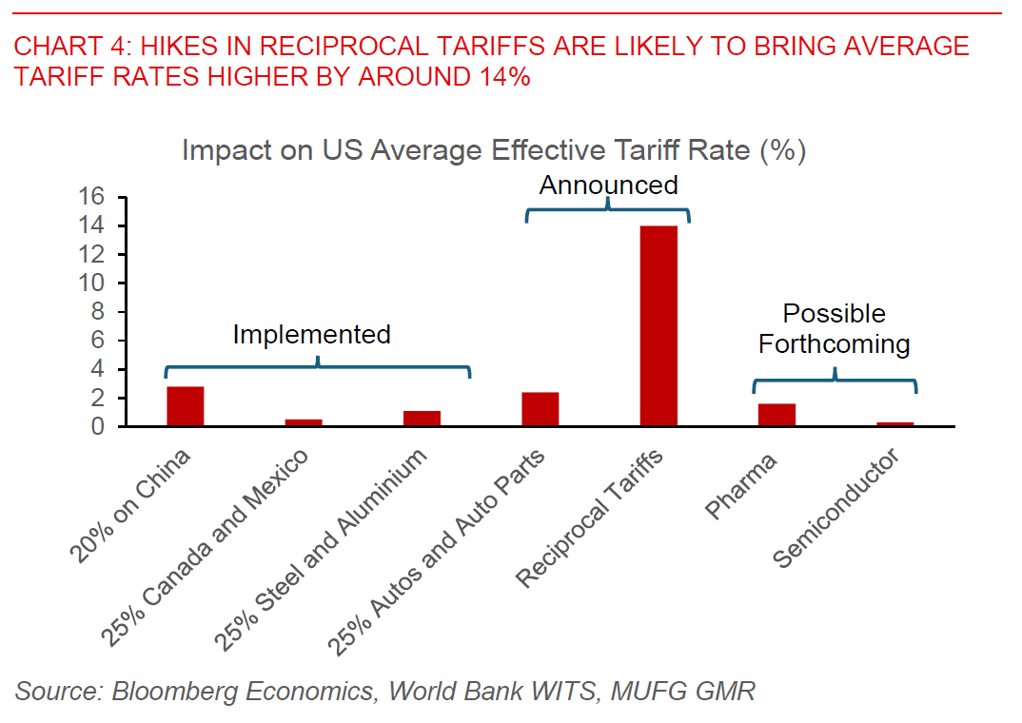

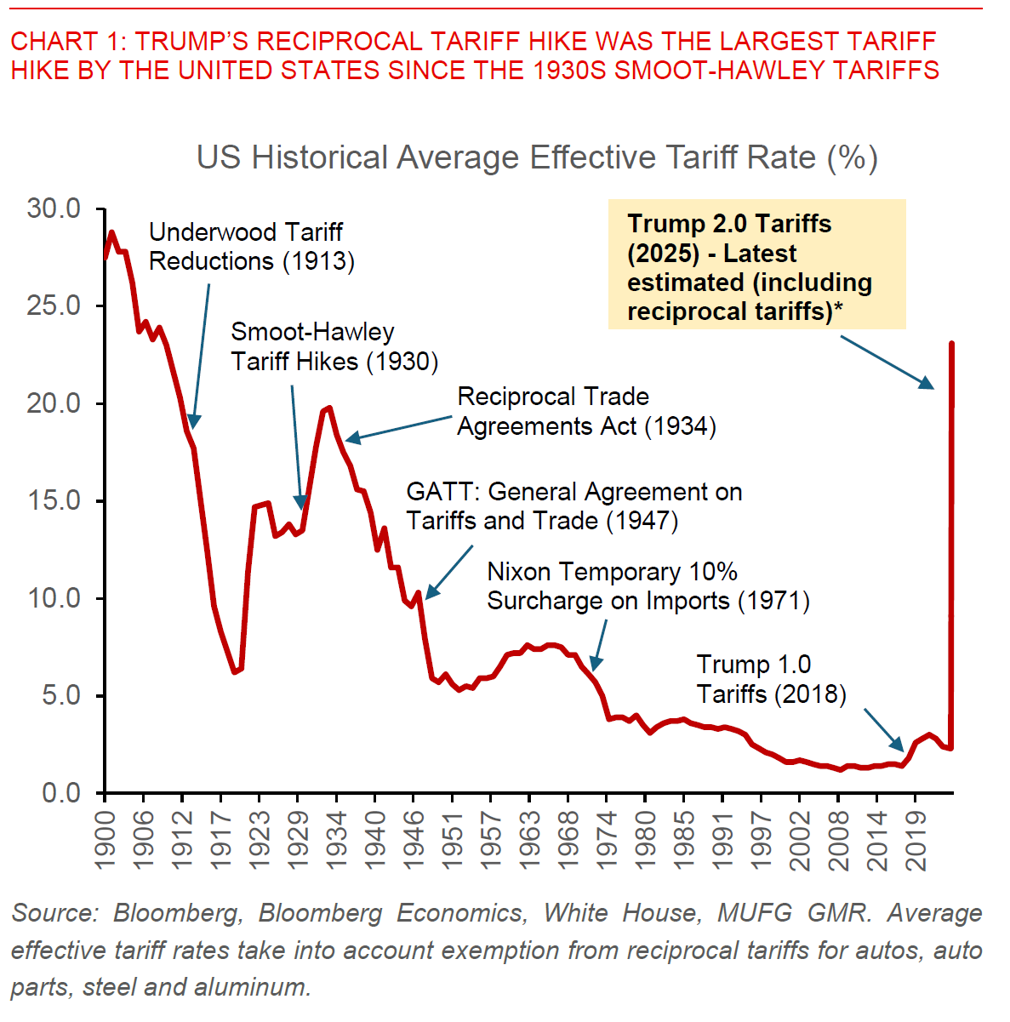

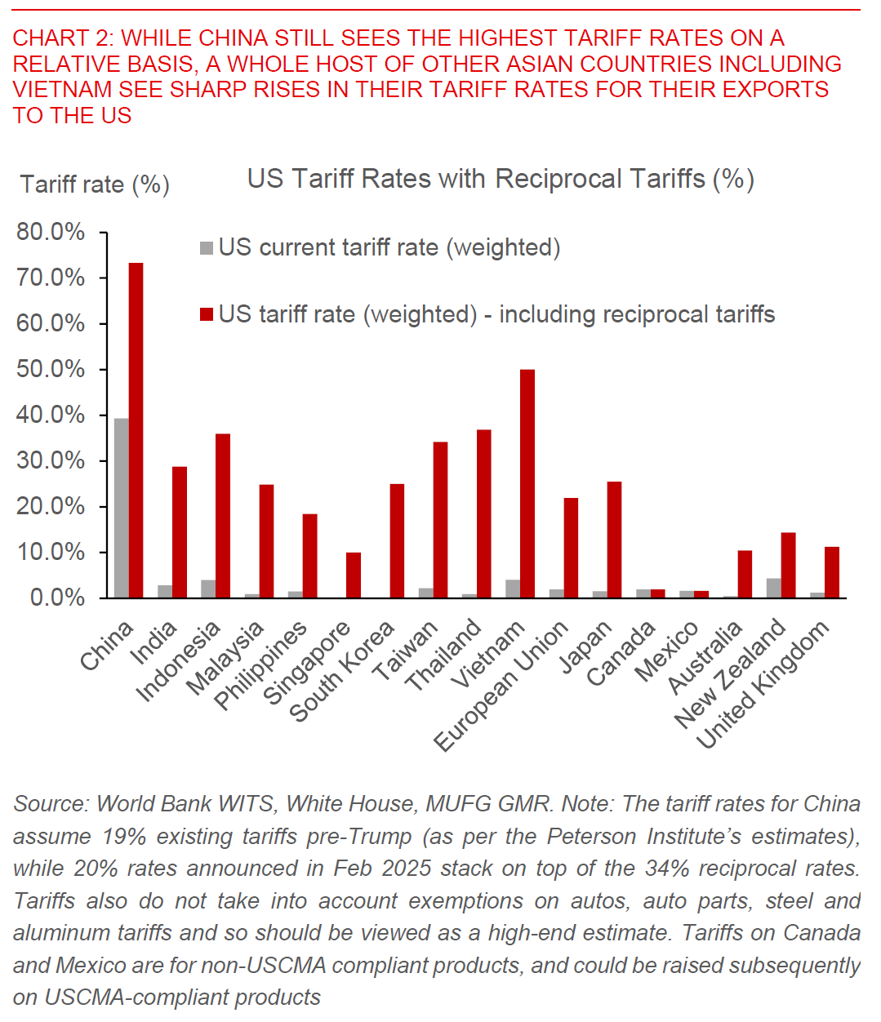

In what we estimate to be the largest tariff hike by the United States since the 1930s Smoot-Hawley tariffs, President Trump announced his reciprocal tariff plan overnight. The administration set a minimum baseline tariff of 10% on all countries, and additional reciprocal tariffs up to 49% for 60 countries.

We estimate US average effective tariff rates are now expected to rise to 23%. This would bring tariff rates above those last seen in the 1930s.

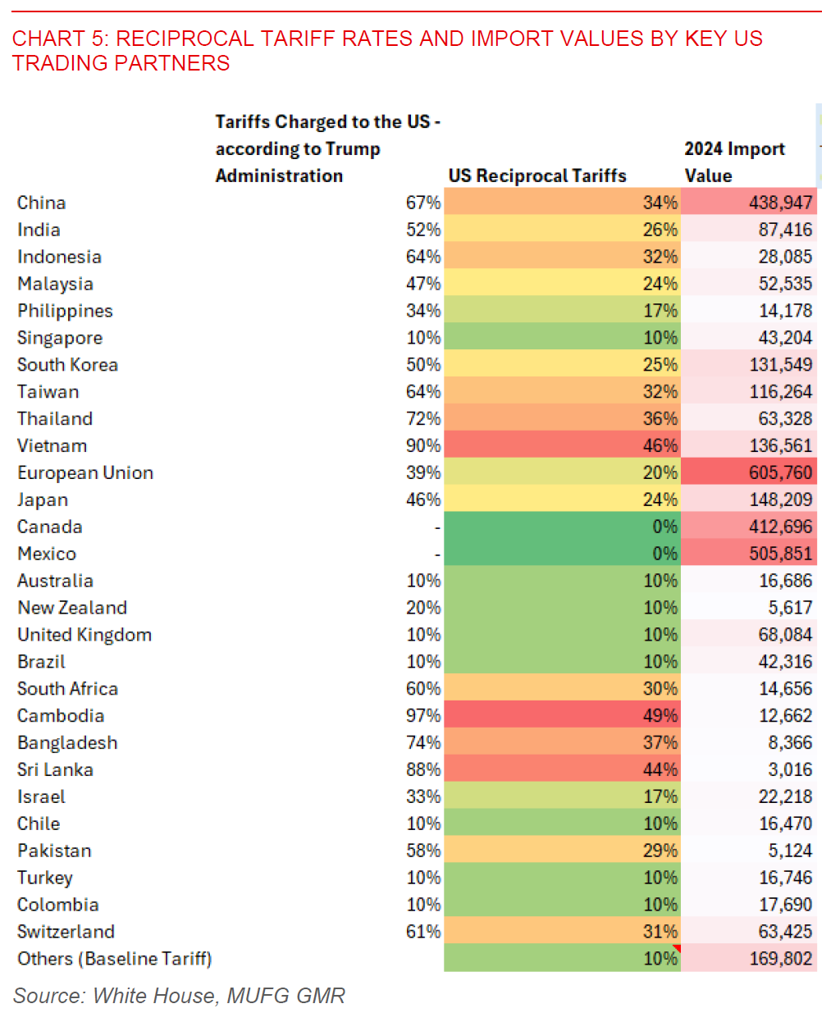

Asia is generally harder hit than other regions. Among the Asia markets we cover, Vietnam (+46%), Thailand (+36%), China (+34%), Taiwan (32%), Indonesia (+32%), and India (+26%) received the highest increase in reciprocal tariffs. Nonetheless, even the Philippines (+17%) and Singapore (+10%) which we thought were the two least likely to be targeted in our region were not spared as well. Canada and Mexico seem to be exempted from these tariffs for now, at least until perhaps a review at a subsequent date on its USCMA-compliant trade.

Regional FX

While we have been of the view that investors were underpricing the downside risks to growth from these reciprocal tariffs, the magnitude with which Trump has announced and increased them certainly also caught us by surprise (see Asia FX Talk – How will reciprocal tariffs be implemented for Asia? for instance).

The dispersion of tariff rate increases between countries also seem somewhat arbitrary. For instance, we would have thought that India would rank higher than Indonesia and Vietnam when taking into account tariff differentials and non-trade barriers, but that was not the case.

From an FX perspective, we think the path of least resistance is for weaker Asian currencies from a directional perspective here, and certainly for the export-oriented ones and those who were hit harder such as China, Vietnam, Thailand, and South Korea.

For Vietnam for example, while we have been positive on the country’s structural prospects in exports, our underlying assumption for USD/VND to rise to 25,900 by 2Q certainly did not take into account a 50% tariff rate.

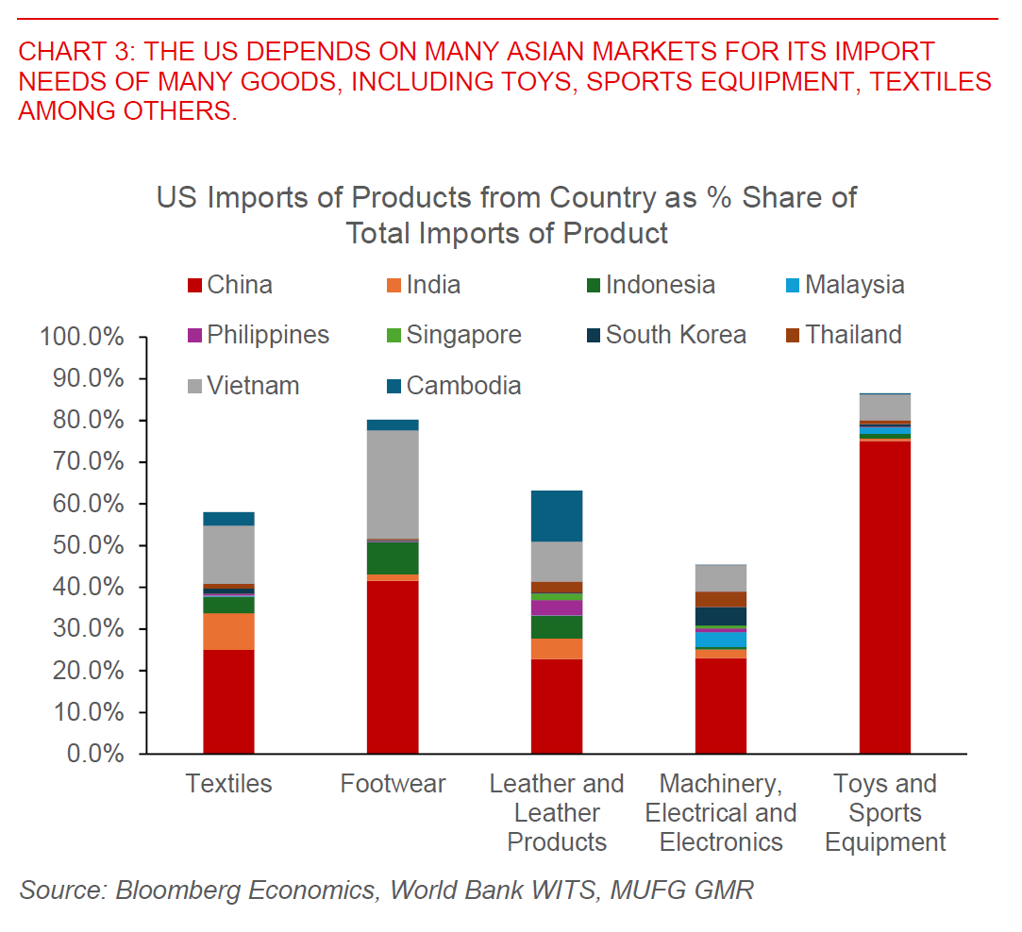

Nonetheless, we would note that FX is a relative price, and the magnitude of Asian currency weakness will also depend on how investors and the market view the relative growth and yield impact in the US versus other countries. With such a broad swath of countries being negatively impacted, we note that the ability for the US to substitute to alternative supplies is much more limited, and hence the possible growth and inflation hit to the US itself. To make it more concrete, we note that Asian economies supply 87% of US import needs of toys and sports equipment, and also 80% of US imports of footwear. These are the products which also likely have much negligible domestic capacity to ramp up supply to meet domestic demand within the US.

Much will also depend among other things on how and whether other countries retaliate, and also whether there is room for negotiation before the actual implementation of the tariffs. We note that the reciprocal tariffs are only slated to take effect on 9 April, and so there could be a few days of frenzied deal-making and negotiation in the lead-up to that.