Ahead Today

G3: US Initial Jobless Claims, US Continuing Claims, Australia Employment Change

Asia: China Retail Sales, Industrial Production, Fixed Assets, Property Investment, 1-year MLF rate, BSP Policy rate

Market Highlights

US CPI was manageable and highlighted continued disinflation in the US, coming roughly in line with expectations, with a 0.165% mom rise in the headline rate up from -0.1% previously, together with a 0.205% mom increase in core. Details showed core goods inflation declining further in July and in line with used car auction prices seen thus far. Core services inflation however increased by 0.3%, led by a pickup in shelter and recreational services, but offset by a sharp drop in medical care inflation. Moving forward and beyond the month-to-month bumpiness, we should see continued disinflation both in rents and services given softer labour market and housing trends, although the pace of goods inflation declines may not continue.

Overall, this number further bolsters the case for a rate cut in September, although we note that the Fed Fund Futures and OIS markets have pared back expectations for a 50bps Sep rate cut over the past week or so. With the focus of the markets shifting also to growth beyond just inflation, today’s US initial jobless claims together with labour market numbers more broadly will take on more importance moving forward. We will also get China’s monthly data for July today such as retail sales, industrial production and fixed asset investment, which will be important to gauge the economy’s momentum. Over here we think that more stimulus will be needed especially on the back of soft credit growth, with today’s 1-year MLF decision also closely watched.

Regional FX

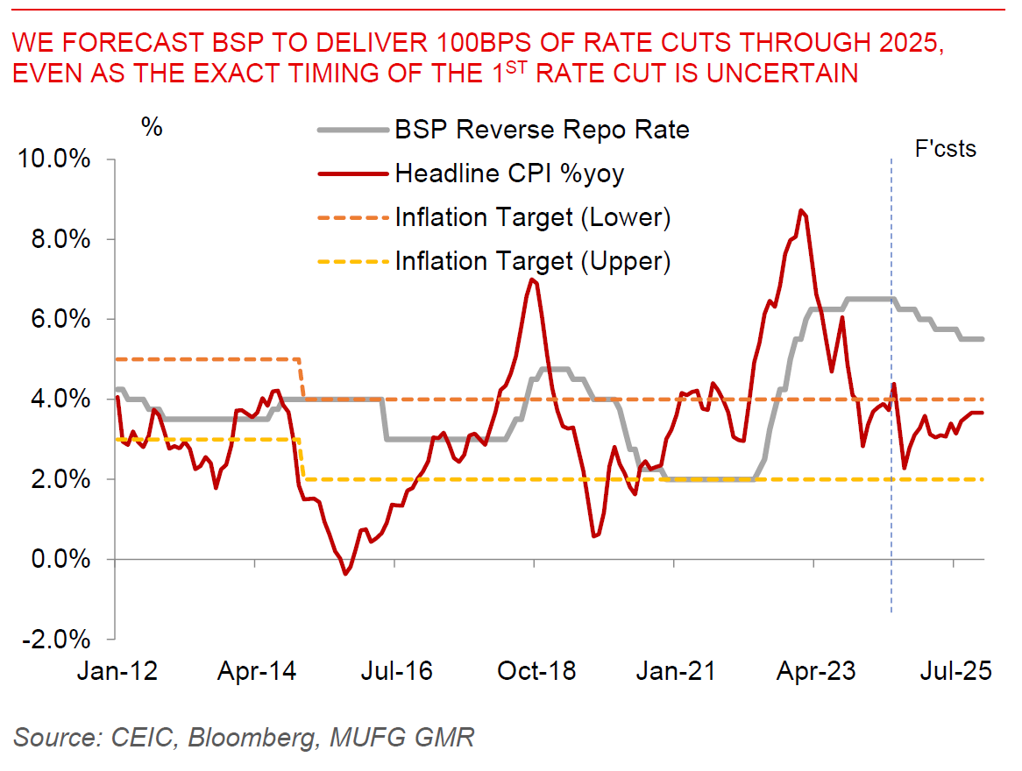

Asian FX was mostly stronger on the back of a softer Dollar from yesterday’s trading session, with IDR (+1.77%), THB (+1%), MYR (+0.76%) and PHP (+0.65%) outperforming, while INR underperformed (+0.03%). Markets will watch closely for the Philippines BSP central bank’s policy meeting today. The policy meeting is a very close call, with 13 out of 23 economists (including ourselves) calling for a 25bps rate cut, while the rest calling for a hold. The recent public comments out of both BSP Governor Remolona and also BSP Monetary Board Member Ralph Recto (also Finance Secretary) have been mixed, but tilt slightly more hawkish. BSP Governor Remolona said that the Philippines central bank has space to maintain tight monetary policy settings after strong 2Q GDP data, while recent pickup in inflation makes a rate cut “a little bit less likely”. This is even as the BSP does not want to keep rates unnecessarily high and will ease when inflation is on its way to target range. Meanwhile, Finance Secretary Ralph Recto said the strong Philippines Peso is a factor for easing, while good growth and low unemployment rate are factors to keep rates on hold.

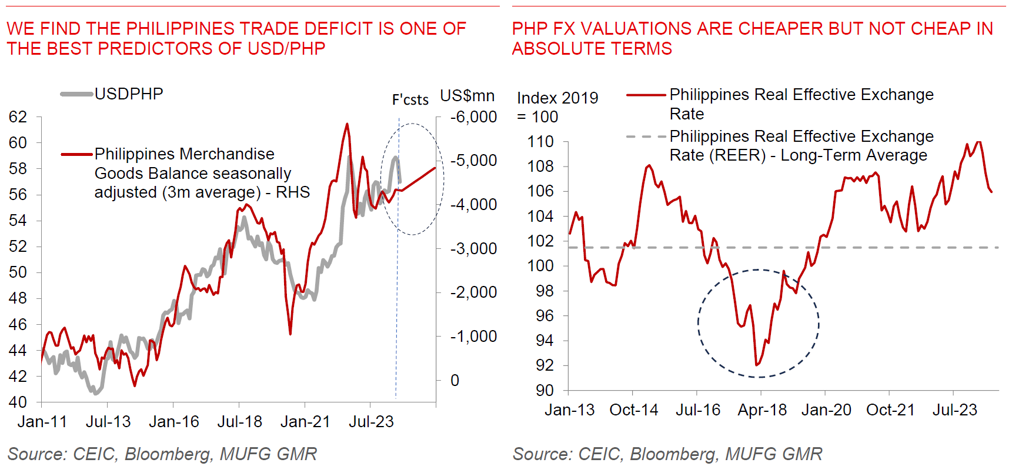

From an FX perspective more broadly, USD/PHP has moved down quite meaningfully since we last published our update and forecasts, and has now gone down below our 2Q2025 forecast of 57.50 to 56.955 (see Philippines: USD/PHP – From Divergence to Convergence?). Part of this is due to global factors which has probably helped support foreign bond flows into the Philippines, but likely also includes building in a possible delay in BSP rate cuts. Over the near-term, there is probably some space for USD/PHP to come down somewhat more towards the 56 handle with better current account and remittances seasonality in 4Q together with good fundamentals of the economy. While we are not bearish on PHP, we stress that the fundamental medium-term macro factors which we have highlighted in our latest report are still relevant, and we don’t think a sharp and sustained PHP rebound like what we saw from 4Q2018 to 2019 is likely further into 2025 (see Philippines: USD/PHP – From Divergence to Convergence?). For one, we still expect the current account deficit to widen from here as infrastructure and import needs pickup. Second, FX valuations as denoted by REER deviation from long-term averages are not cheap in absolute terms. Third, we still expect the BSP to deliver 100bps of rate cuts through 2025, even if it does delay the timing somewhat. Fourth, there are some left-tail risks to growth to watch for, including from Typhoon Carina and the recent ban on Philippines Offshore gaming Corporations (POGOs).