Ahead Today

G3: US Import Price

Asia: China Industrial Production, Retail Sales, Fixed Asset Investment

Market Highlights

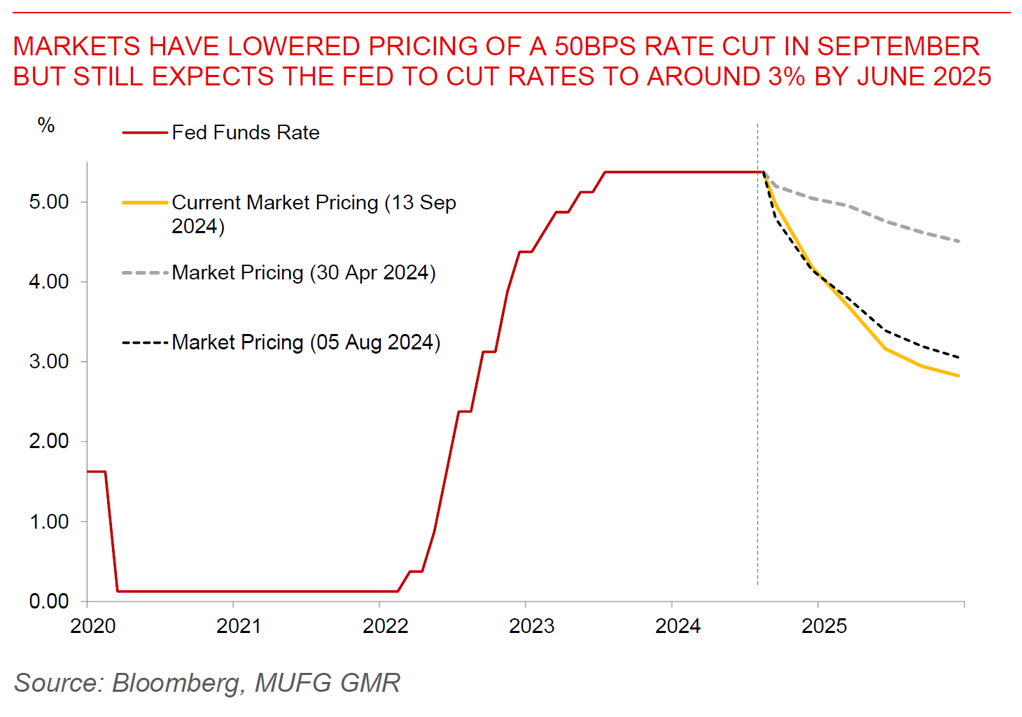

Risk assets rose, gold went up to all time highs, and the Dollar weakened as markets attempted to look past recession fears, while the European Central Bank cut rates by 25bps in its September meeting. The ECB in particular left its policy guidance for rate cuts unchanged, and continued to support a data-dependent and meeting by meeting approach, while not making any commitment on its October rate decision. This helped to support the EUR to some extent – and as such Dollar weakness. Meanwhile, the US PPI numbers were a touch higher than expected and also came on the back somewhat stickier CPI numbers out earlier in the week. More importantly, there was some slight tick up in the US initial claims data. While markets have generally reduced the probability of a 50bps rate cut in the Fed’s September meeting next week, more importantly, the Fed funds futures market is still pricing in for the rate to reach 3% by the middle of next year. A Wall Street Journal by Nick Timiraos released yesterday which highlighted that a 25bps or 50bps rate cut in the Sep meeting has not been decided may also have impacted markets and lowered US yields to some extent.

Meanwhile, Bloomberg news reported that China is poised to cut interest rates on more than US$5 trillion on outstanding mortgages in September, with some homeowners enjoying up to 50bps of immediate rate reduction. We will get China’s monthly data over the weekend which may show some moderation in economic momentum.

Regional FX

Asian FX markets traded stronger against the US Dollar, with KRW (+0.59%), PHP (+0.37%), and CNH (+0.29%) outperforming. INR continued to underperform the Asian FX complex remaining around the 84.00 handle. India’s CPI inflation came in a touch higher than expected at 3.65% (vs consensus for a 3.5%) rise. On a sequential basis, these numbers imply that headline inflation rose 0.1% mom, while core inflation moderated to 0.3%mom in August, with lower spikes in food prices helping to cap overall inflation pressures. These inflation prints are also lower than what RBI has assumed in its latest August monetary policy meeting, and as such, should keep a rate cut on the table. The good news is that the monsoon has been running above normal and better than expected, while overall global oil prices are also subdued with some potential for Oil Marketing Companies to eventually cut domestic fuel prices some time down the line if current prices sustain. We see the 1st RBI rate cut in 1Q2025 (calendar year) for a shallow rate cut cycle of 50bps.