Ahead Today

G3: US mortgage applications, ADP employment change, factory orders

Asia: Asia PMIs

Market Highlights

Fed’s Barkin has said that President Trump’s tariffs could hurt jobs and raise inflation. He has also added that uncertainty is still high over what trade policies will be implemented.

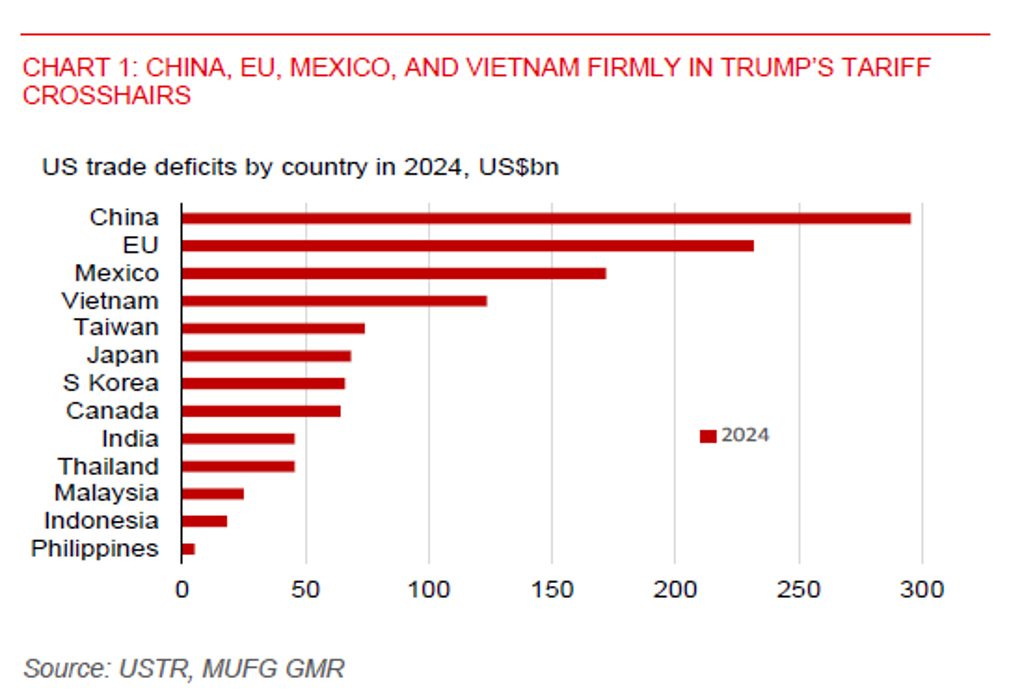

According to news reports, Trump is thinking about 3 different tariff options – a universal 20% tariffs, a tiered system with 3 different tariff rates, and country-based tariffs. A blanket 20% tariff is less likely, according to an official that was quoted by CNBC, and that the goal is to have country-specific tariffs. Trump will be announcing his reciprocal tariff plans today. Sectoral tariffs involving pharmaceutical and semiconductors, among others, would be announced at a later date, while the 25% auto tariff announced earlier will come into effect on 3 April.

President Trump has earlier said that reciprocity is very important, and in some cases, tariffs may be substantially lower. The concept of being reciprocal can cut both ways, either US raises tariffs to match the higher rate that other countries are imposing on its products or trading partners could choose to lower their tariff rates on US imports, which could in turn limit the extent of tariff hikes US would impose on them. Vietnam has announced that it will lower duties on a range of US imports, including LNG, cars, and certain agricultural products. President Trump has also said he heard that India will reduce tariffs on US products substantially.

Meanwhile, US economic data shows a slightly weaker labour market, with jobs opening slightly lower at 7568k in February versus 7762k in January, quit rates easing to 2% from 2.1%, and layoff rate inching up to 1.1% from 1%. The ISM manufacturing index fell to 49.0 (< 50 indicates contraction) in March, from 50.3 in February, with new orders (45.2 vs. 48.6 prior) and employment (44.7 vs. 47.6 prior) sub-indices falling deeper into contraction. However, ISM prices paid jumped to 69.4 from 62.4 in February. US Treasury yields have declined across the curve amid potential negative impact of tariffs on US economic growth.

Regional FX

Asian currencies weakened against the US dollar yesterday, with the Thai baht (-0.5%) leading losses, while CNH (-0.2%), SGD (-0.1%), and VND (-0.2%) fell modestly. Several Asian markets were closed for a public holiday yesterday. Asian FX will brace for US reciprocal tariff risks and might weaken further against the US dollar. Notably, India is the most exposed to US reciprocal tariff hikes in Asia, given its relatively larger tariff differential with the US. Also, the large trade deficit that US has with Vietnam could lead to increased US tariffs on Vietnam.

China's private manufacturing PMI showed factory activity expanding at the fastest rate in four months in March, on the back of robust export orders. However, this improvement could prove to be short-lived, given rising US tariffs.

Elsewhere, we have downgraded our 2025 growth outlook for Thailand to 2.2% from 2.8% previously following the earthquake, which could hurt the tourism industry. The Thai Hotels Association has predicted that visitor arrivals could decline by up to 15% or possibly more in the next couple of weeks. Thai baht has been resilient so far against the US dollar, but this may not last, given a weaker outlook for domestic growth, likely lower visitor arrivals in the coming months, and potential reciprocal tariff hikes (see Thailand: Growth outlook downgraded after the earthquake, baht to weaken). Meanwhile, we think Singapore won’t be directly targeted by Trump. But given it is a major transshipment hub, the SGD is still highly exposed to higher global tariffs and a slowdown in world trade.