Ahead Today

G3: US CPI, initial jobless claims

Asia: Philippines trade

Market Highlights

The US dollar index rose 0.4% to 102.90 on Wednesday’s session, underpinned by resilient US economic growth and haven bid resulting from rising geopolitical risks in the Middle East. The FOMC minutes shows strong consensus for a jumbo 50bps rate cut in September, but there was pushback with some members favouring a smaller 25bps cut. Fed’s Vice Chair Philip Jefferson said the risks to employment and inflation goals are broadly in balance. Markets will await the September US CPI data today, where a hotter than expected print could provide impetus for the US dollar to strengthen more.

Among G10 currencies, the New Zealand dollar was the weakest, after RBNZ cut the policy rate by 50bps to 4.75%. This follows a 25bps cut in August, as the economy is slowing, unemployment is rising, and house prices are falling. JPY has continued to weaken towards the 150-level against the US dollar since the dovish comments by new Prime Minister Ishiba. But latest wage data shows the base pay for full-time workers in Japan rose by 2.9%yoy in August from 2.6% in July. This may give authorities some confidence that solid wage growth could lead to inflation and fuel market optimism that interest rates can gradually normalise.

Regional FX

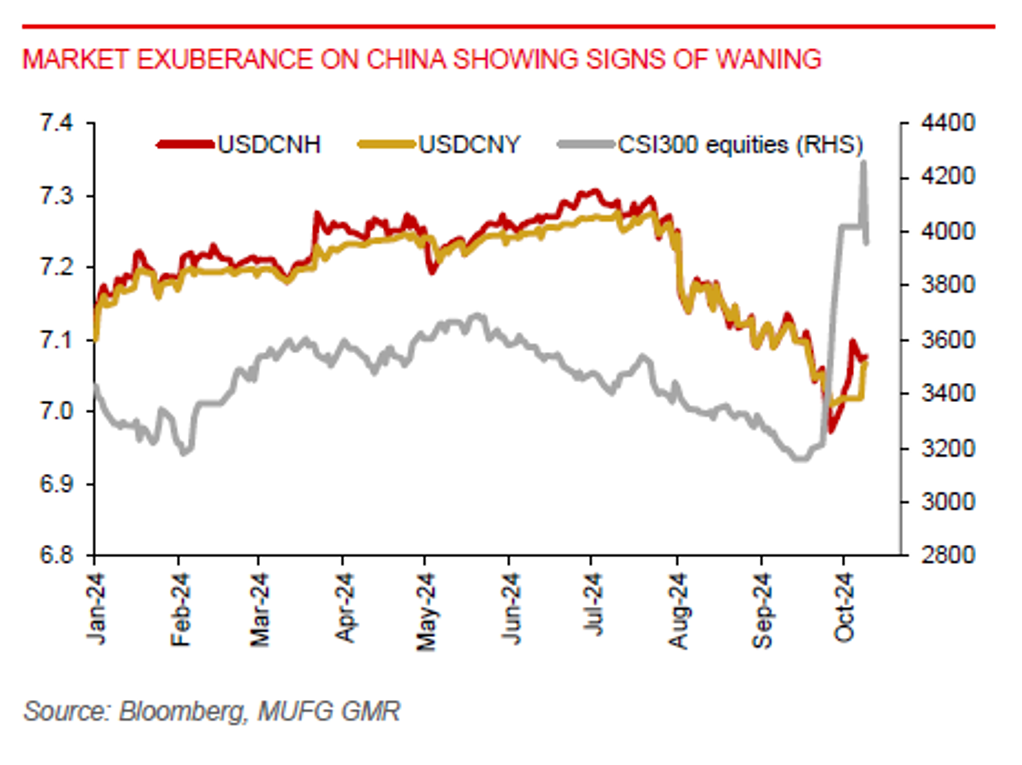

Asia ex-Japan currencies were muted against the US dollar. Markets will look for additional policy stimulus from Chinese authorities at the fiscal policy briefing on 12 October. Any policy disappointment from that meeting could put downward pressure on the CNY, particularly with US elections this November fast approaching and amid global trade policy uncertainty.

The Reserve Bank of India left its key policy rate unchanged at 6.50% yesterday and turned less hawkish with a unanimous vote to alter its policy stance to “neutral”. The policy decision was in line with our view that the RBI will turn more dovish, with the door likely opening for a rate cut during the December policy meeting. RBI also lowered its near-term growth and inflation forecasts for 2QFY2024/25 to 7% and 4.1% respectively (from 7.2% and 4.4%), but with an expectation for a tick-up thereafter.