Ahead Today

G3: Speech by Fed’s Goolsbee

Asia: Thailand exports, Singapore CPI

Market Highlights

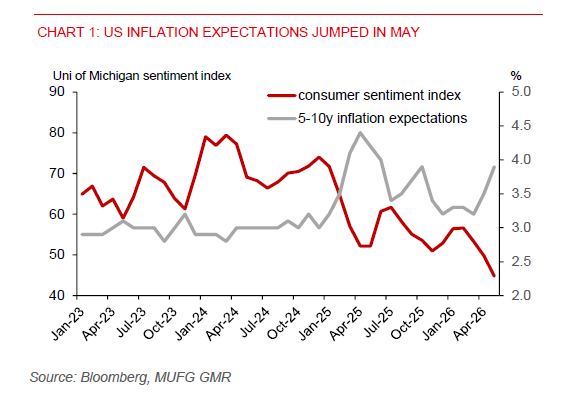

US 2-year yields have continued to grind higher, with markets now fully pricing in one Fed rate hike by January 2027. US average gasoline prices remain elevated, staying above $5 per gallon. The University of Michigan’s May survey showed long-term inflation expectations rising to 3.9% from 3.5% in April, while consumer sentiment fell to a record low.

Positioning-wise, long USD exposure picked up modestly over the past week, though it is not yet stretched. Focus shifts to communication from the new Fed Chair, Kevin Warsh, as markets assess how he will navigate a backdrop of rising inflation risks, weakening consumer confidence, and elevated US government debt.

On the geopolitical front, Trump has announced that a deal with Iran has been largely negotiated. Gulf nations, including the UAE, Saudi Arabia, and Qatar, continue to advocate for a diplomatic resolution and warn against further escalation. For now, momentum remains with USD strength, supported by yields and macro resilience. However, positioning remains vulnerable to a sharp reversal should geopolitical risks ease sharply.

Higher US 2-year yields and still-elevated Brent prices are likely to remain a drag on IDR, PHP, and INR. A meaningful easing in pressure on these currencies would likely require a de-escalation in geopolitical risks, most notably a US–Iran agreement that ensures transit through the Strait of Hormuz.

PHP appears particularly vulnerable, given the sharp rise in inflation and a BSP policy rate of just 4.50% that is insufficient to compensate for the rising risk premium.

For INR, the recent USDINR rally could extend towards the 100.00 level should the Iran conflict persist, and oil prices remain above $100/bbl. That said, RBI intervention and the possibility of rate hikes could offer intermittent support.

For IDR, momentum remains skewed towards further USDIDR upside, with rising fiscal and current account pressures, alongside weak investor sentiment around government policies, reinforcing rupiah vulnerability. However, there is risk of a reversal with USDIDR already in overbought territory, and particularly if there is a breakthrough in US–Iran negotiations. On valuation, the rupiah appears cheap on a REER basis, while higher-yielding SRBI instruments offer some compensation for the elevated risk premium.