Ahead Today

G3: US initial jobless claims, retail sales

Asia: BOK policy meeting

Market Highlights

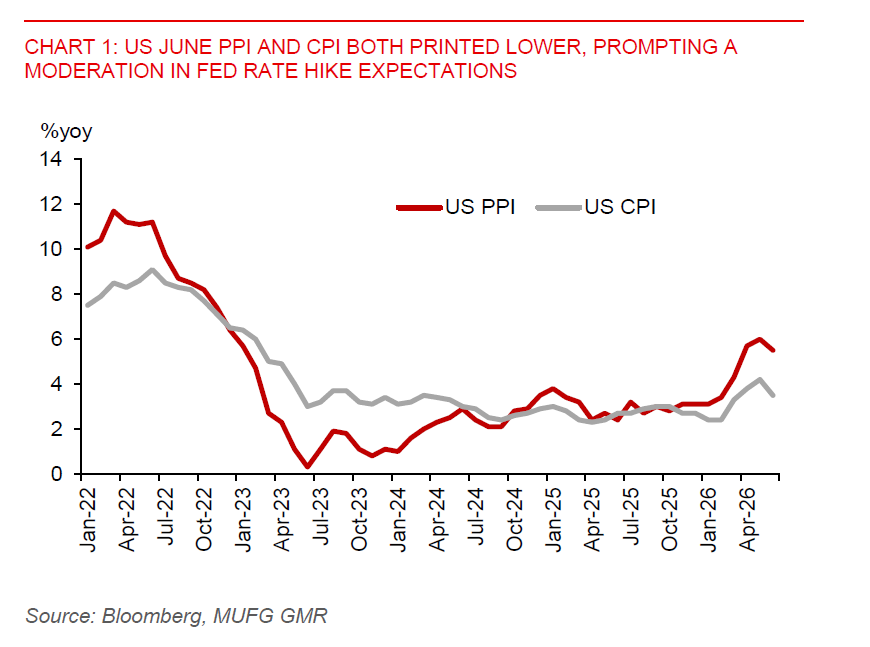

US producer price inflation surprised to the downside in June, reinforcing signs of easing price pressures. Headline PPI fell 0.3%mom, reversing part of May’s 0.6% increase, while core PPI rose 0.2%mom, up from 0.1% in May but below the market consensus of 0.3%. On a year-on-year basis, headline PPI eased to 5.5% from 6.0%, coming in below expectations. The softer-than-expected PPI print follows the recent downside surprise in CPI, prompting markets to pare back Fed rate hike expectations. In response, the dollar weakened by 0.4%, while US Treasury yields declined, with the 2-year yield falling 6bps to 4.13% and the 10-year yield down 4bps to 4.55%. Meanwhile, the Fed’s latest Beige Book indicated that economic activity continued to expand at a moderate pace, supported by improving business sentiment, sustained AI-related investment, and lower fuel prices.

China’s Q2 GDP growth disappointed, slowing to 4.3%yoy from 5.0% in Q1 and undershooting the 4.5% consensus forecast. Urban fixed asset investment fell 5.7% in the first half of the year, a steeper decline than the 5.0% drop expected by markets. The property sector remained a significant drag, with property investment contracting 18%yoy in H1. Consumer demand also remained subdued, with retail sales rising just 1.0%yoy after a 0.6%yoy decline in Q1. One bright spot was industrial production, which accelerated to 5.3%yoy from 4.5% previously. Going forward, it bears close monitoring whether China’s slowing growth momentum will generate negative spillover effects across Asia through weaker trade activity and external demand.

Despite the softer dollar backdrop, USDTHB has broken above the 33.50 level, and we continue to see scope for further baht weakness. Thailand’s low carry profile remains a headwind, while the recent rebound in oil prices is likely to worsen the country’s terms of trade. Growth risks have also increased amid the re-escalation of Middle East tensions, which could encourage the Bank of Thailand to maintain an accommodative policy stance to support the economy. In addition, our valuation metrics suggest that the baht remains modestly overvalued.

Meanwhile, the Korean won has been one of the better-performing Asian currencies so far this month, supported by the Bank of Korea’s relatively hawkish policy stance, which has helped narrow some of the won’s deep undervaluation against the US dollar. The BoK is widely expected to raise rates by 25bps to 2.75%, amid resilient semiconductor exports and inflation that remains above the central bank’s 2% target. Nevertheless, we remain cautious on the broader Asia FX outlook, particularly if China’s slowdown deepens and US growth continues to outperform.