Ahead Today

G3: US U of Mich Sentiment, US PPI, China Trade

Asia: India CPI, India IP

Market Highlights

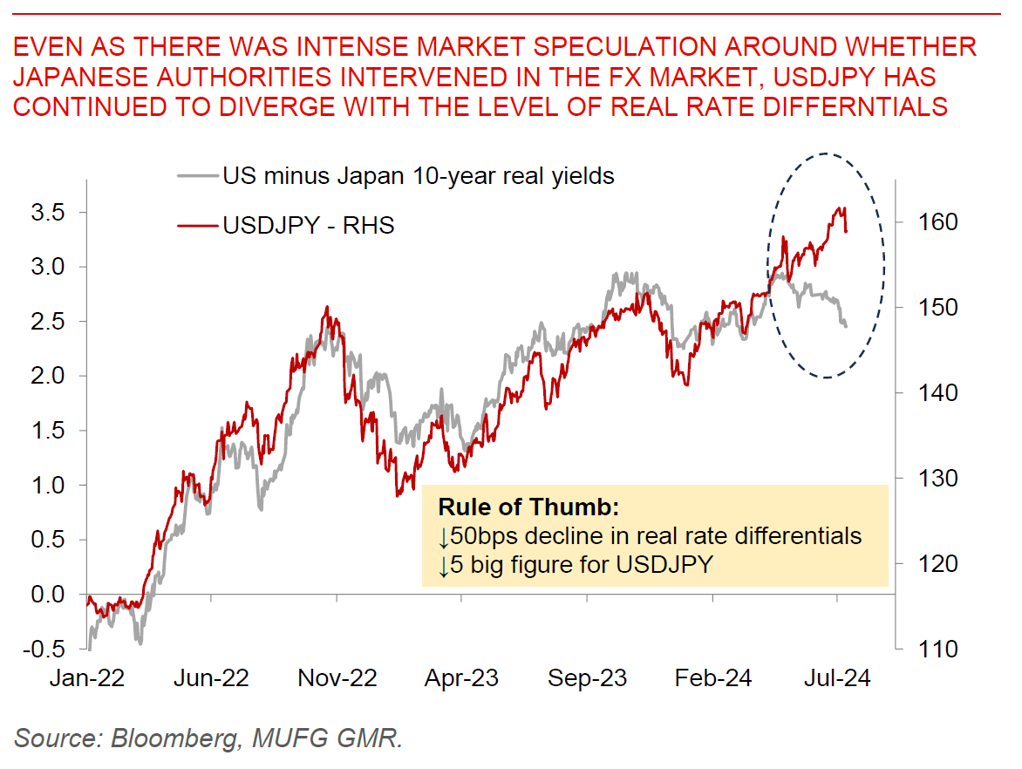

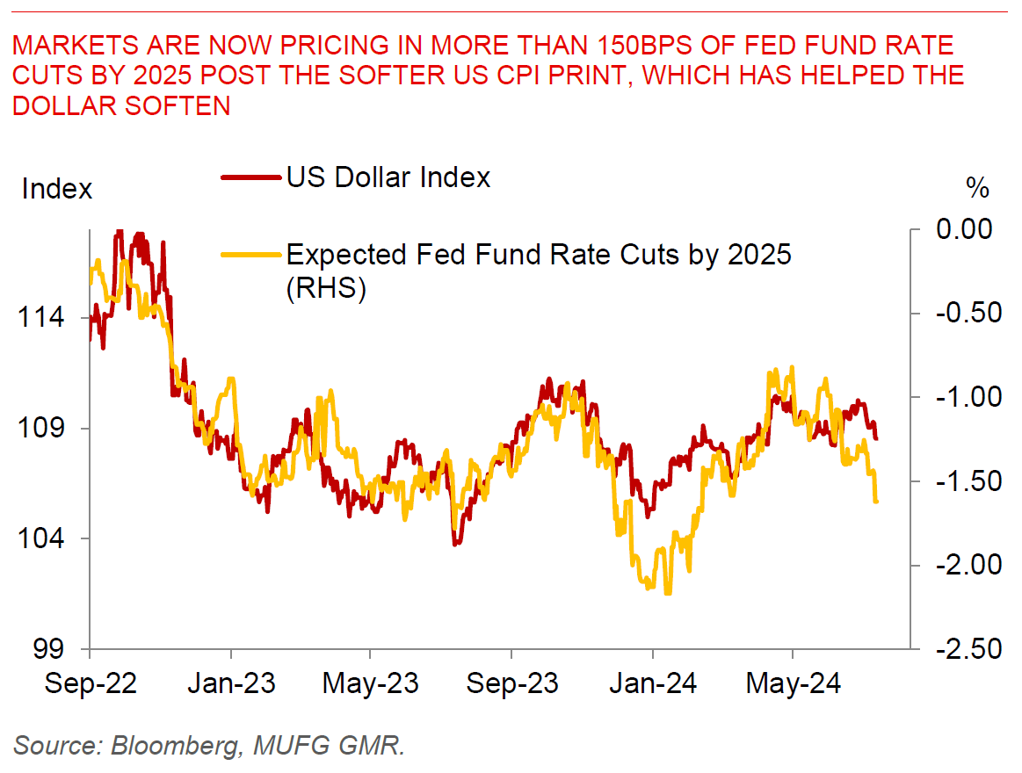

The Dollar weakened sharply, US yields came off, while JPY strengthened significantly on the back of a softer than expected CPI print, together with suspected FX intervention by Japanese authorities. Headline CPI inflation in the US fell 0.1% mom while the core rate rose a smaller than expected 0.1% mom. The details suggest good news for the path forward for disinflation, with the shelter component moderating to 0.17%mom from 0.4%mom, and finally catch-up to higher frequency measures of new rental leases. Other key contributors to the lower core inflation rate include falling used car prices, weaker airline fares, although some other services such as motor insurance, medical care and personal services remained sticky. While the pace of declines could slow for items such as used car prices and core goods, the softer labour market coupled with lower rate of measured shelter inflation should keep a lead on services components.

Markets are now fully pricing a September Fed rate cut, but more importantly, are expecting the Fed Funds rate to reach around 3.70% by the end of next year (a meaningful change from 4% at the end of last month). The biggest market mover overnight was USDJPY, which fell to 158.63 from above 160 before the CPI print. There was intense speculation that authorities conducted FX intervention, although top currency official Masato Kanda would neither confirm nor deny about FX intervention.

Regional FX

Regional FX

Asian FX markets strengthened on the back of the weaker Dollar and stronger JPY, with currencies such as THB (0.7%), MYR (0.7%), coupled with SGD outperforming (+0.5%). USDCNH dropped to 7.266 from 7.28 previously, likely also on the back of the stronger JPY. We had two key central bank decisions yesterday with the Bank of Korea and Bank Negara Malaysia both keeping rates on hold. More importantly while the Korean central bank kept its policy unchanged at 3.5%, it dropped clear hints that interest rate cuts would be coming soon, even as BOK Governor Rhee signaled concerns over excessive market expectations on rate cuts coupled with the pick-up in household debt and house prices. Two of the seven BOK board members said they were open to the possibility of a rate cut in the next three months, up from one in the May meeting. Meanwhile, Bank Negara Malaysia kept rates unchanged but also signaled uncertainty over the inflation outlook given subsidy reforms, with inflation expected to average 2-3.5% in 2024. We continue to think that BNM keeps rates on hold this year at 3%.