Ahead Today

G3: US initial jobless claims and wholesale inventories

Asia: Philippines Q2 GDP, RBI policy meeting, Taiwan trade

Market Highlights

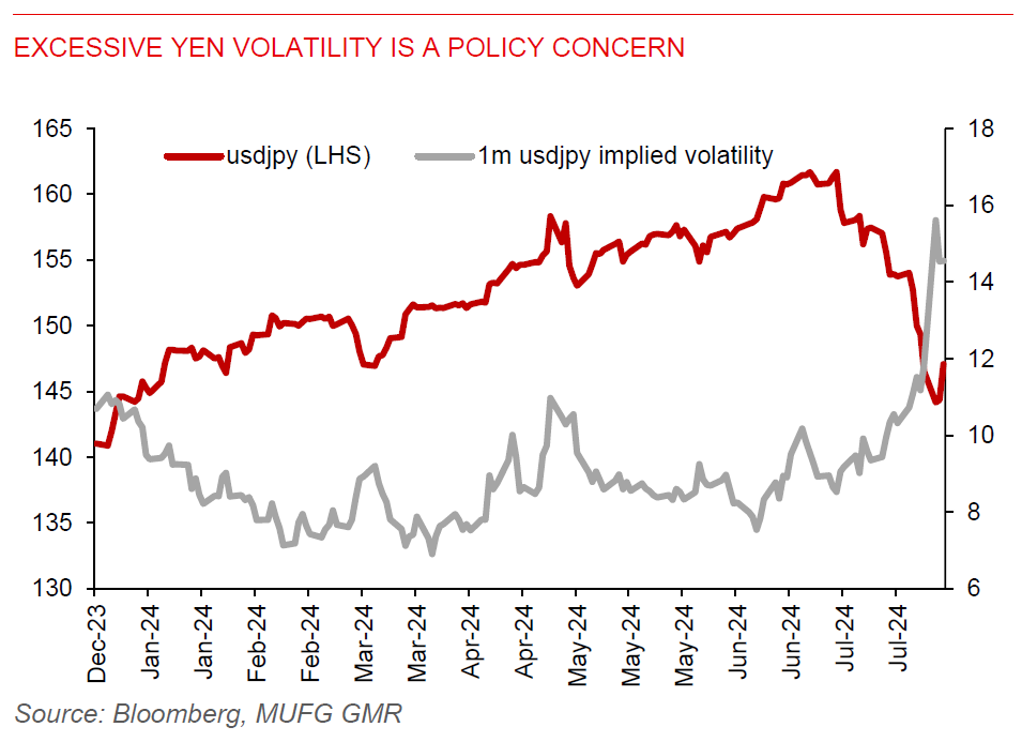

Excessive yen volatility has led to a tweak in Bank of Japan’s narrative, with Deputy governor Uchida pledging that the central bank will not raise the policy rate when markets are disorderly. This has helped stalled the sharp unwinding of the yen carry trade, with USDJPY hovering around the 145-level, US treasury yields stabilising slightly under 4%, and the broad DXY US dollar index ticking higher for a second straight day to recapture the 103-level.

We think USDJPY is probably trading around levels where real yield differentials would suggest. A safe-haven flight to the yen could still lead to further potential yen strength. But we are of the view that a sharp drop in US long-term yields will be a necessary condition for the yen to push below the 140.00-level versus the US dollar.

Meanwhile, oil prices have dropped below $80/barrel, with markets focusing on US recession risks. But geopolitical risks in the Middle East have also been rising. The appointment of hard-liner Sinwar – responsible for masterminding the October 7 attack on Israel – as the new political leader of Hamas militant group, delivers the latest blow to concerted multilateral efforts for forging a truce in Gaza. A scenario of a full-blown regional war in the Middle East could push up oil prices sharply. The Strait of Hormuz is a major shipping route accounting for almost 30% of global oil trade.

Regional FX

Asia currencies had a mixed performance versus the US dollar. IDR gained 0.8% to trade towards the 16000-level per US dollar, partly underpinned by bond inflows and a rise in the foreign reserves. But global volatility could limit the extent of rupiah strength. PHP also extended gains as an above-target inflation in July have pared back BSP rate cut bets. On the other hand, CNH fell for a second day (-0.2%) yesterday on the back of disappointing export data. Chinese exports rose 7%yoy, partly due to low base effects from a year ago and missing market expectations of 9.5%yoy. Exports also likely slowed on a month-on-month basis. MYR and THB – the region’s recent outperformer – have partially reversed their recent gains.