Key Points

Please click on download PDF above for full report.

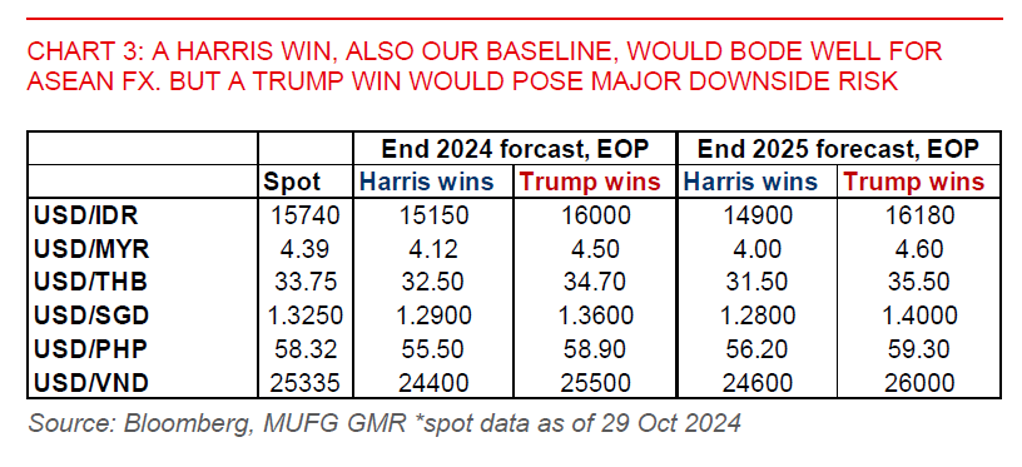

- ASEAN economies have been resilient, underpinned by exports and investment. But the 2025 outlook is subject to the US presidential election outcome this November. Our positive ASEAN outlook is predicated on a Kamala Harris victory, where we anticipate no major escalation of trade tariffs. If Harris wins, we look for markets to quickly unwind their “Trump trades” and re-focus on the positive impact from US rate cuts on ASEAN growth, bonds, and FX.

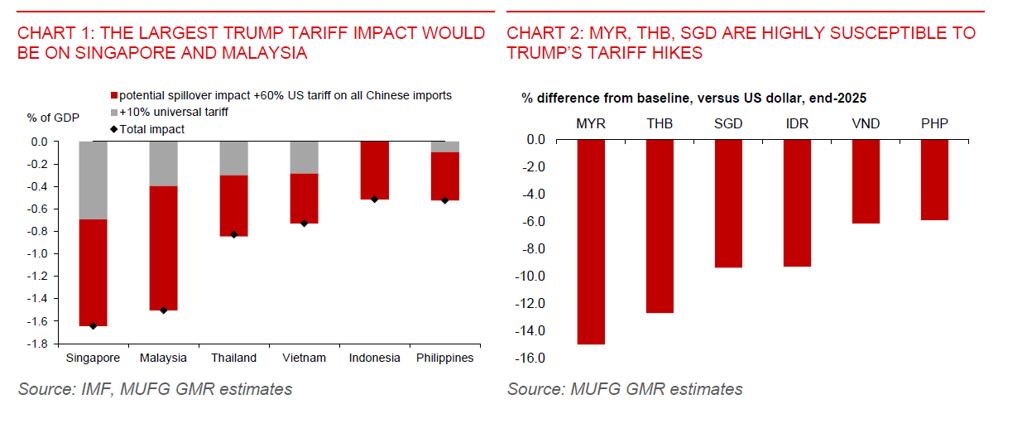

- A victory for Trump would likely hurt the outlook for ASEAN economies and FX. We anticipate that there are significant US tariff hikes on US imports from China, which will hurt Chinese demand with second round effects via lower business confidence. ASEAN’s fortunes are intertwined with China, so there would be huge negative spillover impact on ASEAN economies, mainly via lower trade and investment. Vietnam’s electronics exports to the US could also be targeted by Trump, in a bid to halt the diversion of Chinese electronic products to the US via Vietnam since 2018, while a blanket 10% US tariff hike on everyone else would amplify the shock.

- We estimate the largest negative growth impact from Trump’s onerous tariff hikes in the ASEAN region would be on Singapore (-1.6ppt) and Malaysia (-1.5ppt), given their higher export exposure to both the Chinese and US markets, as well as sensitivity to US tariffs and the negative shock on China’s investment demand. This is followed by Thailand (-0.8ppt), Vietnam (-0.7ppt), Indonesia (-0.5ppt), and the Philippines (-0.5ppt). Indonesia is surprisingly the most integrated with Chinese producers, yet the impact would be smaller, as it is still a more domestic-oriented economy.

- Trade diversion may only provide a limited offset this time. But ASEAN could still net benefit over the medium term from supply chain restructuring and global FDI shift towards ASEAN. Supply chain restructuring is happening at the sectoral level. This shift could accelerate and become structural in a Trump scenario. US imports across strategic sectors (e.g. electrical and mechanical machinery including semiconductor devices) from China have declined since 2018, while increasing sharply in Vietnam, Thailand, and several other economies. Procurement sources and FDI inflows have also notably shifted away from China towards ASEAN as firms diversify their risks.

- A Trump scenario would lead to weaker ASEAN currencies against the US dollar. This will mainly be driven by the Fed keeping interest rates higher than our baseline expectation, given the inflationary consequences of his proposed economic policies (tariffs + wider fiscal deficits). Mapping our analysis of the potential impact of Trump’s tariff on ASEAN FX, we expect larger depreciatory pressure on MYR, THB, and SGD, given the larger tariff impact on them and lower yields versus the US in the case of MYR and THB. The rupiah would also be highly vulnerable in a sustained period of US dollar strength and elevated US rates. A hit to Vietnamese electronics exports would also hurt the VND. PHP would also be affected, but likely less so.

- Currency weakness in a Trump scenario would be a particular constraint for Bank Indonesia and Bangko ng Sentral Pilipinas (BSP). BI and BSP could cut rates slower than we had expected and have a higher neutral rate, as they watch for FX stability. It would also affect other regional central banks, but likely less so. Growth could be hit hard in Singapore, Malaysia, and Thailand, prompting their central banks to ease monetary policy while allowing for a weaker currency.