Week Ahead FX outlook:

Major currencies in Asia continued to strengthen against the dollar this week, despite some recovery of the dollar’s value. Next week, eyes are on US data, mostly. US August nonfarm payroll and unemployment rate will be released on 6 September, the last jobs data points before the September FOMC meeting on 17-18 September.

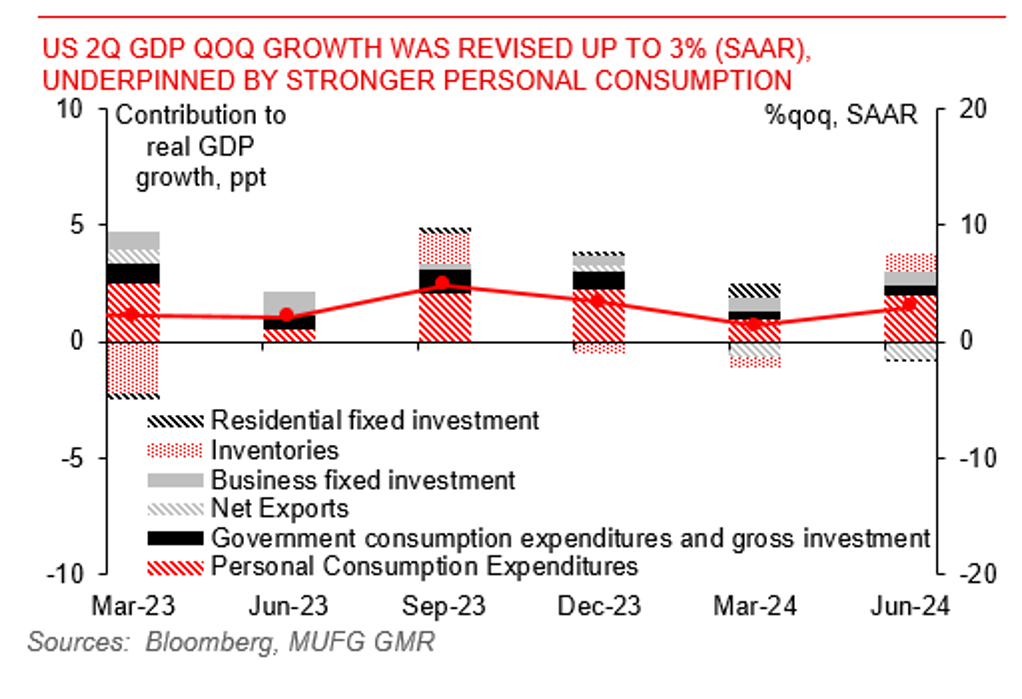

This week, US data releases indicated a more resilient US real economy, compared with Bloomberg consensus forecasts. This week, the second estimate for US GDP was revised up to 3%qoq from prior 2.8%qoq, underpinned by stronger personal consumption, which was revised up to 2.9%qoq from prior 2.3%qoq. Also, US July personal income grew by a faster than expected 0.3%yoy (vs prior 0.2%yoy and consensus 0.2%yoy), real personal spending growth also accelerated to 0.4%yoy in July up from June’s 0.2%yoy. What more positive was that PCE price and core PCE price inflations actually remained at low rate this July and unchanged from June’s value. This combination of resilient US real economy and muted price pressures itself may justify an “not so aggressive” rate cut by Fed this September.

Next week, major data for Asian economy will be announced, including the services and manufacturing PMIs. The new orders sub-index for South Korea’s and Taiwan’s manufacturing activity could shed some light on the sustainability of global tech cycle. While Chinese government plans to allow households to refinance mortgage loans, according to unconfirmed news, more firms are revising China’s 2024 GDP growth forecasts lower lately, the potential re-focusing on China’s fundamentals and property sector performance in August could limit CNY’s performance.

US 2Q GDP QOQ GROWTH WAS REVISED UP TO 3% (SAAR)