Week Ahead FX outlook:

Asian FX and rates markets are pre-occupied with upcoming event risks, chief of which is the US Elections and what a possible Trump Presidency and his proposed tariffs may imply for growth and interest rates. In addition, Japan will also be holding its Lower House Elections on 27 October this weekend. A larger than expected loss by the incumbent LDP-Komeito coalition could increase the chance of PM Ishiba losing his Premiership and as such political uncertainty, even as we stress this is not our base case.

Regardless of who wins in the US Elections, the broader context is the inexorable shift towards a multi-polar world, and with that the geoeconomic fragmentation that comes with it and the likelihood for trade and FDI to detach further along geopolitical blocs. Nonetheless, Asian economies are certainly not standing still. In China, we could see further announcements on fiscal stimulus and fiscal deficit targets in the upcoming National People’s Standing Committee meeting, recently announced to be held from 4-8 November. A Trump victory may increase the probability of more economic support by Chinese authorities in anticipation of disruptive policies. Meanwhile, China’s President Xi Jinping and Indian Prime Minister Narendra Modi met for the first time since 2022 on the sidelines of the BRICS summit, with a temporary détente reached on border issues. Several Southeast Asian economies – Malaysia, Indonesia, Vietnam and Thailand – have also become partner countries of BRICS, with Malaysia and Thailand in particular looking to become full-fledged members in time to come.

Looking to the week ahead, we will have US non-farm payrolls, the Bank of Japan monetary policy meeting, China’s manufacturing PMIs, coupled with Taiwan’s GDP. For the BOJ in particular, we are expecting the central bank to remain on hold and to likely reiterate its stance that it has time on its side for now. The NFP print will be important in the lead up to the Fed’s policy meeting on 8 Nov (Asia time) and also US Elections.

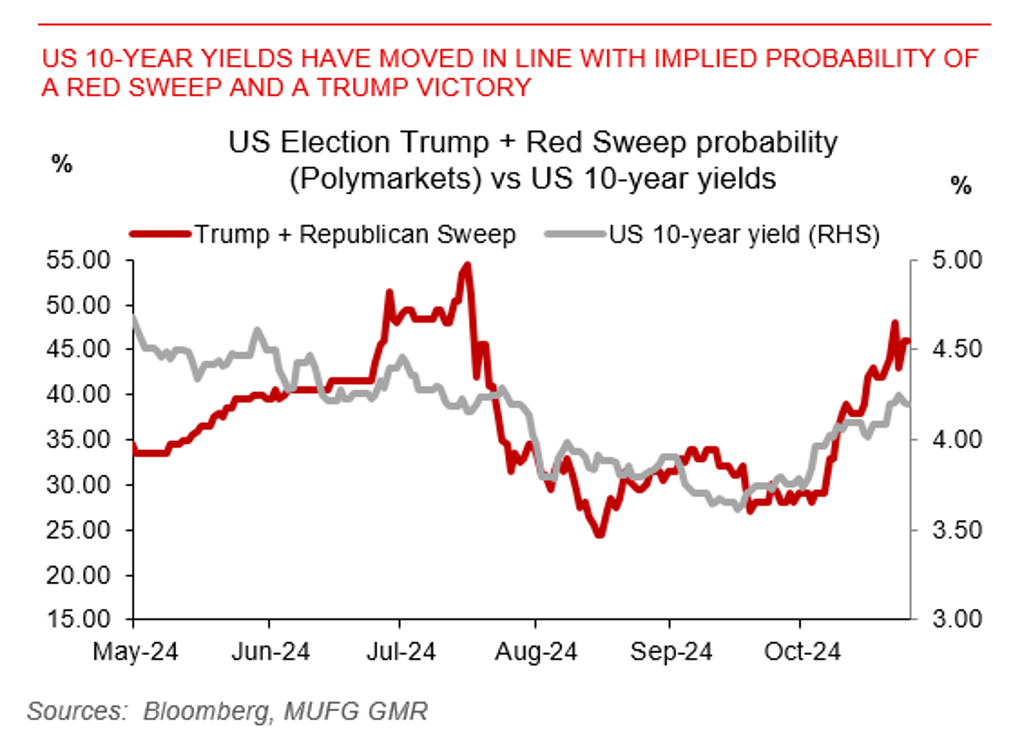

US 10-year yields have moved in line with implied probability of a Red sweep and a Trump victory