Week Ahead FX outlook:

Key FX views:

Asia’s macro and FX this week has been dominated by the interaction of rising US yields, renewed geopolitical risk and data releases of Asian economies, resulting in a consolidation of Asia FXs and certain uneven pressure, for currency like KRW and IDR particularly. It is not a new story that oil shock weights on Asian currencies, but a lingering oil shock could expose individual economy’s unique weakness, fiscal conditions/policy constraints, and even cause sovereign risk pricing and push for strong capital outflow. Additionally, the exports control policy added another layer for recent IDR’s weakness too. In contrast, the Chinese yuan has remained relatively more stable, despite that PBOC had been setting a weaker fixing and China’s latest April macro numbers offered a clear negative surprise, compared with the market consensus views.

On the macro side, recent data continues to point to resilient but uneven growth across Asia, with a clear divergence between external and domestic demand. Japan’s 1Q GDP surprised on the upside (+0.5%qoq vs consensus ~0.4%qoq), highlighting still-solid momentum before the full impact of higher energy costs. China’s April data indicated a weakened domestic demand, with growth decelerations seen in IP, sales, FAI and property investment, while exports being the only major silver lining which grew by a strong 14.1%yoy in April. Across ASEAN, Malaysia’s April CPI inflation edged a bit up, and its exports growth accelerated strongly in April. Increasingly exposed to higher import costs and weaker real incomes likely, we expect continued transmission from high oil prices to broad CPI prices, and higher stress on Asian economy. This has left policymakers in a difficult position, balancing currency stability and inflation risks against the need to support growth. BI hiked its policy rate by 50bps on 20 May.

Next week,with the May 28 cluster of US GDP, PCE and income/spending, and other data including US consumer confidence, EU/Germany CPI, and China PMIs at week‑end shape the growth‑inflation narrative. For Asia FX, a strong US growth/inflation print would reinforce higher US yields and renew pressure on Asian FX, while softer data could trigger USD consolidation and unwind some pressure on Asian FXs. No BOK rate change expected

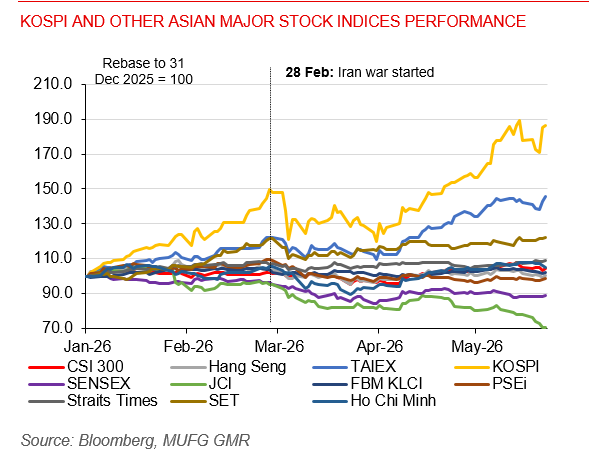

KOSPI and other asian major stock indices performance