US dollar & yen strengthen as risk aversion intensifies

USD: Growth concerns & geopolitics lift the dollar ahead of jobs data

The dollar strengthened yesterday despite the clearest signal yet from the FOMC that the rate cut is a plausible scenario at the next FOMC meeting in September. Yields fell again yesterday and now in just three trading days, the 2-year yield is down 25bps. The fact that the US dollar (bar VS JPY of course!) advanced yesterday indicates there are broader factors at play here beyond simply US macro and rate expectations.

One obvious near-term development that could be providing some support is increased geopolitical risks. The markets await possible retaliation by Iran and/or Hezbollah following the Israel attacks in Beirut and Iran that killed senior Hamas and Hezbollah members. While an escalation in the Israel conflict would be bad news for sentiment we don’t see this as the primary driver of market moves yesterday. For Middle East risks to escalate and impact sentiment one would expect crude oil to be part of that, but crude oil prices declined yesterday. Escalation of the conflict would primarily benefit Israel and hence is unlikely to happen and any retaliation by Iran or Hezbollah will be more for show than anything meaningful that would lead to a widening of the conflict in the region.

Crude oil prices are now down between 8-9% from the closing high in early July and this price action is probably more reflective of what is now supporting the US dollar despite falling US yields – concerns over weakening global growth and linked to that in part concerns over the Fed possibly falling behind the curve. Not so long ago, news from the Fed that it was putting a rate cut on the table would have been greeted with cheer from investors – but not this time. US small caps have underperformed highlighting domestic growth concerns. The Russell 2000 is down 3.4% since the FOMC announcement while the S&P 500 is down 1.3%.

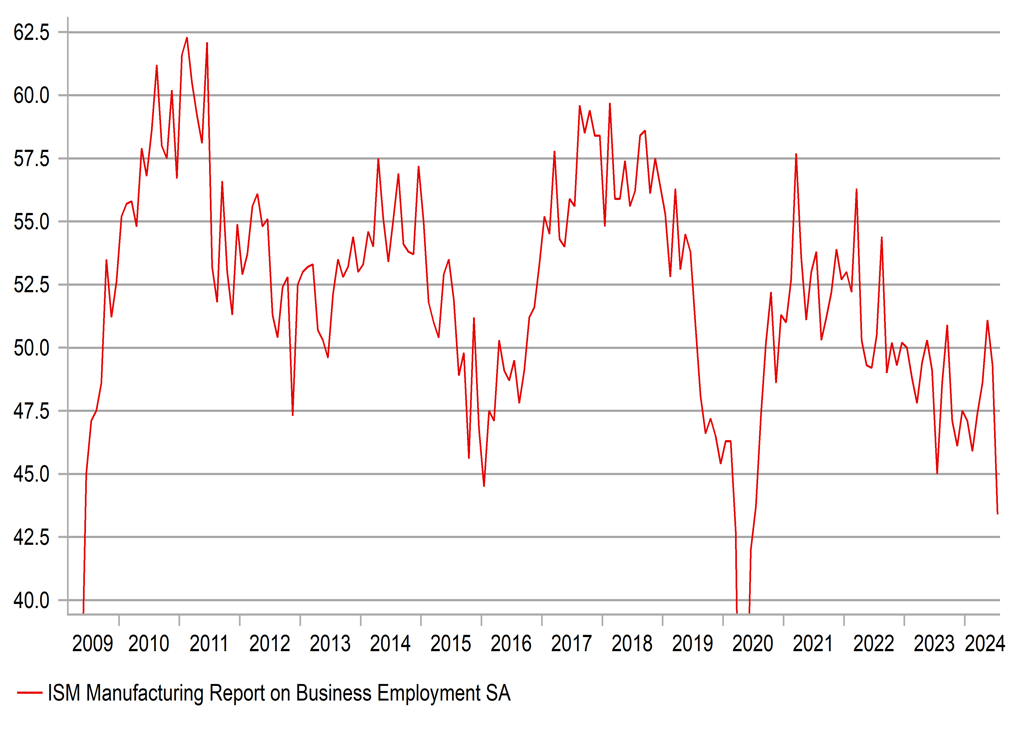

So bad news may no longer be good news from a risk perspective which certainly may provide added bias to the upside for the dollar. Certainly the data yesterday was bad enough to have usually weakened the dollar. The ISM manufacturing employment index fell to 43.4, a terrible reading and the biggest one-month drop (from 49.3) since April 2020 as covid hit the jobs market hardest. Initial claims data too pointed to a weakening labour market. We would still expect the dollar to weaken if the NFP today was weaker than expected but it would be surprising now to see a sharp dollar sell-off given the global backdrop that is resulting in front-end yields falling notably (BoE rate cut, soft inflation in Australia, weak Caixin from China) in many countries and given the increased geopolitical risk concerns going into the weekend.

ISM EMPLOYMENT INDEX FELL TO A NEW LOW – EXCLUDING COVID THE LOWEST LEVEL SINCE THE GFC BACK IN 2009

Source: Macrobond & MUFG GMR

JPY: Sharp drop in Japan equities as yen gains further

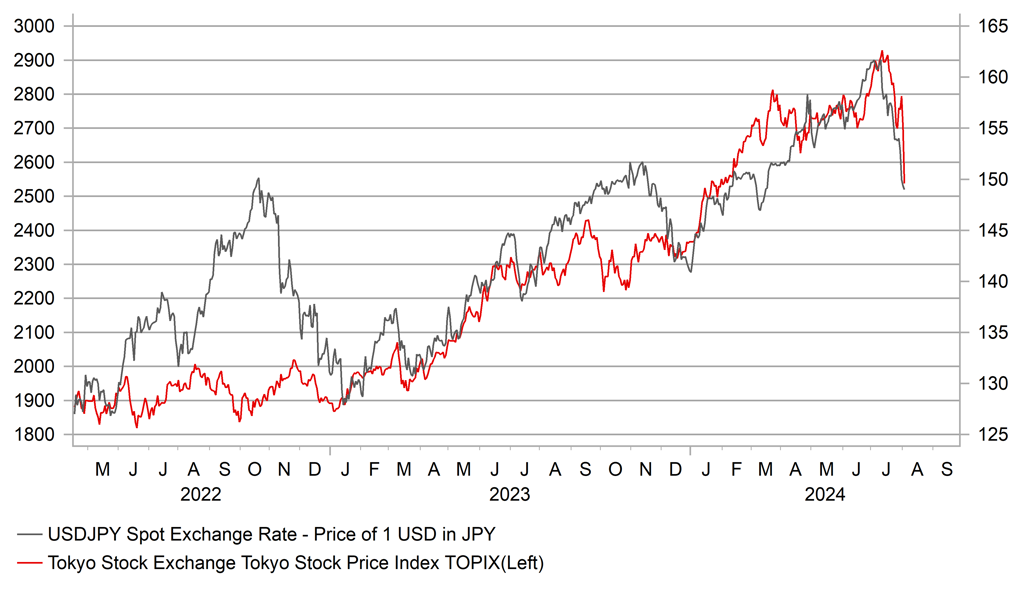

The weak yen trend since early 2022 helped fuel the strong rally in Japanese equities and the reversal of yen weakness is now having a significant impact on Japan equity market performance. The Topix Index closed down 6.1% after the yen took another leg stronger into the New York close yesterday. After hitting a closing high on 11th July, the Topix Index today is set to close at the lowest level since February.

This remarkable swing indicates that market participants are now taking on board the significance of the BoJ monetary policy meeting on Wednesday with the hawkishness of Governor Kuroda underlining the prospect of more hikes to come. Of course it will be argued that if this correction in equities was to continue that it would likely threaten the ability of the BoJ to carry on lifting the policy rate.

While we would argue that the fundamental story in Japan that has turned much more favourable in pointing to an end to mild deflation had very little to do with FX, the liquidation of positions can still do damage if large enough. This is very likely foreign investor led given the turn of the yen, the deteriorating global sentiment outlined above and the fact that the flow data had already started to indicate a turn in sentiment. The weekly flow data released yesterday for last week revealed foreign investor selling of Japan equities totalling JPY 671bn, the largest weekly selling by foreign investors since March. The problem here is that the link between equities and the yen can intensify with one leading the other and then vice-versa. Given the dire yen sentiment over the last two years and given a foreign investor gets paid to hedge yen downside risks, the plunge in equities now may mean foreign investors are over-hedged which could mean the yen buying momentum is reinforced as short yen hedges are unwound.

Key now will be what happens to US yields. As we always highlight, while the BoJ move is important, the bigger variable in the US-JP yield spread is the Fed. This move in USD/JPY more broadly speaking is due to the big drop in US front-end yields, down 60bps now since the beginning of July and approaching 100bps in the last three months. The authorities in Japan though will no doubt be nervous and those in the markets over 20yrs (like me!) will certainly see some parallels here with 1998. Japan intervened to buy the yen in June 1998 then front-end US yields plunged as the Fed began cutting rates in September and then USD/JPY fell over 20 big figures in three trading days in October! However, we would argue there is a big difference now compared to 1998 – Japan is likely exiting 25yrs of mild deflation, not entering.

USD/JPY AND TOPIX INDEX SINCE THE START OF THE GLOBAL INFLATION SHOCK AND THE YEN SELL-OFF

Source: Macrobond, Bloomberg

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

NO |

09:00 |

Unemployment Change |

Jul |

-- |

75.00K |

! |

|

IT |

10:00 |

Italian Retail Sales (YoY) |

Jun |

-- |

0.4% |

! |

|

IT |

10:00 |

Italian Retail Sales (MoM) |

Jun |

0.2% |

0.4% |

! |

|

UK |

12:15 |

BoE MPC Member Pill Speaks |

-- |

-- |

-- |

!!!! |

|

US |

13:30 |

Nonfarm Payrolls |

Jul |

176K |

206K |

!!!!! |

|

US |

13:30 |

Private Nonfarm Payrolls |

Jul |

148K |

136K |

!!! |

|

US |

13:30 |

Average Hourly Earnings (YoY) (YoY) |

Jul |

3.7% |

3.9% |

!! |

|

US |

13:30 |

Average Hourly Earnings (MoM) |

Jul |

0.3% |

0.3% |

!!!! |

|

US |

13:30 |

Average Weekly Hours |

Jul |

34.3 |

34.3 |

! |

|

US |

13:30 |

Participation Rate |

Jul |

-- |

62.6% |

!! |

|

US |

13:30 |

U6 Unemployment Rate |

Jul |

-- |

7.4% |

!! |

|

US |

13:30 |

Unemployment Rate |

Jul |

4.1% |

4.1% |

!!!!! |

|

US |

15:00 |

Durables Excluding Defense (MoM) |

Jun |

-- |

-7.0% |

! |

|

US |

15:00 |

Durables Excluding Transport (MoM) |

Jun |

-- |

0.5% |

! |

|

US |

15:00 |

Factory Orders (MoM) |

Jun |

-2.7% |

-0.5% |

!! |

|

US |

15:00 |

Factory orders ex transportation (MoM) |

Jun |

-- |

-0.7% |

! |

|

US |

15:00 |

Total Vehicle Sales |

Jul |

-- |

15.30M |

! |

|

US |

17:00 |

Fed's Goolsbee on BBG TV |

!!! |

|||

|

US |

17:00 |

Fed's Barkin on US TV |

!!! |

Source: Bloomberg