Payrolls in focus as US dollar softens & yields decline

USD: Solid jobs growth expected

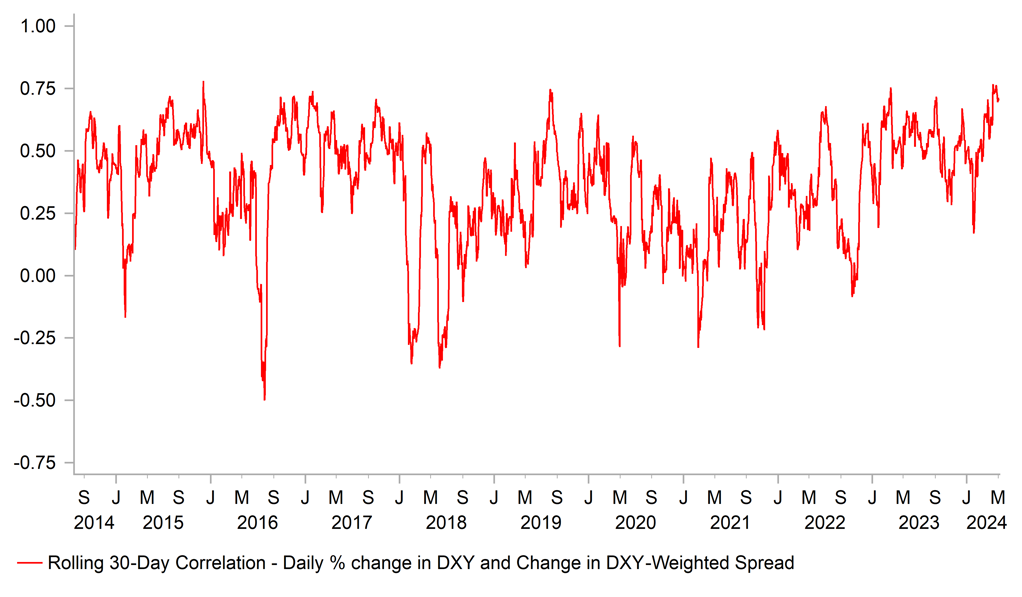

The consequences of the FOMC press conference by Fed Chair Powell has been clear to see with rate cut expectations brought slightly forward – a November rate cut is now fully priced with 20bps of cuts priced for September. As we stated here before it becomes a lot more difficult for hawkish rhetoric to lift yields when only one rate cut is priced by year-end. The 2-year UST note yield fell 8bps yesterday and is down 16bps from the peak on Monday and is at its lowest level since the day of the CPI data on 10th April. The 2yr yield spread correlation with DXY on a daily basis remains close to record highs above 0.70 and underlines the continued importance of incoming data and Fed policy expectations for the US dollar.

In that regard today brings us one of the two key data points of the month – the non-farm payrolls data. Powell this week indicated that with inflation still as high as it is, the jobs data would have to show considerable weakness in order for the Fed to cut rates. The consensus for today is a gain in NFP of 240k, down from 303k last month. Other incoming economic data has not indicated any marked deterioration in employment is imminent and hence it would be a big surprise to see a print today that was considerably weaker than expected. The ISM Manufacturing Employment index remains below the 50-level but has increased for two consecutive months. The JOLTS report continues to show the labour market becoming more balanced but with no sign of marked deterioration. The initial claims data too have been low and stable.

Still, the signs of weakness do remain and there is plenty of evidence to suggest the true health of the labour market is not as robust as implied by the NFP data. The Services Employment index will be released today but the past two months has seen the lowest two-month average since covid in 2020. The NFIB Hiring Plans index is also at levels last seen during covid although it did pick up in the last report from a new low of 11 to 12. We will be looking closely at the Household survey too today. It indicates much weaker employment conditions with full-time employment now down 1.35mn over the last 12mths – a scenario that has only happened during covid and before then the GFC. Finally Bloomberg analysis reported yesterday interestingly concluded that the latest Business Employment Dynamics report, released on 24th April, that will be used to revise 2023 NFP data indicated a far weaker labour market then. Q3 NFP revealed a gain of 494k but Bloomberg analysis of the BED report suggests a drop of 192k is what actually unfolded.

While incoming data does not suggest a notable deterioration in the data today, at some point we expect it to happen as rate hikes bite, covid-savings driven consumption fades and fiscal impetus weakens. With US yields where they are we’d expect a weaker print to garner a bigger reaction in both rates and FX.

2-YEAR DXY-WEIGHTED YIELD SPREAD CHANGE AND % CHANGE IN DXY CORRELATION REMAINS CLOSE TO A RECORD HIGH

Source: Macrobond, Bloomberg & MUFG Research

GBP: Dash for cash may have QT implications

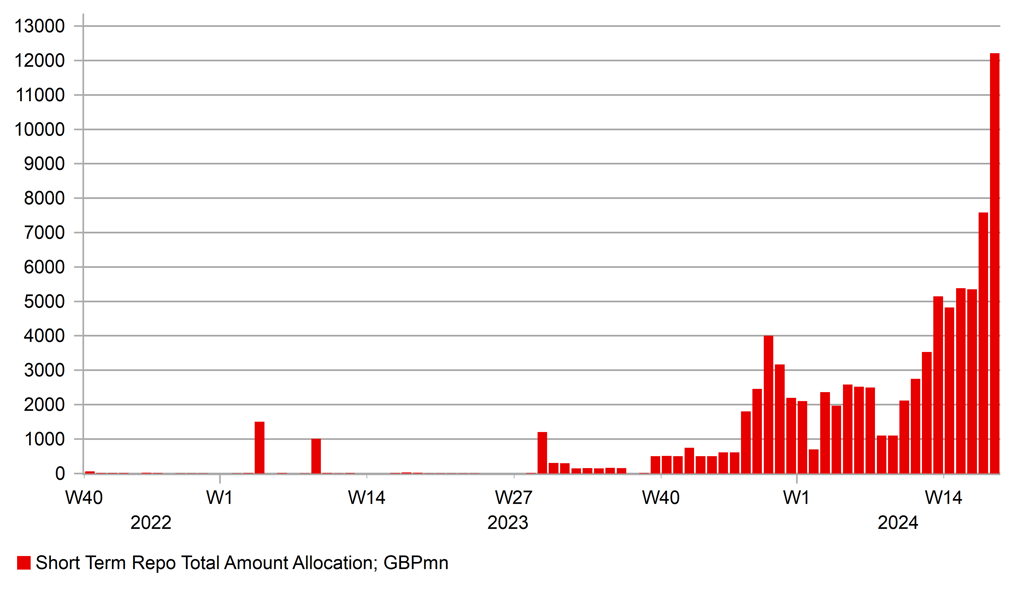

On the day following the FOMC’s decision to commence QT tapering by cutting the taper cap of US Treasury securities from USD 60bn to USD 25bn, effective from June, evidence is continuing to build in the UK that financial conditions are tightening and liquidity conditions have the potential to create increased short-term rate volatility going forward. Even if tighter cash conditions do not lead to any increased rates volatility, the shortage of cash and the potential upward pressure on rates would certainly be inconsistent with the MPC cutting rates. Nearly a full 25bp cut is priced by August.

However, it is not as clear-cut as with the Fed in predicting what the BoE might do. The Fed has always indicated an intention to halt QT at some ‘equilibrium’ level of reserves on the balance sheet. Indeed, the Fed may have reached such appoint in 2019 when the Fed announced a plan to increase purchases of T-bills in order to ensure ample reserves to help stabilise short-term rates.

In the case of the BoE there appears to be less support for maintaining such a large balance sheet and previously it has been signalled that the BoE could allow excess reserves to run right down to a “preferred minimum range of reserves”. A BoE official cited a BoE survey that revealed responses from banks put that range between GBP 335bn and GBP 495bn. Today that balance stands at GBP 770bn, implying a still considerable period of time to get to that range based on the current BoE policy of reducing asset holdings by GBP 100bn per year.

The next updated guidance on QT comes in September and if by then the MPC has cut rates and if the current signs of tight liquidity continues there may be a change considered. Certainly any complication in the transmission of monetary policy would increase pressure for QT to be tapered. In the meantime, the BoE will likely be investigating to assess why this demand for cash is surging at a time when reserves are viewed as considerably above the previously reported equilibrium level.

We doubt these developments have much implications for GBP performance. We are still a way off any change in QT policy. Nonetheless, if demand for cash continues to rise and QT tapering speculation builds, it may help dampen Gilt yields which all-else-equal would be GBP negative.

BOE SHORT-TERM REPO OPERATION USAGE

Source: Macrobond & Bloomberg

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

IT |

09:00 |

Italian Monthly Unemployment Rate |

Mar |

7.5% |

7.5% |

! |

|

NO |

09:00 |

Interest Rate Decision |

-- |

-- |

4.50% |

!! |

|

UK |

09:30 |

Composite PMI |

Apr |

54.0 |

52.8 |

!!! |

|

UK |

09:30 |

Services PMI |

Apr |

54.9 |

53.1 |

!!! |

|

EC |

10:00 |

Unemployment Rate |

Mar |

6.5% |

6.5% |

!! |

|

US |

13:30 |

Average Hourly Earnings (YoY) (YoY) |

Apr |

4.0% |

4.1% |

!! |

|

US |

13:30 |

Average Hourly Earnings (MoM) |

Apr |

0.3% |

0.3% |

!!!! |

|

US |

13:30 |

Average Weekly Hours |

Apr |

34.4 |

34.4 |

! |

|

US |

13:30 |

Nonfarm Payrolls |

Apr |

243K |

303K |

!!!! |

|

US |

13:30 |

Private Nonfarm Payrolls |

Apr |

180K |

232K |

!! |

|

US |

13:30 |

Unemployment Rate |

Apr |

3.8% |

3.8% |

!!!! |

|

US |

14:45 |

S&P Global Composite PMI |

Apr |

50.9 |

52.1 |

!! |

|

US |

14:45 |

Services PMI |

Apr |

50.9 |

51.7 |

!!! |

|

US |

15:00 |

ISM Non-Manufacturing PMI |

Apr |

52.0 |

51.4 |

!!! |

Source: Bloomberg