Key payrolls report with markets split on size of 1st FOMC rate cut

USD: Data this week lifting expectations of a 50bp cut

The US dollar is down 1.0% now from the high recorded on Tuesday and the data flow and Fed communications have lifted prospects of the Fed cutting rates by 50bps at the meeting on 18th September. The OIS market is now close to 50-50 on the pricing of the cut being 50bps rather than 25bps. The weaker JOLTS report on Wednesday was followed yesterday by the ADP employment report which was weaker than expected while the ISM Employment index was also slightly softer than expected.

The communications from Fed officials though in our view continue to indicate that the FOMC will likely be open to a larger cut if the employment market was to worsen further. San Francisco Fed President Mary Daly stated in a podcast with the Wall Street Journal that while the speed of cutting rates is unknown, further evidence of labour market weakness would be “unwelcomed”. Chicago Fed President in a separate interview spoke of the “mounting warning signs” from the labour market and that inflation “is coming down very significantly” and that multiple rate cuts will be required. Again, our sense of his comments were that concerns over the labour market have been increasing and hence we are likely to get a considerable change in the Summary of Economic Projections at that meeting that could certainly provide the justification for a larger 50bp rate cut.

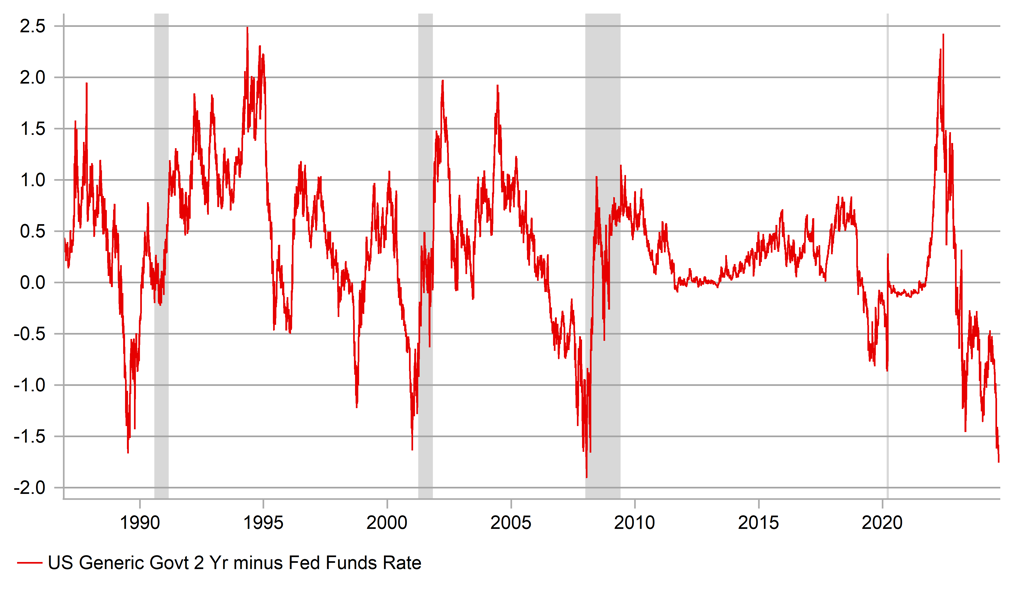

As stated earlier this week, the current SEP forecasts show the unemployment rate at 4.0% and the core PCE inflation at 2.8% by the end of this year and hence will justify forecast changes and hence a median dot profile with much more easing indicated than in June. But the scale of change will still be dependent to some degree on the payrolls report today. This jobs report certainly feels to be one in which it could trigger considerable moves either way in front-end yields and the dollar. The 2-year UST note yield is down 23bps from the high on Tuesday with the spread to the fed funds -176bps, the widest since January 2008 heading into the GFC. There is a lot of easing priced into the 2-year yield now and suggests a stronger than expected report could prompt a larger rebound in the 2-year yield than a weaker report would push yields lower.

From an FX perspective, that would certainly result in some recovery for the dollar. The impact on equity markets from another weak report will likely shape how the dollar responds. A very weak report that hits equity markets notably would likely see the dollar perform better versus high-beta G10. We’d see the best prospects for the yen and Swiss franc and to a degree the euro. The yen (+2.7%); the Swiss franc (+0.9%) and the euro (0.6%) are the three best performing G10 currencies this week and that indicates that FX is positioned more for risks of a weak report like in the Treasury bond market. Despite the yen gains already recorded, we would still expect further notable gains on increased prospects of a 50bp cut from the FOMC and would imply scope for USD/JPY to trade into the 130’s over the coming days and weeks. Long USD/JPY was the most popular global inflation trade in FX and the change in that macro backdrop will ensure USD/JPY continues to reverse the 2022-2024 near-40% rally.

2-YEAR – FED FUNDS SPREAD MOST NEGATIVE SINCE JUST BEFORE GFC

Source: Macrobond & Bloomberg

EUR: Macron picks a PM with limited reaction

President Macron announced yesterday the appointment of Michel Barnier as his new prime minister which came nearly two months to the day after the second round of parliamentary elections on 7th July. The post-election gridlock since meant naming a PM was always going to be difficult. Michel Barnier, from Les Republicans party will have two key tasks ahead – the first to form a cabinet that avoids a no-confidence motion and submitting a budget to parliament by the deadline of 1st October.

The choice does initially look like a reasonable one. Barnier ran in the presidential primaries in 2021 on a policy platform that some called ‘hard-right’. Some policies would have breached EU law like a moratorium on immigration to freeze the arrival of immigrants in France and a “constitutional shield” to lock down migration policy to decide annual visa quotas. So on the policies of immigration he could find some common ground with RN.

The President of RN, Jordan Bardella stated on X that RN “will judge his policy decisions, and his actions”. He added that RN’s policies on purchasing power, security and immigration needed to be addressed and that RN “reserved all political means of action if these are not taken into account”. So it does seem given the far-left will oppose the choice of Bernier as PM that RN will have the ultimate control on whether a no-confidence motion would prove successful going forward.

The lack of reaction in the financial markets is understandable. In a way, the choice of a PM was the easier first step and the greater challenges will be making progress in terms of forming a government and proposing a budget that can pass parliament without triggering a no-confidence motion. The RN will likely reserve judgement and Marine Le Pen has stated that a policy speech to parliament will be a key event (no fixed date yet). For the financial markets the take on this is likely that we were in gridlock before the Barnier announcement and we are still likely in gridlock now with Barnier faced with very difficult tasks. In that sense OATs and the Bund/OAT spread may well take more direction from incoming US economic data and the prospect of the first rate cut from the Fed on 18th September. Similarly, the impact on the euro from politics in Europe will likely remain limited for now.

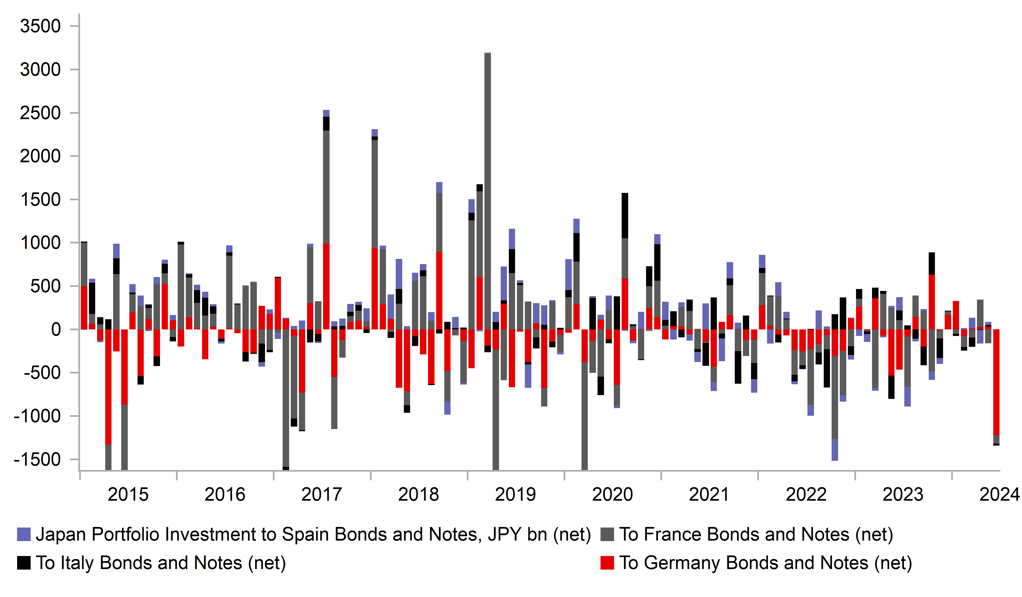

JAPANESE INVESTORS WERE HEAVY SELLERS OF GERMAN BONDS IN JUNE – A POSSIBLE SIGN OF CONCERN AFTER THE EU ELECTIONS

Source: Macrobond & Bloomberg

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

08:00 |

ECB's Elderson Speaks |

-- |

-- |

-- |

!! |

|

IT |

09:00 |

Italian Retail Sales (MoM) |

Jul |

0.1% |

-0.2% |

! |

|

IT |

09:00 |

Italian Retail Sales (YoY) |

Jul |

-- |

-1.0% |

! |

|

EC |

10:00 |

Employment Change (QoQ) |

Q2 |

0.2% |

0.3% |

! |

|

EC |

10:00 |

GDP (QoQ) |

Q2 |

0.3% |

0.3% |

!! |

|

EC |

10:00 |

GDP (YoY) |

Q2 |

0.6% |

0.4% |

!! |

|

US |

13:30 |

Nonfarm Payrolls |

Aug |

164K |

114K |

!!!!! |

|

US |

13:30 |

Unemployment Rate |

Aug |

4.2% |

4.3% |

!!!!! |

|

US |

13:30 |

Average Hourly Earnings (YoY) (YoY) |

Aug |

3.7% |

3.6% |

!! |

|

US |

13:30 |

Average Hourly Earnings (MoM) |

Aug |

0.3% |

0.2% |

!!!! |

|

US |

13:30 |

Average Weekly Hours |

Aug |

34.3 |

34.2 |

! |

|

US |

13:30 |

U6 Unemployment Rate |

Aug |

-- |

7.8% |

!! |

|

CA |

13:30 |

Avg hourly wages Permanent employee |

Aug |

-- |

5.2% |

! |

|

CA |

13:30 |

Employment Change |

Aug |

25.6K |

-2.8K |

!!! |

|

CA |

13:30 |

Participation Rate |

Aug |

-- |

65.0% |

! |

|

CA |

13:30 |

Unemployment Rate |

Aug |

6.5% |

6.4% |

!!! |

|

US |

13:45 |

FOMC Member Williams Speaks |

-- |

-- |

-- |

!!!! |

|

US |

15:00 |

Total Vehicle Sales |

Aug |

15.40M |

15.80M |

! |

|

CA |

15:00 |

Ivey PMI |

Aug |

55.3 |

57.6 |

!! |

|

US |

16:00 |

Fed Waller Speaks |

-- |

-- |

-- |

!!!! |

Source: Bloomberg