From ECB to payrolls – our bias is to the upside for EUR/USD

EUR: Upside scope is building

The ECB 25bp rate cut and communications yesterday were broadly in line with consensus and was covered in an FX Focus piece yesterday (here) and the level of caution on future rate cuts was enough to provide ongoing support for the euro. The data-dependency guidance will certainly increase the sensitivity of rates and FX moves around key data releases. Governing Council member Holzmann dissented for the very reason that recent data meant a cut was not justified. With EUR/USD higher after yesterday’s rate cut, whether this move can extend further to possible test the 1.1000-level will very much depend on the key US jobs report this afternoon.

The consensus for today is for an increase in non-farm payrolls of 180k, up modestly from the 175k gain last month. The average hourly earnings annual growth rate is expected to remain at 3.9% with a MoM increase of 0.3%. A lot of the incoming employment-related data has been showing labour market slowdown and hence a consensus print this afternoon may well be met with some relief that could propel the US dollar and yields modestly higher. In five trading days to Wednesday, the 2-year UST note yield is down 25bps and the dollar has declined by close to 1.0%. There is certainly some increased expectations of slower growth that a consensus print today would at least partially reverse.

But as each and every month passes with other jobs-related data showing deceleration, there is certainly an increasing risk that this will eventually become more clearly evident in the key NFP data. Whether that’s today or over the months ahead, the risks are rising that we see the labour market finally begin to crack. The JOLTS report this week along with the ISM Services Employment index are the latest data points to showing softening demand. Any weakness today could well sway the FOMC to lean to a median dots profile of two rate cuts this year rather than just one.

That would help keep front-end yields under downward pressure. The 2-year EZ-US swap spread has narrowed to 128bps, the narrowest since March when EUR/USD last traded over 1.0900 and down 20bps since 28th May. Any surprise weakness today could be enough to propel EUR/USD higher to test the key 1.1000-level.

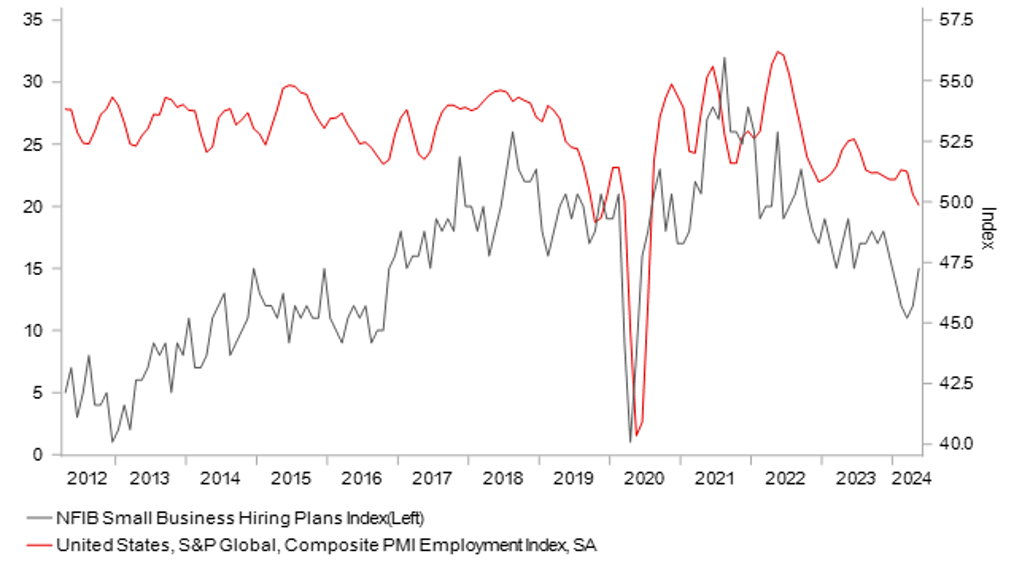

PMI COMPOSITE EMPLOYMENT INDEX AND NFIB HIRING PLANS ARE BOTH DETERIROATING TO LEVELS CONSISTENT WITH SLOWER NFP GAINS

Source: Bloomberg, Macrobond & MUFG GMR

EUR: Elections unlikely to have much impact

The European parliament elections have officially begun with the Netherlands voting yesterday. All 27 EU countries will go to the polls through to Sunday with 373mn Europeans eligible to vote with those voters electing 720 lawmakers to parliament. Exit polls in the Netherlands released last night revealed that Geert Wilders’ far-right Party for Freedom has won seven seats in the election with the centre-left alliance winning eight seats. The seven-seat win for Party for Freedom is a big gain on the one seat from the last election and likely signals more of the same to come across Europe.

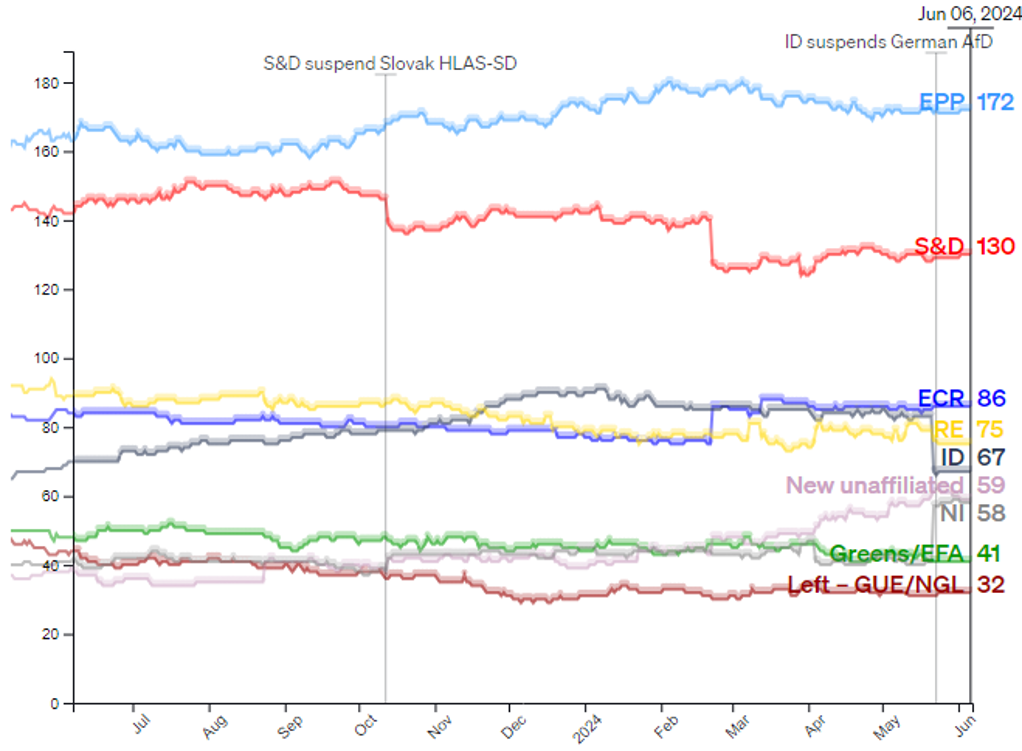

The above Poll of Polls chart from Politico indicates that the moderate centre-right party (EPP) and moderate centre-left party (S&D) will be the two largest parties. However, there influence has been steadily eroded over recent parliaments as periphery parties advance. A further notable advance for the periphery parties (in particular the far-right) is likely going to be the key takeaway from these elections and should become clear early next week as results start to come in. The European political system is pretty complicated and hence there’s never a clear immediate takeaway from an EU election result that triggers in a financial market reaction.

That’s likely to be the case again and certainly from a macro perspective it is difficult to ascertain any discernible impact. We are going to see a clear shift to the right however and the bias in direction of policy change will almost certainly be in favour of less momentum in regard to green policies with the far-right parties far less supportive and campaigning on the view that climate change policies have gone too far.

There may also be less momentum in the direction of greater EU integration. This is certainly bad news given the need for further steps in favour of reducing barriers to services trade and the need for greater capital markets integration. There will certainly be a greater focus on controlling immigration.

Dealing with China and trade policy is led by the EU Commission President – Ursla Von der Leyen and while she remains the candidate of the EPP for presidency, the ultimate decision rests with the European Council – the leaders of each EU member country. We would assume policy continuity here although many far-right parties have turned away from Russia (for obvious reasons) but instead have turned more favourable toward China. That could ultimately complicate the EU-US relationship on trade, especially if Trump is in the White House.

If there is to be an FX reaction next week, it would possibly be in response to a stronger than expected showing for National Rally and Marine Le Pen. Her party is currently polling at 33% well ahead of Ensemble (Macron’s party) on 15%. The next presidential election in France is not until April 2027 but a stronger than expected result will increase fears of more meaningfully bad election results over the coming years.

EU ELECTION OPINION POLLING FOR MAIN POLITICAL PARTY GROUPS

Source: Politico.eu as of 6th June 2024

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

SZ |

08:00 |

Foreign Reserves (USD) |

May |

-- |

720.4B |

! |

|

CH |

09:00 |

FX Reserves (USD) |

May |

3.210T |

3.201T |

! |

|

EC |

09:00 |

ECB's Schnabel Speaks |

-- |

-- |

-- |

!!! |

|

EC |

10:00 |

Employment Change (QoQ) |

Q1 |

0.3% |

0.3% |

! |

|

EC |

10:00 |

GDP (QoQ) |

Q1 |

0.3% |

0.0% |

!! |

|

EC |

10:00 |

GDP (YoY) |

-- |

0.4% |

0.1% |

!! |

|

US |

13:30 |

Nonfarm Payrolls |

May |

186K |

175K |

!!!!! |

|

US |

13:30 |

Average Hourly Earnings (YoY) (YoY) |

May |

3.9% |

3.9% |

!!! |

|

US |

13:30 |

Average Hourly Earnings (MoM) |

May |

0.3% |

0.2% |

!!!! |

|

US |

13:30 |

Average Weekly Hours |

May |

34.3 |

34.3 |

! |

|

US |

13:30 |

Participation Rate |

May |

-- |

62.7% |

!! |

|

US |

13:30 |

U6 Unemployment Rate |

May |

-- |

7.4% |

!! |

|

US |

13:30 |

Unemployment Rate |

May |

3.9% |

3.9% |

!!!! |

|

CA |

13:30 |

Avg hourly wages Permanent employee |

May |

-- |

4.8% |

! |

|

CA |

13:30 |

Employment Change |

May |

27.8K |

90.4K |

!!! |

|

CA |

13:30 |

Participation Rate |

May |

-- |

65.4% |

! |

|

CA |

13:30 |

Unemployment Rate |

May |

6.2% |

6.1% |

!!! |

|

US |

15:00 |

Wholesale Inventories (MoM) |

Apr |

0.2% |

-0.4% |

! |

|

US |

15:00 |

Wholesale Trade Sales (MoM) |

Apr |

-- |

-1.3% |

! |

|

EC |

15:15 |

ECB President Lagarde Speaks |

-- |

-- |

-- |

!!! |

|

US |

17:00 |

Fed Governor Cook Speaks |

-- |

-- |

-- |

! |

Source: Bloomberg