RBNZ cuts as US dollar stabilises at stronger levels

NZD & USD: RBNZ cuts with China optimism maintained

The New Zealand dollar is the clear under-performer in the G10 space this morning following the decision of the RBNZ to cut by 50bps to 4.75%. While not fully priced market pricing prior to the announcement indicated nearly a 90% probability of a 50bps cut. The decision to cut by 50bps continues a sharp shift in position from the RBNZ which in May was communicating to the markets that the first cut would come in the second half of 2025 and then in August when the RBNZ cut by 25bps it stated cuts would be done “calmly” and at a “measured pace”. There is nothing in today’s communications to question the prospect of the next cut also being 50bps when the RBNZ meets on 27th November. The OIS market now has that fully priced with 90bps priced over the next two meetings. Real GDP contracted by 0.2% Q/Q in Q2 and the RBNZ is projecting that annual CPI is set to fall to 2.3% in Q3 in data to be released on 16th October. New Zealand’s 2-year inflation expectation measure has now dropped back to 2.0%, the mid-point of the RBNZ’s target band. The RBNZ was one of the most aggressive central banks when policy was being tightened and there is certainly scope for the RBNZ to now be the most aggressive in easing given the speed in which inflation has returned back to target. We assume in our forecasts that NZD will lag behind most of the rest of G10 over the forecast period.

The fallout for NZD may have been lessened somewhat today by the announcement from the State Council Information Office in China that it will hold a briefing on fiscal policy on Saturday. According to the notice Finance Minister Lan Fo’an will introduce moves to strengthen fiscal policy. Chinese equity markets are lower today on disappointment but have rallied from earlier lows on the hope of something more meaningful being announced on Saturday. USD/Asia is lower helped by the renewed optimism. It’s crucial for the sustainability of the recent risk-on moves that something significant is announced on Saturday but we remain cautious, or even sceptical.

Tonight the minutes from the FOMC meeting in September when the Fed cut by 50bps will be released and markets will be looking for a sense of how strong the support for the larger cut was. Governor Bowman dissented but were others closer to joining her? Vice Chair Jefferson stated yesterday that risks to the two elements of the Fed’s dual mandate were now “roughly balanced” and we suspect the minutes tonight will indicate greater optimism on inflation but possibly to a lesser degree than implied by the decision to cut by 50bps. The CPI data tomorrow will still be key to whether the dollar breaks further stronger. The DXY index has still not broken above the high from Friday when the jobs data was released. That to us is indicative of reduced conviction in buying at these stronger levels and if the CPI data comes in as expected (m/m gains easing) we may see some modest retracement.

NEW ZEALAND 2-YEAR INFLATION EXPECTATIONS HAS FALLEN SHARPLY AND IS NOW BACK AT THE 2.0% MID-POINT OF THE TARGET BAND

Source: Macrobond & MUFG GMR

JPY: The Diet dissolved ahead of election on 27th October

USD/JPY has stabilised at levels below 150.00 with the highs in August following the rebound from the low on 5th August still to be breached. Momentum looks to be fading following the sharp rebound after the US jobs report fuelled by the big jump in front-end yields in the US. The wages data released in Japan yesterday were certainly strong enough to maintain the prospect of the BoJ continuing to gradually hike its short-term policy rate. The overall labour cash earnings annual rate slowed from 3.4% (revised from 3.6%) to 3.0% but this was stronger than the consensus. Overall wage growth slowed but to levels that remain consistent with the views of the BoJ – that the sustainability of the wage price spiral is set to result in the achievement of the inflation goal.

Still, it is clear that the new government is more uneasy over the risk of financial market stability undermining economic conditions to an extent that could see LDP support decline ahead of the election on 27th October. Yesterday, Economic Revitalisation Minister Ryosei Akazawa confirmed again the government’s support of the BoJ policy stance and the potential of future rate hikes “as long as they don’t cause a shock to the Japanese economy or markets”. The objective of the government is to try and ensure policy continuity and thus some signs of back-tracking on the initial comments from PM Ishiba that implied the government was more strongly opposed to the BoJ’s plans to hike rates. The new government could quickly become more concerned over excessive yen weakness. A break back above the 150-level could prompt renewed appetite for yen selling and given the link to the cost of living crisis, this is something the government will want to avoid as well. The LDP want to address voters anger with a stimulus package that the LDP says will ensure households are better protected from rising inflation. This package will be compiled after the election.

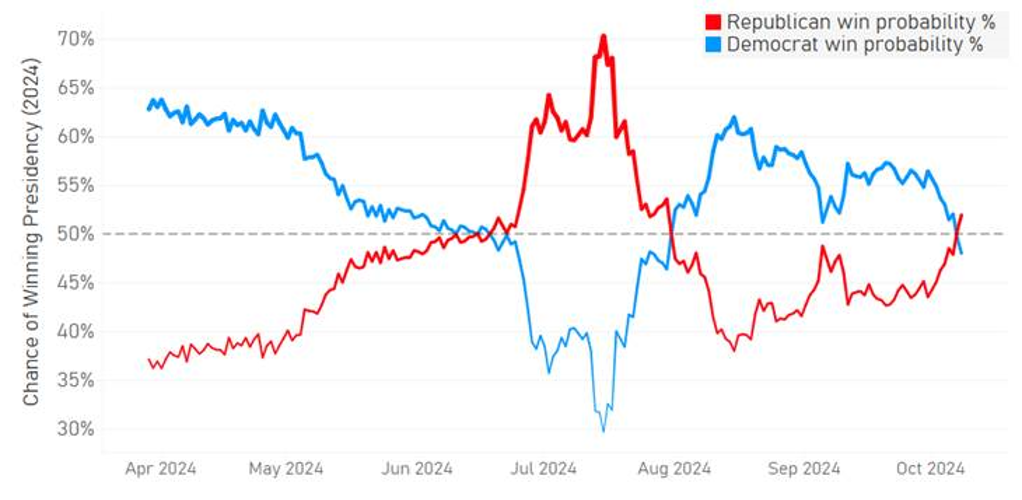

The Diet is being dissolved today and in a press conference later PM Ishiba will formally announce that the election will take place on 27th October. For the BoJ its next meeting will be just after the election on 31st October and updated forecasts at that meeting may further lower expectations of an imminent rate hike as Governor Ueda has already told us that upside inflation risks have receded – so the inflation projections may be somewhat lower. Still, for USD/JPY the Fed’s actions and the result of the US presidential elections will be far more important in determining USD/JPY direction. A Trump victory looks to be an increasing prospect based on betting odds which may well encourage further upside for USD/JPY if that momentum for Trump persists.

PROBABILITY OF TRUMP VICTORY SURPASSES HARRIS

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

09:30 |

ECB's Elderson Speaks |

-- |

-- |

-- |

!! |

|

US |

12:00 |

MBA Mortgage Applications (WoW) |

-- |

-- |

-1.3% |

! |

|

US |

13:00 |

FOMC Member Bostic Speaks |

-- |

-- |

-- |

!! |

|

US |

14:15 |

Fed Logan Speaks |

-- |

-- |

-- |

!! |

|

US |

15:00 |

Wholesale Inventories (MoM) |

Aug |

0.2% |

0.2% |

! |

|

US |

15:00 |

Wholesale Trade Sales (MoM) |

Aug |

-- |

1.1% |

! |

|

US |

15:30 |

Fed Goolsbee Speaks |

-- |

-- |

-- |

!! |

|

US |

15:30 |

FOMC Member Barkin Speaks |

-- |

-- |

-- |

!! |

|

US |

15:45 |

Fed Logan Speaks |

-- |

-- |

-- |

! |

|

US |

16:00 |

FOMC Member Williams Speaks |

-- |

-- |

-- |

!!! |

|

US |

16:00 |

Thomson Reuters IPSOS PCSI |

Oct |

-- |

55.02 |

! |

|

CA |

16:00 |

Thomson Reuters IPSOS PCSI (MoM) |

Oct |

-- |

49.48 |

! |

|

US |

17:00 |

Atlanta Fed GDPNow |

Q3 |

3.2% |

3.2% |

! |

|

US |

17:15 |

FOMC Member Barkin Speaks |

-- |

-- |

-- |

!! |

|

US |

17:30 |

Fed Governor Jefferson Speaks |

-- |

-- |

-- |

!!! |

|

US |

18:00 |

10-Year Note Auction |

-- |

-- |

3.648% |

!! |

|

US |

19:00 |

FOMC Meeting Minutes |

-- |

-- |

-- |

!!!! |

|

US |

22:00 |

Fed Collins Speaks |

-- |

-- |

-- |

!! |

|

US |

23:00 |

FOMC Member Daly Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg