Relief rebound for USD as expectations for larger Fed cut are pared back

USD: Weakening US labour market continues to pose downside risks for USD

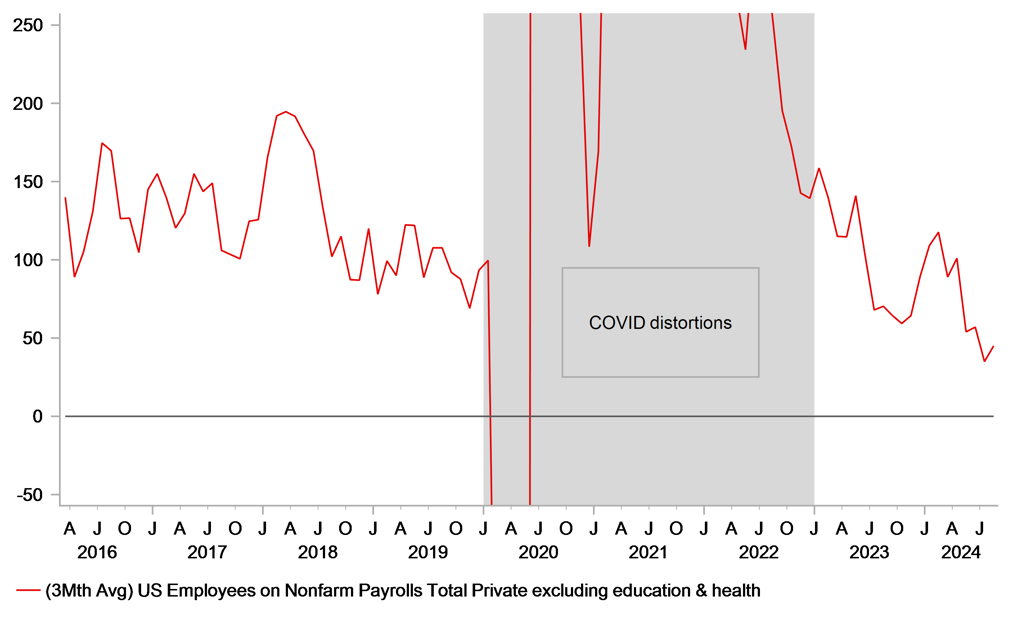

The US dollar has continued to trade at modestly stronger levels during the Asian trading session following the release of the latest nonfarm payrolls report on Friday. The dollar index is currently trading around +0.3% higher than pre-nonfarm payroll levels. The initial relief rally for the US dollar has been driven by the paring back of expectations for the Fed to deliver larger 50bps rate cut at the next policy meeting on 18th September. The US rate market is now pricing in around 32bps of cuts for the September FOMC meeting. At the same time, the US dollar is deriving support from more risk-off trading conditions. The sell-off in global equity markets has continued during the Asian trading session after last week’s correction lower. The release of the latest nonfarm payrolls report for August revealed further evidence that US labour demand continues to soften. While nonfarm employment picked up to 142k in August, it was offset by downward revisions to employment growth in previous months totalling -86k. There has been a clear slowdown in employment growth over the last three months to an average monthly increase of 116k compared to the average so far this year of 184k. With stronger labour supply growth, the recent pace of employment growth if sustained is unlikely to prevent a further increase in labour market slack. After increasing by 0.2 points in the previous month, the unemployment rate dropped back by 0.1 point to 4.2% in August but the upward trend remains in place.

The developments should keep pressure on the Fed to lower rates more quickly to less restrictive levels. The longer the Fed keeps rates at more restrictive levels, the higher the risk it triggers a sharper slowdown in the US labour market. In his keynote speech at Jackson Hole, Fed Chair Powell emphasized that “we will do everything we can to support a strong labour market”, and that “that the current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of an unwelcome further weakening in labour market conditions”. In light of these comments, one can’t completely rule out that the Fed could start their easing cycle by delivering a larger 50bps cut given current risks are tilted in favour of a further weakening in the labour market. Even though the US rate market has pared back expectations for a larger 50bps cut in September, market participants still believe it is a matter of time before a larger cut will be delivered. A 50bps cut is now almost fully priced in by the November FOMC meeting although the outcome for the US election will add additional uncertainty at that point in time.

Fed speakers since the nonfarm payrolls report was released did not give a strong indication that they favoured a larger 50bps cut as soon as this month although they are more confident to lower rates now. New York Fed Chair Williams stated that he feels that the Fed is “well positioned” and indicated that the Fed has no general principle on fast vs. gradual moves. Fed Governor Waller added that if appropriate he will advocate for “front-loading” cuts, and Chicago Fed President Goolsbee stated that he is concerned that tight policy is “raising recession risk”. Taking everything into consideration, we expect the relief rally for the US dollar to prove short-lived with the US labour market continuing to weaken, and a larger 50bps cut can’t be completely ruled out this month. We recommended a new short USD/JPY trade idea in our latest FX Weekly report (click here).

WEAK US PRIVATE EMPLOYMENT GROWTH

Source: Bloomberg, Macrobond & MUFG GMR

EUR: ECB to stick to gradual plans for rate cuts providing support for EUR

The EUR has continued to trade at stronger levels against the USD after breaking out above the 1.0500 to 1.1000 trading range in the second half of August. The pair closed above the 1.1000-level for the third consecutive week. It is the longest run of higher closes since late July/early August of last year. Recent price action is giving us more confidence that the adjustment higher for EUR/USD will prove more sustainable. In our latest monthly FX Outlook report (click here) we revised higher our forecasts for EUR/USD for the next couple of quarters to indicate that we now expect the pair to continue to trade within a higher range between 1.1000 and 1.1500 into year end.

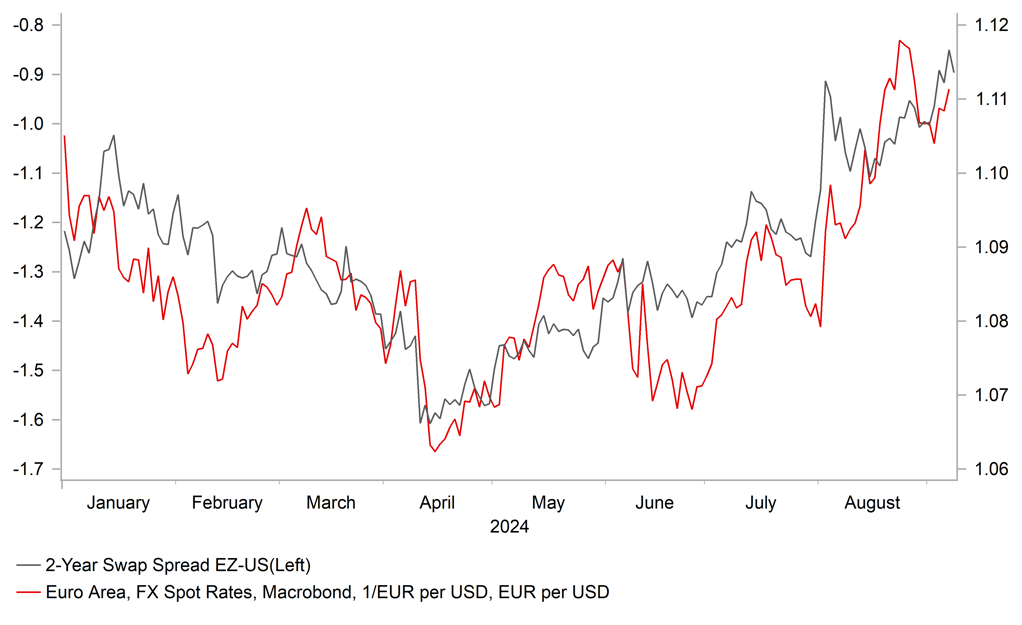

The main driver for the recent adjustment higher for EUR/USD has been building market expectations for more aggressive Fed easing as they plan to start cutting rates this month. Yields in the US have fallen by more than in the euro-zone over the past month. The two-year US government bond yield has fallen by 36bps compared to only 13bps for the German equivalent. US rate market participants have become more confident that the Fed will play catch up with the ECB by cutting rates at all three remaining FOMC meetings this year by a cumulative total of around 111bps. It reflects expectations as well that at least one larger 50bps cut will be delivered to reflect the risk that the Fed feels it has fallen behind the curve. In contrast, the euro-zone rate market still expects the ECB to remain more cautious when lowering rates. There are only around 63bps of ECB rate cuts priced in by the end of this year.

We expect the ECB to cut rate for the second time in the current easing cycle in the week ahead by 25bps lowering the policy rate to 3.50%. It follows the decision to leave rate on hold at the last meeting in July. The decision to cut rate again this week should be supported by the updated ECB staff forecasts that could be revised modestly lower both for inflation and growth in the euro-zone. The previous ECB staff forecasts from June for inflation were set at 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, while the GDP forecasts were set at 0.9% in 2024, 1.4% in 2025 and 1.6% in 2026. However, the forecast revisions are unlikely to be sufficient on their own to encourage the ECB to speed up the pace of rate cuts.

The ECB will have been encouraged by the release recently of their latest negotiated wage data for the euro-zone that revealed a sharper slowdown to 3.6% in Q2 from 4.7% in Q1. ECB Chief Economist Lane stated recently that they expect wage growth to ease significantly next year as well. On balance, we still expect the ECB to stick to the current quarterly pace for rate cuts. While we don’t expect President Lagarde to completely rule out back to back cuts at the next policy meeting in October, it remains more likely that the ECB will wait until December to deliver the third rate cut in the cycle when they will again have access to updated ECB staff forecasts. For the ECB to speed up the pace of rate cuts, it will require clearer evidence that inflation is falling back more quickly to their target and euro-zone economy/labour market is much weaker than expected. After returning to modest growth in the first half of this year, we expect the economic recovery to continue through the rest of this year supported by rising real disposable income as the negative energy price shock continues to ease. The disappointing performance of Germany’s economy does though remain one area of concern. Economic growth contracted again in Q2 for the third time out of last five quarters.

In these circumstances, we are not expecting this week’s ECB policy to have a significant impact on the performance of EUR/USD assuming that the ECB’s updated communication remains consistent with further gradual policy easing. President Lagarde would have to signal more strongly that back to back rate cuts could be delivered in October to trigger a bigger dovish repricing for the euro-zone rate market and trigger a deeper pullback for EUR/USD back below support at the 1.1000-level. Without a significant dovish policy surprise from the ECB, the performance EUR/USD is likely to remain driven more by expectations for Fed policy in the near-term.

SHORT-TERM YIELD SPREADS HAVE BEEN MOVING IN FAVOUR OF EUR

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

SZ |

09:00 |

Total Sight Deposits CHF |

Sep-06 |

-- |

456.7b |

! |

|

EC |

09:30 |

Sentix Investor Confidence |

Sep |

-1220.0% |

-1390.0% |

!! |

|

US |

16:00 |

NY Fed 1-Yr Inflation Expectations |

Aug |

-- |

3.0% |

!! |

|

US |

20:00 |

Consumer Credit |

Jul |

$12.000b |

$8.934b |

!! |

|

NZ |

23:45 |

Mfg Activity SA QoQ |

2Q |

-- |

0.7% |

! |

Source: Bloomberg