Fears over tightening credit conditions remain in focus ahead of US CPI report

USD: All eyes on US CPI report for fresh direction

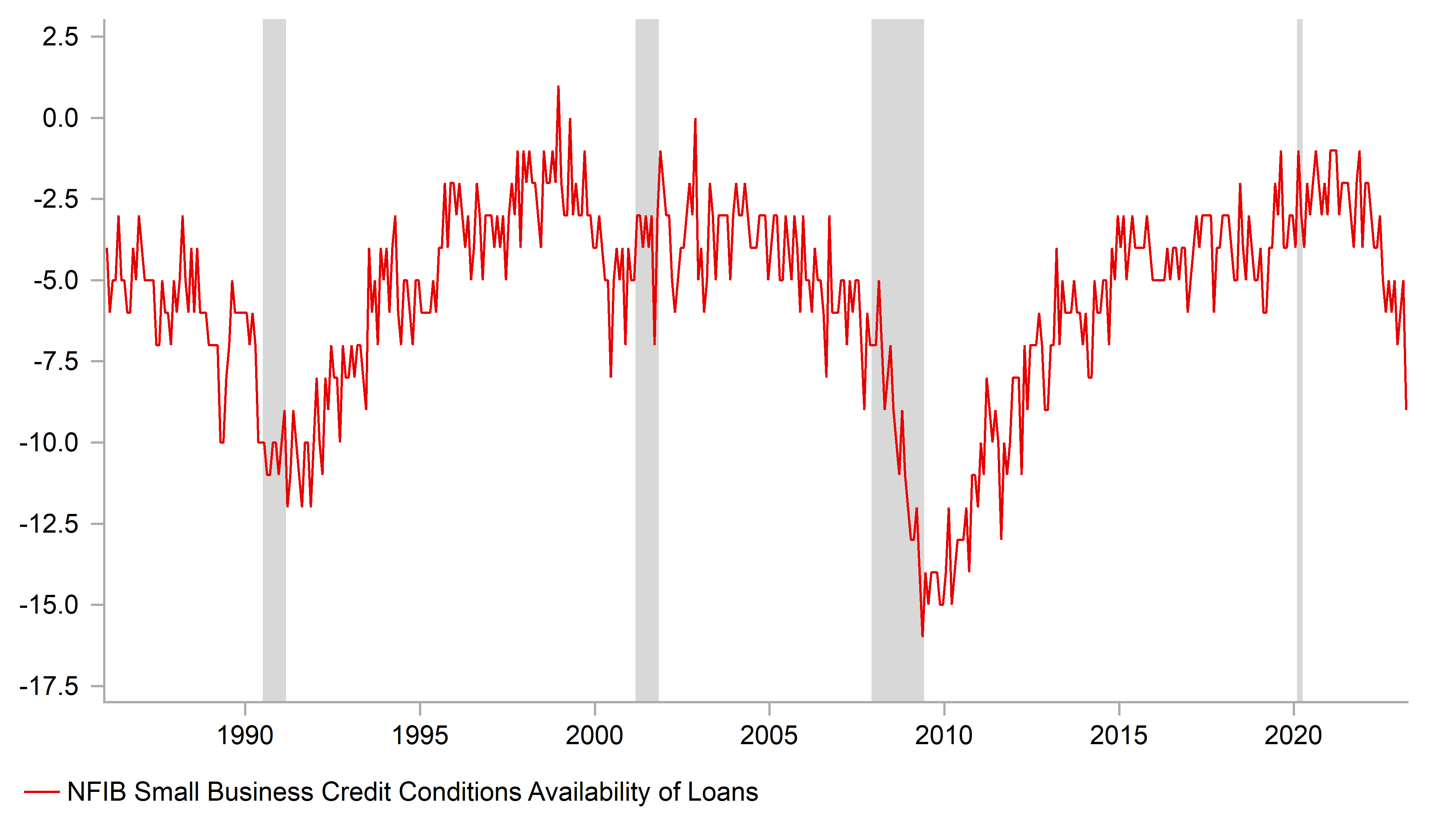

The major foreign exchange rates have remained relatively stable overnight ahead of the release later today of the latest US CPI report for March. It leaves the dollar index trading at just above the year to date lows. It has not derived much support so far from the scaling back of dovish Fed policy expectations since late last week. The US rate market has moved to almost fully price in at least one more 25bps hike by the end of this quarter but is still expecting the Fed to perform a u-turn later this year and deliver around 50bps of cuts by year end. Key to those expectations for the Fed to begin cutting rates later this year is the assumption that credit conditions will tighten significantly and trigger a sharper slowdown in US growth and inflation. The release yesterday of the NFIB business confidence survey for March will have encouraged those dovish expectations. It revealed that the availability of loans sub-component dropped sharply by -4.0 points to -9.0 in March which was the lowest reading since the end of 2012. It fits with expectations that small and medium sized-businesses are expected to be hit the hardest by the loss of confidence in US regional banks.

Furthermore, the hiring plans sub-index continued to fall and hit its lowest level since March 2020 during the worst initial stage of the COVID shock. After last week’s NFP report revealed that employment slowed to 236k in March, the NFIB sub-index is signalling that employment growth is set to fall below 200k in the coming months.

The additional uncertainty over the outlook for the US economy that has been created by the loss of confidence in US regional banks is leading to some divergence in views over the outlook for Fed policy amongst officials. New York Fed President Williams spoke yesterday and indicated that one more hike by the Fed followed by a pause was a good starting place. He still feels that the Fed has some work left to do to bring inflation down to target. Meanwhile Chicago Fed President Goolsbee who is a voter on the FOMC this year expressed more caution calling for “prudence and patience” in assessing the impact of tighter credit conditions. Overall the comments did not materially alter market expectations for one final 25bps hike. Market participants will now turn their attention to the release later today of the latest US CPI report for March. The report is expected to reveal that underlying inflation pressures remained uncomfortably strong at the start of this year. While a stronger print poses upside risks for the US dollar, ongoing fears over the negative fallout for the US economy from tighter credit conditions will continue to put a dampener on upside potential in the near-term.

NFIB SURVEY ADDS TO FEARS OVER TIGHTENING CREDIT CONDITIONS

Source: Bloomberg, Macrobond & MUFG GMR

EM FX: Latam FX continues to outperform at the start of this year

The recent rebound for EM currencies against the USD has lost some upward momentum at the start of this month following on from strong gains recorded during the second half of March. There has though been a wide divergence in performance amongst emerging market currencies. One constant has been the continued underperformance of the RUB which is well course to be the worst performing emerging market currency for the second consecutive month. The RUB has been trending weaker since December. The pace of RUB depreciation has even accelerated so far in April resulting USD/RUB jumping up from around the 78.00-level at the end of last month to closer to the 83.000-level. The pair is now trading back above pre-Ukraine conflict levels from in early 2020. The RUB has weakened following the introduction of the price cap on Russian oil from 5th December for crude oil and 5th February for petroleum products. The release yesterday of the latest current account report from Russia provided confirmation that the surplus narrowed sharply in Q1 providing less support for the RUB. After peaking at USD77.2 billion in Q2 of last year, Russia’s current account surplus has fallen back sharply to USD18.6 billion I Q1. The RUB has continued to weaken in recent weeks even as the price of oil has rebounded triggered in part by the surprise decision (click here) from OPEC+ members to cut production. The recent faster pace of RUB weakness could increase pressure to the CBR to bring forward plans to raise rates although the release in the week ahead of the of latest Russian CPI report is expected to reveal that inflation fell sharply in March driven by favourable base effects.

At the other end of the spectrum, the best performing EM currencies this month have been the COP (+2.5% vs. USD), the HUF (+1.9%), the BRL (+1.1%), the PLN (+1.0%) and the RON (+1.0%). The HUF, COP, and BRL are also amongst the best performing EM currencies so far this year, with the MXN (+7.3% vs. USD YTD) and CLP (+5.6%) making up the rest of the top 5 performers. Latam currencies have outperformed as the USD has weakened broadly and US yields have adjusted lower. The higher yields on offer in Latam remain attractive for carry trades. The initial jump in EM FX volatility and squeeze on carry trades in response to banking sector fears proved to be short-lived. The HUF has similarly been boosted by the NBH’s recent strong commitment to maintain higher policy rates. The ongoing outperformance of Latam currencies would be threatened if fears over a sharper global slowdown and/or US recession were to intensify. USD/BRL and USD/MXN have given back some of their gains over the past week after they moved closer to important support levels at 5.0000 and 18.000. USD/BRL did though briefly move below the 5.0000-level yesterday as fears over the government’s budget plans eased further that could open up a further move lower for the pair if support is broken. Please see our latest EM EMEA weekly for more details (click here).

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

US |

13:30 |

Core CPI (YoY) |

Mar |

5.6% |

5.5% |

!! |

|

US |

13:30 |

CPI (YoY) |

Mar |

5.2% |

6.0% |

!!! |

|

EC |

13:30 |

ECB's De Guindos Speaks |

-- |

-- |

-- |

!! |

|

UK |

14:00 |

BoE Gov Bailey Speaks |

-- |

-- |

-- |

!!! |

|

CA |

15:00 |

BoC Monetary Policy Report |

-- |

-- |

-- |

!!! |

|

CA |

15:00 |

BoC Interest Rate Decision |

-- |

4.50% |

4.50% |

!!! |

|

CA |

16:00 |

BOC Press Conference |

-- |

-- |

-- |

!!! |

|

UK |

20:15 |

BoE Gov Bailey Speaks |

-- |

-- |

-- |

!!! |

Source: Bloomberg