ECB cuts again with focus on size of Fed cut weighing on USD

USD: 50bp cut next week still on?

The ECB cut its key policy rate by 25bps as expected and we were not surprised by the communications from ECB President Lagarde who repeated the key elements of past guidance – that future decisions would be “meeting-by-meeting”, that the policy stance would remain restrictive for “as long as necessary” and that the battle against inflation was still not won. Services inflation was still too high. As outlined in an FX Focus piece yesterday (here), we saw this meeting as consistent with a probable skip at the October meeting followed by a cut at the next forecast-update meeting in December. EUR/USD advanced based on the fact that there was no indication of a faster pace of cuts with no clear signal of a cut in October.

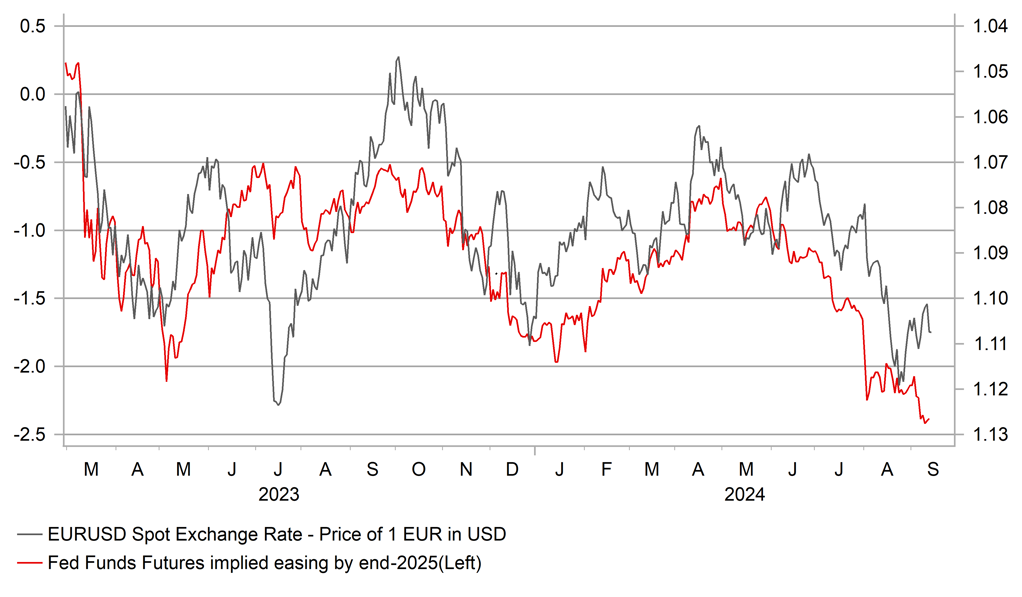

EUR/USD has been given a further lift by the increased speculation that the FOMC may indeed cut by 50bps next week. The MUFG house view, from our US rates team, remains a 50bp cut and we argued this week that even after the surprise 0.3% core CPI gain there was a justification for cutting by 50bps given the upside surprise was not broad-based (only rents and airfares fuelled the upside surprise). If the Fed truly want to be forward looking and have already indicated the shift in focus from upside inflation risks to downside employment risks there is every reason to commence with a 50bp cut. As stated here this week, four 75bp rate hikes and two 50bp rate hikes when policy was being tightened in 2022-23 certainly provide recent precedent for moving in larger sizes.

The renewed speculation of a bigger cut has been triggered by a Wall Street Journal article by Nick Timiraos (“The Fed’s rate cut dilemma: Start big or small?”) and is being interpreted by the markets as being an orchestrated move by the Fed given this journalist is known to have Fed links. The article also quotes Jon Faust who served as a senior advisory to Fed Chair Powell until earlier this year stating that the decision next week between 25/50bps is “a close call”. There is also an article in the FT today on the same topic of how much the Fed may cut next week.

The probability of a 50bp cut dropped to less than 10% following the higher than expected CPI print but has now jumped to a one-in-three chance which means for the FOMC to go by 50bps next week would be a surprise for the market, but not a big surprise and not something that would necessarily shock the markets. We don’t know if this WSJ article has been orchestrated or not but this leaves the decision next week finely balanced. We recommended a short USD/JPY in our FX Weekly last Friday (here) in part on the view that the Fed would surprise and cut by 50bps next week and we also raised our EUR/USD end-Q3 forecast from 1.0900 to 1.1200 in part on the basis of a larger cut in September. The labour market is weakening and inflation is close to target – there is no reason to delay.

EUR/USD (INVERTED) VS BPS OF EASING BY FED BY MID-2025

Source: Macrobond & Bloomberg

CAD: Negative sentiment building

The Canadian dollar has been broadly stable this week despite data last week increasing concerns over the outlook for the economy. The data flow last week was mixed but certainly didn’t allay the expectations of the economy performing poorly and worse than the BoC is forecasting. There was an increase in employment of 22.1k in August but because of labour supply, the unemployment rate increased from 6.4% to 6.6%. That will help dampen wage growth and ease inflation further after recent months of recorded declines in CPI that were greater than expected. The Ivey Purchasing Managers’ Index further increased expectations of a weakening economy with a sharp fall to 48.2, the lowest level since December 2020 when covid was impacting the economy.

CAD stability this week also comes after a speech by BoC Governor Macklem in London where he suggested increased BoC concerns over supply-side dynamics possibly weighing more on inflation than initially expected. Macklem mentioned “strong” immigration flows which if coupled with signs of increased layoffs “would be a concern”. The fact that younger workers and new entrants to the labour market were taking longer to find a job certainly increased the risk of labour market weakness that would alter the inflation risks. That scenario could open up the potential for faster rate cuts by the BoC, Macklem added, implying the potential for a 50bp cut.

Our assumption at this juncture was that the BoC would stick to 25bp cuts and that the prospect of 50bp cuts by the Fed would allow for the policy rate spread to narrow back from the current wider level of close to 100bps. That could prompt a further liquidation of short CAD positioning and allow for some moderate CAD appreciation into year-end. The positioning backdrop has already changed somewhat with Leveraged Funds having already pared back 50% of the short position over the last three weeks. That could imply renewed capacity for rebuilding CAD shorts if expectations of a 50bp cut increases further. At the moment there is about 50% probability of a 50bp cut in one of the two remaining meetings this year.

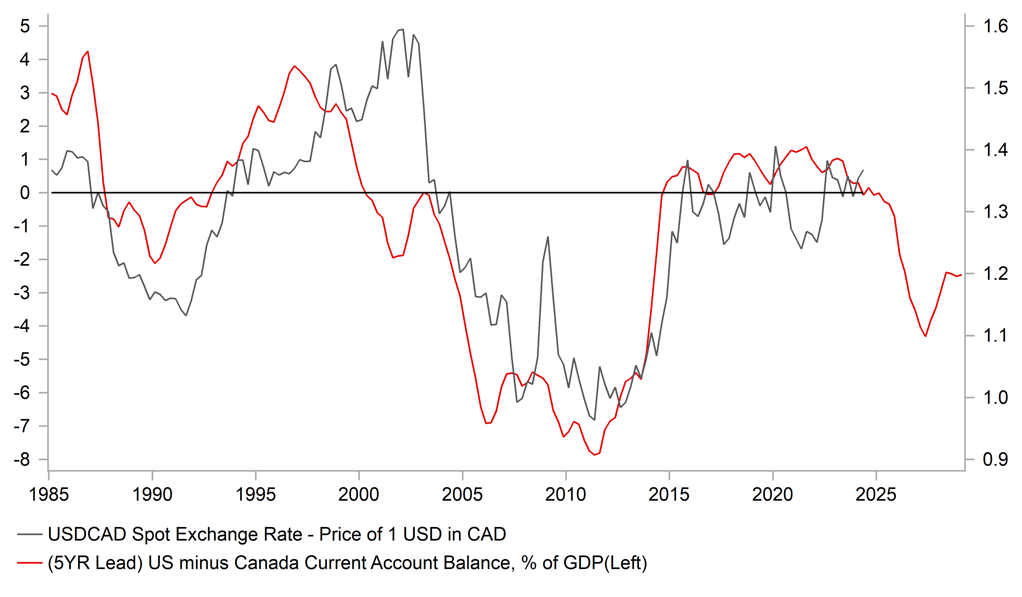

The crude oil market could also prove a downside risk, especially if at the same time expectations of a larger BoC rate cut increase. The oil CAD correlation is not particularly robust, our daily % change correlation between USD/CAD and crude oil is around -0.32% with the oil correlation with JPY and CHF currently stronger. Still, if crude oil falls further we would expect the CAD correlation to strengthen. If the BoC does end up cutting faster, it would more likely mean that the drop in USD/CAD we expect will not materialise rather than USD/CAD rising notably from here. We also assume here that crude oil prices do not fall notably from here. Canada’s external position also points to better underlying support for the Canadian dollar.

CANADA’S RELATIVE EXTERNAL POSITION VS US SHOULD HELP LIMIT CAD DOWNSIDE CYCLICAL RISKS

Source: Macrobond & Bloomberg

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

UK |

09:30 |

Inflation Expectations |

-- |

-- |

2.8% |

! |

|

EC |

10:00 |

Industrial Production (YoY) |

Jul |

-2.7% |

-3.9% |

! |

|

EC |

10:00 |

Industrial Production (MoM) |

Jul |

-0.6% |

-0.1% |

!! |

|

CH |

12:00 |

M2 Money Stock (YoY) |

Aug |

6.2% |

6.3% |

! |

|

CH |

12:00 |

New Loans |

Aug |

810.0B |

260.0B |

!! |

|

CH |

12:00 |

Outstanding Loan Growth (YoY) |

Aug |

8.6% |

8.7% |

! |

|

CH |

12:00 |

Chinese Total Social Financing |

Aug |

2,950.0B |

770.0B |

! |

|

US |

13:30 |

Export Price Index (MoM) |

Aug |

-0.1% |

0.7% |

! |

|

US |

13:30 |

Import Price Index (MoM) |

Aug |

-0.2% |

0.1% |

! |

|

CA |

13:30 |

Capacity Utilization Rate |

Q2 |

78.8% |

78.5% |

! |

|

CA |

13:30 |

Wholesale Sales (MoM) |

Jul |

-1.1% |

-0.6% |

!! |

|

US |

15:00 |

Michigan 1-Year Inflation Expectations |

Sep |

-- |

2.8% |

!! |

|

US |

15:00 |

Michigan 5-Year Inflation Expectations |

Sep |

-- |

3.0% |

!! |

|

US |

15:00 |

Michigan Consumer Expectations |

Sep |

71.0 |

72.1 |

!! |

|

US |

15:00 |

Michigan Consumer Sentiment |

Sep |

68.3 |

67.9 |

!! |

|

US |

15:00 |

Michigan Current Conditions |

Sep |

61.5 |

61.3 |

! |

Source: Bloomberg