US data leaves USD vulnerable to further selling

USD: Very front-end rate support will fade

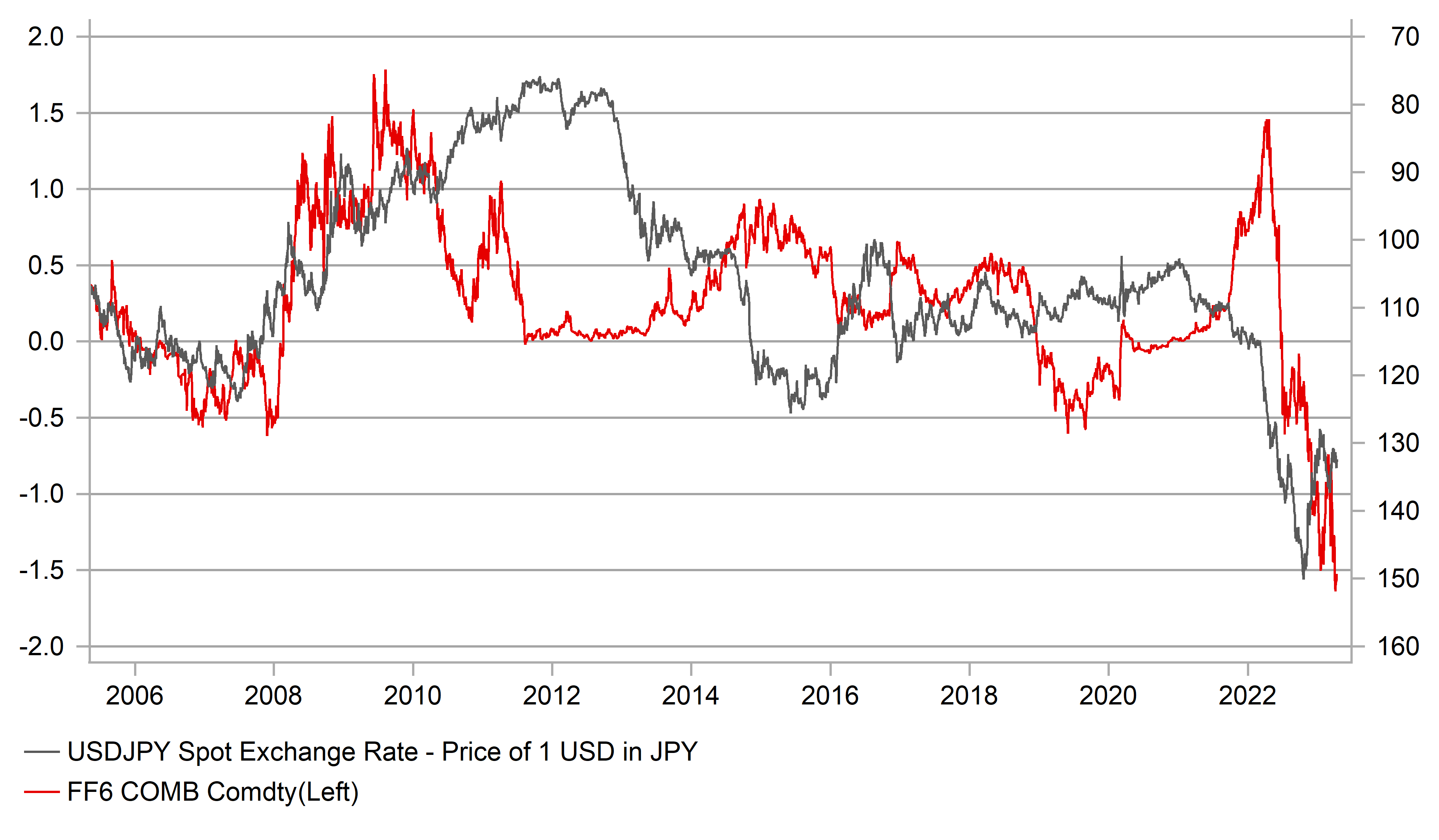

The chart below is the spread between 6mth forward fed funds and 18mth forward derived from the futures market and in the history of the available data on Bloomberg there has never been such a divergence in rate expectations over a 12mth period six months forward, even in the run in to the Global Financial Crisis. The correlation with USD/JPY has not particularly reliable. After all, if that spread narrows from here on the markets removing the scale of rate cut expectations in 18mths that would be a lot more supportive for USD/JPY than the scenario of that spread narrowing due to the rate cuts being brought forward more in 6mths relative to 18mths. The period immediately after the GFC is when this spread correlated well as the Fed cut aggressively.

It seems unlikely that this scale of spread inversion over a relatively short period of time will last long. Something will have to give. The FOMC not cutting on 3rd May would likely see the spread narrowing as would a very quick pivot following a May rate hike that fuelled more aggressive rate cut speculation over a shorter period. We certainly see those risks as a lot higher now than the market removing the scale of monetary easing priced into the market at the 18mth point of time. That would leave USD/JPY most vulnerable to a sharper move to the downside no matter what BoJ Governor Ueda decides to do with the current YCC framework.

The PPI data from the US yesterday was the latest data that adds to the risk of that 6mth-18mth fed funds spread starting to narrow. The scale of drop in the PPI readings were a lot larger than expected and provided further evidence that inflationary pressures are turning south dramatically. The Trade Services component in the PPI data which is a measure of company profit margins has been plunging as supply constraint problems ease and conditions normalise.

The 3mth annualised rate of change recorded in March was a huge -7.7% - a record low in the series, surpassing the previous low in 2012. Admittedly, the history of the data is relatively short but it is nonetheless indicative of deflationary conditions in the goods sector emerging later in the year. The below chart includes the PCE goods inflation on an annual basis.

As we stated yesterday, we believe a rate hike in May is not necessary as the evidence of declining inflation becomes more obvious. But the FOMC seems more likely to act again based on the minutes released on Wednesday which will delay the turn higher in that 6mth-18mth fed funds spread. US dollar momentum is set to remain negative. The Fed can only now be waiting for more obvious signs of labour market weakness before turning more unanimously dovish and when that happens USD/JPY is likely to take another tumble lower.

US TRADE SERVICES PPI (3MTH ANNUALISED) VS PCE GOODS INFLATION YY

Source: Macrobond & MUFG GMR

USD: Debt ceiling concerns could add to dollar woes

We are now well into the second quarter of the year and that brings with it increased concerns that by the end of this quarter we could be in a situation of the debt-ceiling issue still not being resolved. It was the month of June that US Treasury Secretary Yellen cited as the first month when we could arrive at the point when extraordinary funding for the government runs out. Most see it a little later than that but there has been little sign of progress on what has been cited as a key risk to watch this year.

This week price action in the T-bill market revealed the issue is now coming into focus as a key short-term risk. Rates on bills maturing prior to June saw yields plunge this

this month for bills maturing this month and in May. Indeed, the 1-month T-bill fell 30bps yesterday although the yield has rebounded some today. The 1-month yield is still down over 50bps in April.

Investors are shunning bills in the 3-6mth area of the curve given most estimate any debt-ceiling related default risk lies in that period of time. The yield on the 1-month T-bill fell to 3.71% yesterday while the 3-month yield increased to 4.96%. The 3-month bill yield is over 20bps higher in April. The 12-month T-bill yield is at 4.63%. Money market funds have been flush with cash of late with bank deposits finding their way into these funds and these entities are avoiding the 3-6-month area of the curve. The FOMC possibly hiking in May could explain some of the spread but to have 3-6-month yields so much higher than 1-month and 12-month is telling.

The topic looks set to garner more attention ahead with Bloomberg reporting “people familiar with the talks” stating that Kevin McCarthy, the House Speaker, will next week unveil a plan to suspend the debt ceiling for a year in return for government spending concessions. The plan includes holding a vote in late May in the House to suspend the debt ceiling. However, the Democrats’ stance is that any negotiations on the debt ceiling should not have strings attached so that plan doesn’t look like it will go far. Of course the extent of the demands in that plan will be important.

In current circumstances, increased risks now on the debt ceiling is likely to be a dollar negative influence – it’s US specific and if it drags on into the summer will become a considerable drag on sentiment. Something to watch more closely from here over the coming weeks

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

US |

09:00 |

IEA Monthly Report |

-- |

-- |

-- |

!! |

|

US |

13:30 |

Export Price Index (MoM) |

Mar |

-0.1% |

0.2% |

!! |

|

US |

13:30 |

Import Price Index (MoM) |

Mar |

-0.1% |

-0.1% |

!! |

|

US |

13:30 |

Core Retail Sales (MoM) |

Mar |

-0.3% |

-0.1% |

!! |

|

US |

13:30 |

Retail Control (MoM) |

Mar |

-0.3% |

0.5% |

!!! |

|

US |

13:30 |

Retail Sales (YoY) |

Mar |

5.90% |

5.39% |

!! |

|

US |

13:30 |

Retail Sales (MoM) |

Mar |

-0.4% |

-0.4% |

!!! |

|

US |

13:30 |

Retail Sales Ex Gas/Autos (MoM) |

Mar |

-- |

2.8% |

!!! |

|

CA |

13:30 |

Manufacturing Sales (MoM) |

Feb |

-2.7% |

4.1% |

! |

|

US |

13:45 |

Fed Waller Speaks |

-- |

-- |

-- |

!! |

|

US |

14:15 |

Capacity Utilization Rate |

Mar |

79.0% |

79.1% |

! |

|

US |

14:15 |

Industrial Production (YoY) |

Mar |

-- |

0.32% |

!! |

|

US |

14:15 |

Industrial Production (MoM) |

Mar |

0.2% |

0.3% |

!! |

|

US |

14:15 |

Manufacturing Production (MoM) |

Mar |

-0.1% |

0.1% |

!! |

|

US |

15:00 |

Business Inventories (MoM) |

Feb |

0.3% |

-0.1% |

! |

|

US |

15:00 |

Michigan 5-Year Inflation Expectations |

Apr |

2.80% |

2.90% |

!!! |

|

US |

15:00 |

Michigan Consumer Sentiment |

Apr |

62.0 |

62.0 |

!! |

|

US |

15:00 |

Michigan 1-Year Inflation Expectations |

Apr |

3.5% |

3.6% |

!!! |

|

US |

15:00 |

Retail Inventories Ex Auto |

Feb |

0.4% |

0.1% |

!! |

|

UK |

16:30 |

MPC Member Tenreyro Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg