US-Iran deal encourages weaker USD

USD: A deal is finally reached to end conflict and reopen the Strait of Hormuz

The US dollar has continued to weaken at the start of this week driven by the announcement over the weekend that the US and Iran have finally reached an interim agreement to end the conflict and reopen the Strait of Hormuz. Officials from both countries will meet in Switzerland on 19th June to formally sign the agreement. The The exact details of the agreement have not yet been released but it will reportedly set another 60-day window for negotiations to continue over the future of Iran’s nuclear programme. President Trump has warned that the US could restart military strikes if an agreement on Iran’s nuclear programme is not reached within 60 days. Market participants will now be watching closely to see how quickly it takes for vessels to begin flowing back through the Strait of Hormuz. The price of oil has continued to drop back towards USD80/barrel overnight reflecting building investor optimism that energy supplies will soon begin to normalize. However, we doubt it will return to pre-conflict levels below USD70/barrel given it will take time for supplies to come back on stream, inventories have been run down and a larger geopolitical risk premium will still be required to reflect the ongoing risk of the deal breaking down.

The deal should help to reduce the risk of a more disruptive outcome for the global economy and financial markets. The biggest beneficiary so far among G10 currencies has been the Swedish krona which had been by far the worst performing since the conflict started in late February. A deal could also trigger a rebound for Asian currencies which have been hit hard by the conflict such as the Indonesian rupiah, South Korean won, Thai baht and Indian rupee. The Indonesian rupiah has already strengthened sharply by almost 1% against the US dollar at the start of this week. For the US dollar more broadly, the deal should encourage a further reversal of gains recorded during the conflict although market participants will be wary of building short positions ahead of the FOMC meeting on Wednesday given the risk of a hawkish policy update. FOMC participants are expected to indicate less support for lowering rates further including dropping the Fed’s easing bias. The updated DOT plot could also reveal more FOMC participants favouring rate hikes in response to upside inflation risks. However, we still expect new Fed Chair Kevin Warsh to signal that he is willing to look through the energy price shock by leaving rates on hold. A development which appears more likely now that a deal has been reached to end the conflict and reopen the Strait of Hormuz. The US rate market has already moved to scale back Fed rate hike expectations, but there is room for US yields and the US dollar to fall further if Kevin Warsh does not provide a hawkish policy surprise this week. The main risk to our view is that he indicates that the Fed is actively considering raising rates. Please see our latest FX Weekly report for more details (click here).

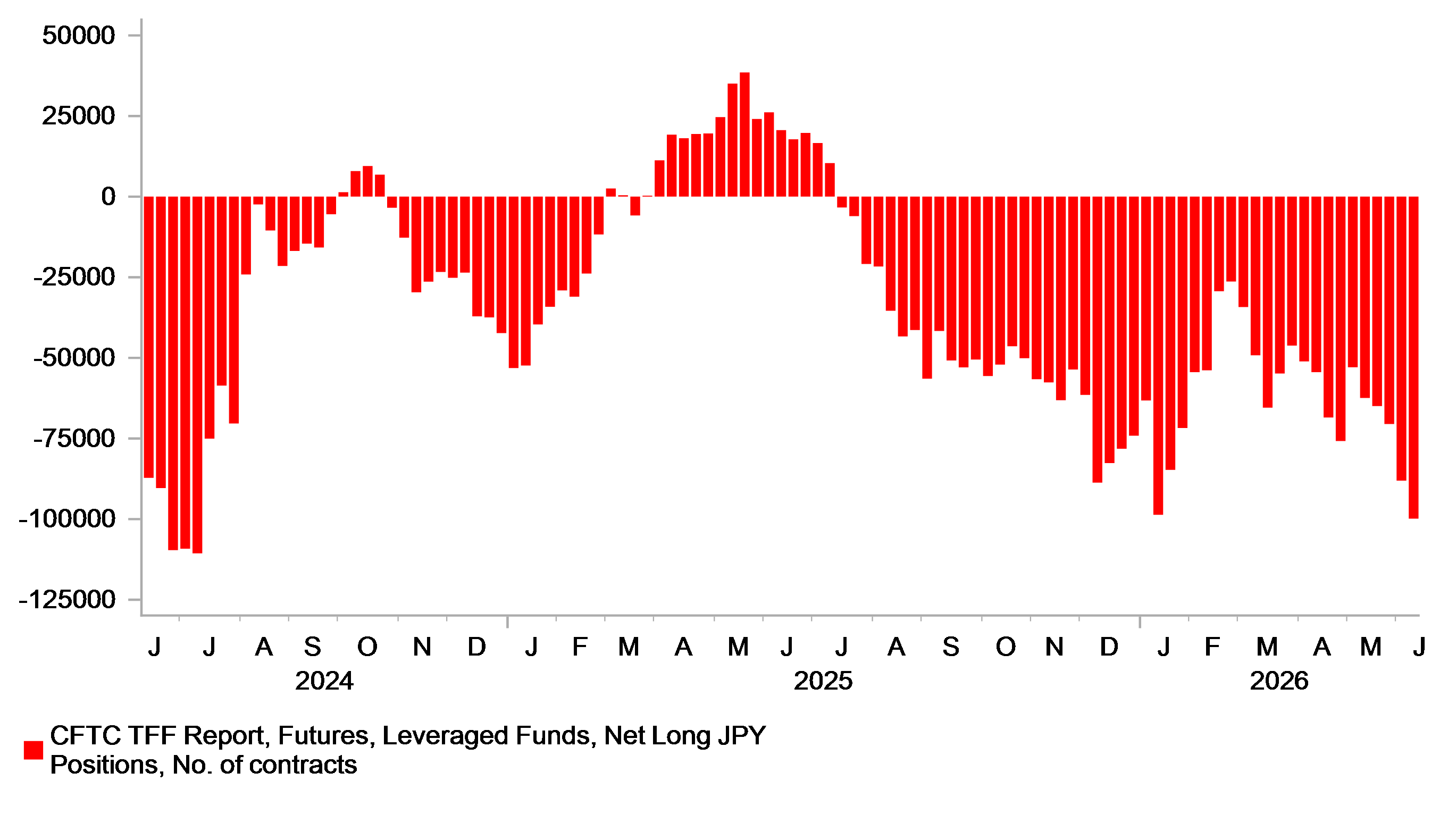

YEN-FUNDED CARRY TRADES HIT MULTI-YEAR HIGHS

Source: Bloomberg, Macrobond & MUFG Research

JPY: Short yen positions continue to increase ahead of BoJ meeting

The yen has failed to benefit so far from the ongoing drop in energy prices with USD/JPY continuing to trade above 160.00 ahead of this week’s BoJ policy meeting. Prior to the Middle East conflict, USD/JPY was trading lower at closer to the 156.00-level. The US-Iran deal through lower energy prices could help to ease yen selling. The latest IMM report revealed that leveraged funds have significantly increased short yen positions since the conflict started. Short yen position increased for the fifth consecutive week to 9th June and have increased by almost four times since late February reaching. It is the largest short yen position since the start of July 2024 which was then followed by the heavy liquidation of yen-funded carry trades in the summer of 2024 after the BoJ hiked rates in July 2024 and the Fed cut rates in September.

The BoJ is expected to raise rates again this week but another Fed rate cut appears unlikely until the end of this year at the earliest. Japanese media reports last week set the stage for the BoJ to hike rates by 25bps this week, and indicated that the BoJ is considering pausing QE tapering from FY2027. A 25bps hike is already fully priced in so is unlikely to trigger a reversal of yen weakness on its own thereby encouraging a further build-up of yen shorts recently. The updated rate guidance is likely to rock the boat either by sticking to a path for further gradual tightening. We expect another hike to be deliver by later this year. One potential source of market volatility will be press conference given that Deputy Governor Uchida will be stepping in for Governor Ueda who is ill. If the yen remains weak, it will keep pressure on Japan to intervene again to provide support. Intervention could prove more effective if energy prices continue to fall and Fed rate hike expectations are pared back.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 08:15 | ECB President Lagarde Speaks | - | - | - | !! |

EU | 10:00 | Trade Balance | (Apr) | 7.8B | 7.8B | !! |

US | 14:15 | Industrial Production (MoM) | (May) | 0.3% | 0.7% | !! |

Source: Bloomberg & Investing.com