USD starts week on firmer footing amidst Turkey election fallout

USD: UoM survey creates some unease over upside inflation risks

It has been a quiet start to the week for the major foreign exchange rates with the dollar index attempting to break to the upside from the narrow trading range it has been in since late March between 100.79 and 103.36. US dollar gains have been most evident overnight against the yen which has helped to lift USD/JPY back above the 136.00level. The next important resistance level for the pair is provided by the 200-day moving average that comes in at just above the 137.00-level. It has been tested on two occasions already this year in early March and early May, and has held so far. The US dollar is benefitting especially against the yen from the adjustment higher in US yields at the end of last week. The main trigger was release on Friday of the latest University of Michigan consumer confidence survey that revealed a sharp jump in long-term inflation expectations. It revealed that the 5-10 year measure of inflation expectations increased by 0.2ppt to 3.2% which was the highest level since March 2011. While one should never put too much weight an individual survey result, it is an uncomfortable reading for the Fed in their ongoing efforts to dampen upside inflation risks.

Furthermore, it will create some unease amongst participants who have become increasingly confident recently that the Fed’s rate hike cycle has come to an end. There is still only 3bps of additional hikes priced in for the current tightening cycle, and then followed up by -68bps of cuts by the end of this year. The rise in inflation expectations did though contribute to weakness in consumer confidence. The UoM expectations component of consumer confidence fell sharply to low levels that were recorded during past recessions during the Global Financial Crisis and in the early 1990’s. It continues to highlight the risk of a sharper slowdown for the US economy which alongside easing inflation and an already restrictive policy rate continues to favour the Fed pausing their hiking cycle soon. At the start of the early 1990’s recession and the Global Financial Crisis, the UoM long-term inflation expectations continued to rise before falling back as the downturn took hold.

In our latest FX Weekly (click here), we also highlighted other fundamental drivers that could be offering the US dollar more support in the near-term. Recent developments are dampening optimism over the outlook for growth outside of the US that is helping to provide more support for the US dollar. The USD sell-off since late last year has been driven in part by the improving cyclical outlook for growth in China and Europe.

While China’s economy is rebounding at the start of this year and European economies have avoided recession, doubts have started to creep back in recently over the strength of growth. Commodity prices sensitive to China demand (copper & iron ore) have corrected lower over the past month, and in the euro-zone the run of positive economic surprises since September of last year has come to an end. The release tomorrow of the latest monthly activity (industrial production, property investment & retail sales) data from China will be watched closely to further assess the strength of the economic recovery at the start of this year.

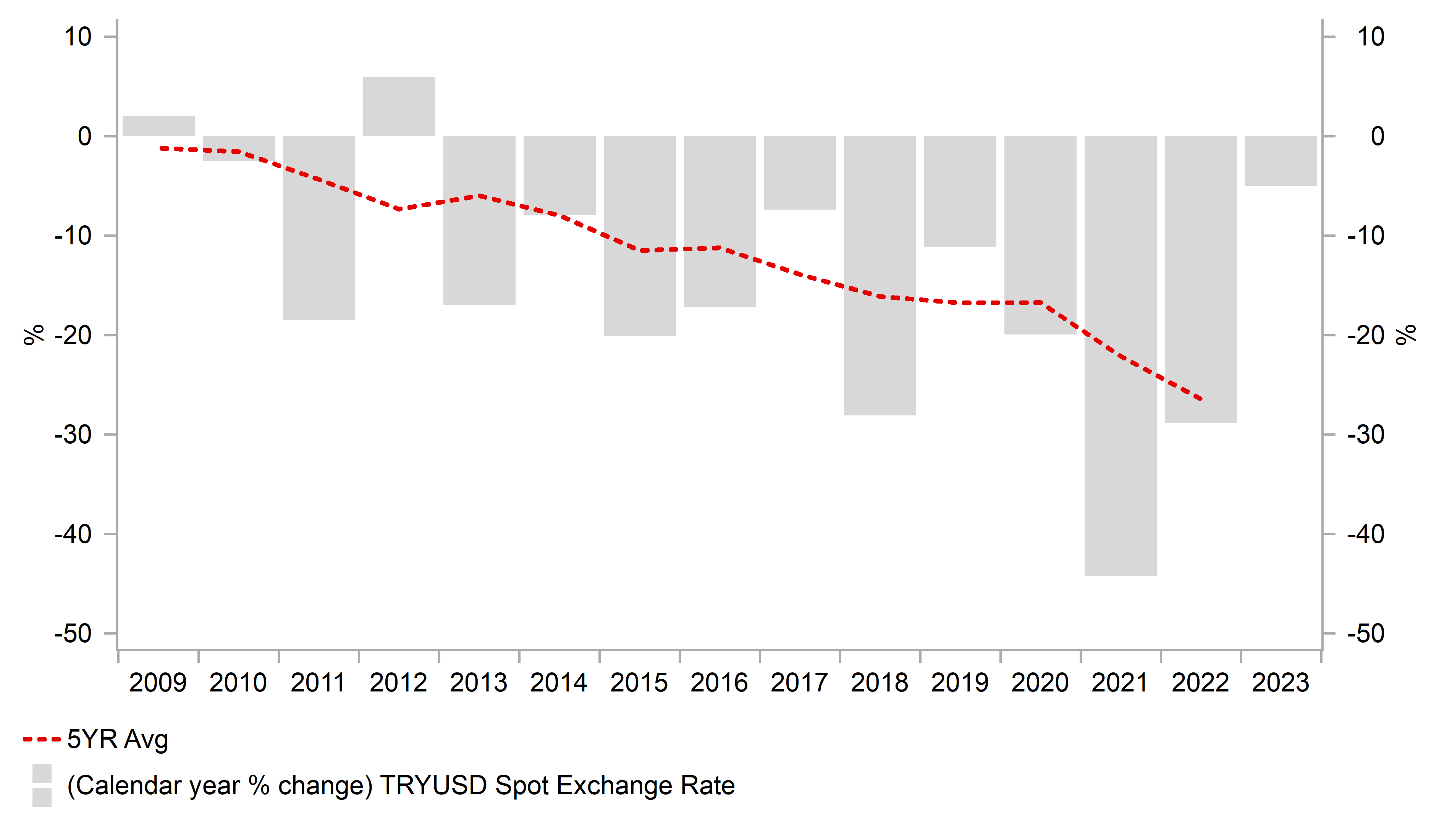

PRE-ELECTION WEAKENING TREND FOR TRY

Source: Bloomberg, Macrobond & MUFG GMR

TRY: Turkey elections results favour status quo outcome

In the run up to the elections in Turkey, the opinion polls had been signalling that it would be a close contest and that President Erdogan faced his toughest test to remain in power. The preliminary results released so far have revealed that President Erdogan is on course for a narrow victory in the Presidential election having won 49.3% of the vote compared to 45% for opposition leader Kilicdaroglu. With neither candidate currently on course to win 50% of the vote, it looks like a second Presidential election will need to be held on 28th May when the top two candidates face off against each other. It does though leave President Erdogan as the clear favourite to be re-elected. A further positive for President Erdogan is that his AKP party and their political alliance are well on course to maintain their majority parliament. It has been reported that President Erdogan’s governing coalition have secured 49.4% of the overall vote. It was though the worst parliamentary election result for the AKP party since it came to power in 2002.

The election results favour a continuation of status quo in Turkey, and is unlikely to trigger the return of foreign investors back to Turkey. We would expect policymakers in Turkey to maintain a relatively stable lira in the near-term ahead of the likely second round election. After the elections are over and the dust has settled, a continuation of unconventional policy settings, an elevated current account deficit, elevated inflation and dwindling FX reserves all point towards a weaker lira. As we have seen in recent years, the pace of lira depreciation has been picking up. Over the last five calendar years, the lira has depreciated against the US dollar on average by -26%. So far this year the pace has slowed down ahead of the elections with the lira falling more modestly by only -5% year to date. It leaves room for catch up weakness ahead. We see no reason to believe that the accelerating weakening trend in recent years will change if unconventional policies remain in place.

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

10:00 |

Industrial Production (MoM) |

Mar |

-2.5% |

1.5% |

!! |

|

EC |

11:00 |

Eurogroup Meetings |

-- |

-- |

-- |

!! |

|

GE |

13:10 |

German Buba President Nagel Speaks |

-- |

-- |

-- |

!! |

|

CA |

13:15 |

Housing Starts |

Apr |

224.6K |

213.9K |

!! |

|

US |

13:30 |

NY Empire State Manufacturing Index |

May |

-3.70 |

10.80 |

!! |

|

US |

13:45 |

FOMC Member Bostic Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg