GBP takes a hit as inflation continues to slow

CAD & NZD: Softer inflation readings add to headwinds

The biggest mover overnight amongst G10 currencies has been the New Zealand dollar following the release of the latest CPI report from New Zealand. It has resulted in NZD/USD falling back closer towards support at the 0.6000-level and lifted AUD/NZD further above the 1.1000-level. The report revealed that inflation in New Zealand slowed more than expected in Q3 to an annual rate of 2.2% down from 3.3% in Q2. It brings inflation back inside the RBNZ’s 1-3% target band and is the lowest reading since Q1 2021. The RBNZ had been expecting inflation to slow to around 2.3% in Q3 so it was broadly in line with their outlook. The breakdown of the inflation data revealed that domestically-driven components were responsible for the downside surprise in Q3. Non-tradable inflation slowed to an annual rate of 4.9% in Q3 down from 5.4% in Q2 and below the RBNZ’s forecast of 5.1%. At the same time the annual rate of tradable inflation fell into negative territory coming in at -1.6% in Q3 and it was the fourth consecutive quarter that prices in the tradable sector had fallen compared to the previous quarter. In particular, further evidence of slowing domestic inflation pressures will encourage the RBNZ to keep cutting rates at a faster pace after delivering a larger 50bps rate cut at last week’s policy meeting. The New Zealand rate market is already fully pricing in another 50bps rate cut at the final policy meeting of this year in November, and is starting to even price in higher risk of a larger 75bps rate cut. It follows comments as well this week from RBNZ Deputy Governor Hawkesby who stated that the policy rate is “headed more toward neutral”. He added that the pace of decline “is really around how things evolve from here” in terms of what information and data come up. With the policy rate still elevated at 4.75%, it remains well above estimates of the neutral policy rate which is likely closer to 3.00% and leaves plenty of room to keep cutting rates. A more aggressive rate cutting cycle form the RBNZ will remain a headwind for kiwi performance heading into next year.

Inflation also surprised to the downside in Canada yesterday although the negative impact on the Canadian dollar was more limited. USD/CAD initially rose up to an intra-day high yesterday at 1.3839 just after the release of the latest Canadian CPI report for September but has since more than fully reversed those losses and fallen to an intra-day low overnight of 1.3770. The Canadian CPI report revealed that headline inflation fell below the BoC’s target of close to 2% when it slowed to just 1.6% in September. It was the lowest reading since February 2021. The breakdown revealed that core inflation pressures continued to ease as well. The three-month annualized rate of change in the average of the trimmed and median core inflation measures slowed to 2.1% in September down from 2.3% in August. After stripping out mortgage interest rate costs, inflation has been running at an annual rate of just 1.1%. Similar to the RBNZ, the slowdown in inflation pressures provides a green light for the BoC to speed up the pace of rate cuts. The BoC has already discussed delivering larger 50bps rate cuts, and the Canadian rate market has now moved to more fully price in 50bps rate cuts at the next two BoC policy meetings in October and December. A development that poses downside risks for the Canadian dollar heading into year end. With the price of oil dropping sharply yesterday as well, the resilient performance of the Canadian dollar is impressive perhaps suggesting that it has already weakened a lot this month to better reflect the weakening fundamentals. Over the last couple of years USD/CAD has struggled to sustain levels above 1.3800.

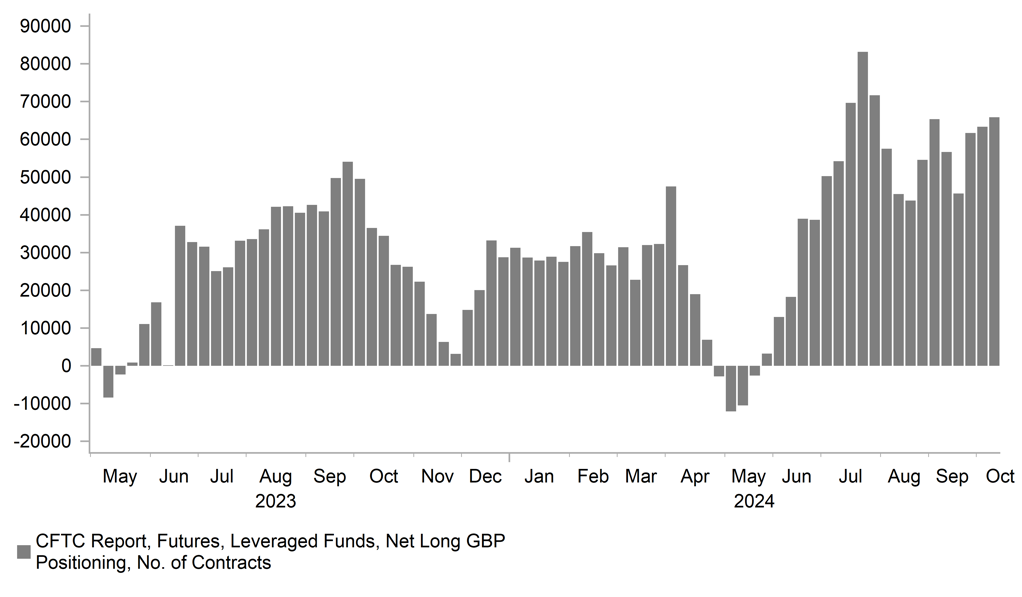

FASTER BOE RATE CUTS WOULD CHALLENGE LONG GBP POSITIONS

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Lower inflation & Budget to create more leeway for BoE cuts

The pound has been the biggest mover at the start of today’s European trading session with cable dropping sharply back below the 1.3000-level and EUR/GBP rising back up towards the 0.8400-level. The main driver has been another softer inflation report released this morning in the UK. The latest UK CPI report revealed that headline inflation fell back below the BoE’s 2.0% target to 1.7% in September from 2.2% in August. It is the first time that inflation has been below the BoE’s target since April 2021. The report provided further evidence that core and services measures of inflation continued to slow. The uptick for core and services inflation in August was more than fully reversed in September with the core inflation falling by 0.2ppt to 3.2% and services inflation by 0.3ppt to 4.9%.

Further evidence of slowing inflation will open up more room for the BoE to keep easing monetary policy. BoE Governor Bailey recently indicated that he would be willing to back more active rate cuts if there was further positive progress towards meeting their inflation target. Today’s softer inflation report and further evidence of slowing wage growth in yesterday’s labour market report support our forecast for the BoE to speed up the pace of rate cuts by the end of this year. We expect the BoE to deliver a 25bps rate cut in November and to signal that they are open to cutting rates again as soon as at the following meeting in December when we have pencilled in a back-to-back 25bps cut. A faster pace of BoE rate cuts would help to reverse pound gains recorded so far this year by undermining its carry appeal.

At the same time, it has been reported that the UK government is considering a larger package of fiscal consolidation measures in the upcoming Budget which could total up to GBP40 billion compared to previous claims that they wanted to fill a GBP22 billion black hole. Measures to raise additional tax revenues and cut public spending are reportedly intended to give the Chancellor more of a buffer against her target of ensuring the current budget is balanced, i.e. day-to-day spending is covered tax revenues. While additional fiscal consolidation measures will be welcomed by the gilt market and help to ease upward pressure on yields especially at the long end of the curve, they will act as more of a dampener on the growth outlook in the UK. At the margin, it could give the BoE more leeway to lower rates as well.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

IT |

09:00 |

Italian HICP (YoY) |

Sep |

0.8% |

1.2% |

! |

|

CA |

13:15 |

Housing Starts |

Sep |

235.0K |

217.4K |

!! |

|

US |

13:30 |

Import Price Index (YoY) |

Sep |

-- |

0.8% |

! |

|

CA |

13:30 |

Manufacturing Sales (MoM) |

Aug |

-1.5% |

1.4% |

! |

|

US |

19:00 |

Federal Budget Balance |

Sep |

61.0B |

-380.0B |

!! |

|

EC |

19:40 |

ECB President Lagarde Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg