The JPY continues to underperform ahead of BoJ policy meeting

JPY: Muted market reaction to assassination attempt on PM Kishida

The US dollar has staged a modest rebound since the end of last week after recording a year to date low on Friday of 100.79. However, the downward trend for the US dollar remains firmly in place this month. Only the New Zealand dollar and the yen have failed to strengthen further against the US dollar so far this month. USD/JPY continued to rebound overnight rising back above the 134.00-level as it moves further above the low from last month of 129.64. There has though been a relatively limited reaction from the yen and Japanese financial markets to the shocking news over the weekend that Japanese Prime Minister Kishida was subject to an assassination attempt when he was delivering a speech in the city of Wakayama in support of a fellow LDP politician who was running for the by-election. Five by-elections are scheduled to take place on 23rd April. As Bloomberg highlighted today the by-elections will provide another indication of whether the timing is right for Prime Minister Kishida to call an early election to strengthen his grip on power. It follows strong results in local elections earlier this month that have added to speculation that Prime Minister Kishida could call an early election after Japan hosts the latest G7 Summit in Hiroshima between 19th May and 21st May. The G7 foreign ministers are meeting in Japan at the start of this week that will set the agenda for next month’s G7 summit.

It has been speculated that if Prime Minister Kishida chooses to call an early election and is successful in strengthening his grip on power, it could provide the green light for the BoJ to make a bigger shift away from the looser policies more associated with Abenomics and thereby provide a fresh catalyst for the yen to strengthen further this year. The yen has recently lost upward momentum following the speech last week from new Governor Ueda who dampened speculation over a more imminent shift in BoJ policy as soon as at his first meeting as governor that takes place on 28th April. He stated clearly last week that he thought current policy settings including YCC were appropriate. It would now be a big surprise for the BoJ to adjust YCC policy settings later this month. The paring back of expectations for a further shift in in BoJ policy have contributed towards the yen underperforming this month. But with the US yields having peaked and the risk of a sharper US slowdown increasing, we see only limited room for USD/JPY to rebound further in the near-term and still expect it to break back below the 130.00-level this year.

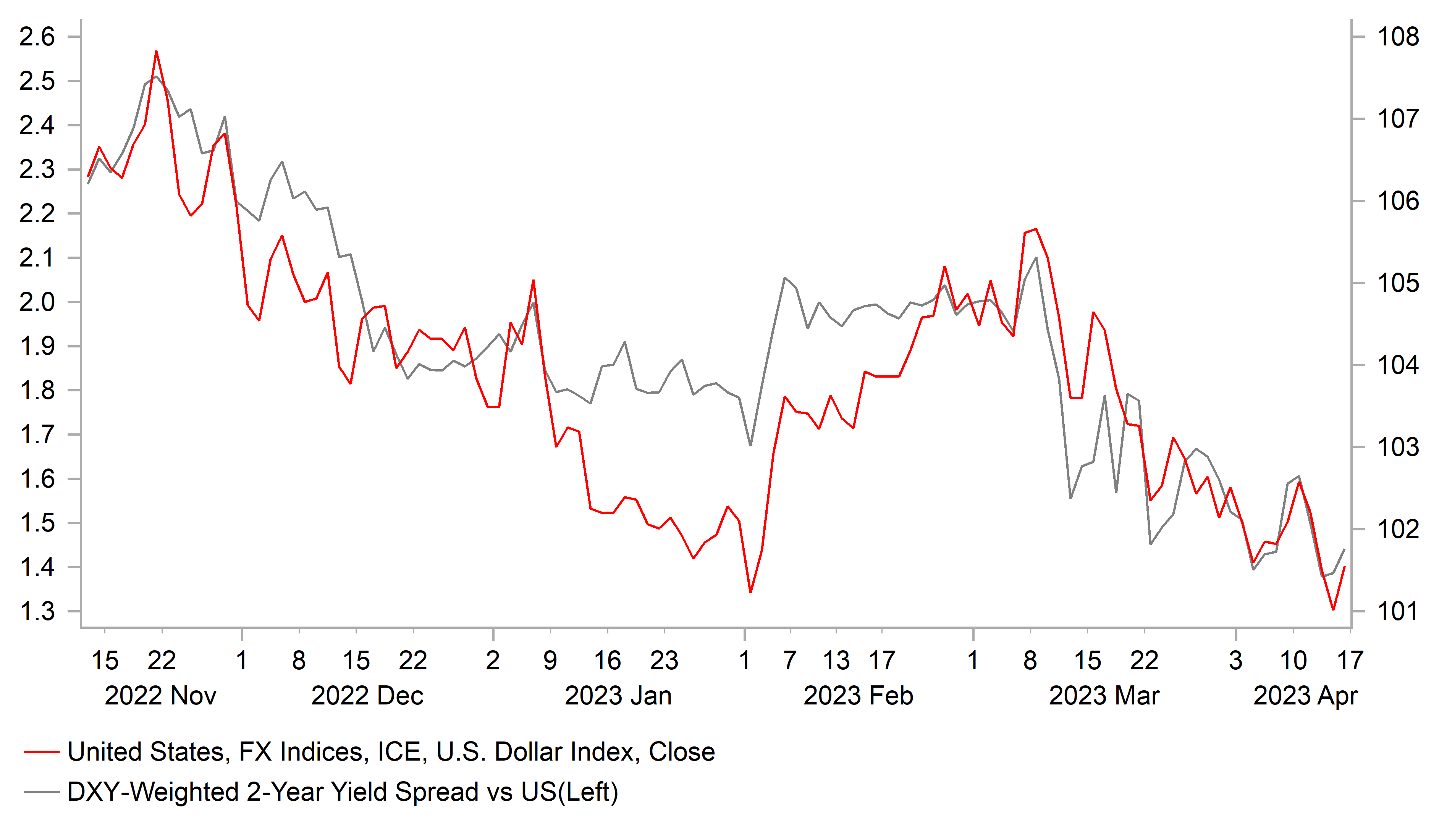

YIELD SPREADS REMAIN IMPORTANT DRIVER OF USD WEAKNESS

Source: Bloomberg, Macrobond & MUFG GMR

USD: Fears over impact of tighter credit conditions continue to weigh heavily

With the dollar index falling to a fresh year to date low, it brought the USD’s decline since the intra-day high on 8th March closer to 5% against other major currencies. The collapse of Silicon Valley Bank and the subsequent loss of confidence in other US regional banks has proven to be an important bearish turning point for the USD. It is poised to extend its decline further with important support levels in the process of being challenged. Over the past week there have been a number of bearish technical developments including: i) EUR/USD breaking above the year to date high from 2nd February at 1.1033 and reaching its highest level in just over a year, ii) USD/CHF falling even more sharply to its lowest level the start of 2021 after breaking below the 0.9000-level, and iii) USD/CAD falling below support from the 200-day moving average at around 1.3400 for the first time since the summer of last year.

The USD’s bearish momentum has been reinforced recently by economic data releases that have supported expectations for a sharper slowdown in both US growth and inflation. Last week’s NFIB small business survey signalled that credit conditions are tightening with the sub-component for the availability of loans falling sharply to its lowest level since 2012. The release of the minutes from the last FOMC meeting on 22nd March revealed the Fed staff were already anticipating a mild US recession later this year triggered by the tightening in credit conditions. At the same there has been further encouragement that inflation pressures continue to ease (click here). Recent developments give us more confidence that inflation will fall back towards 3.0% by year end. With the Fed’s policy rate already close to 5.0%, a further sharp fall in inflation would lift the real policy rate into more restrictive territory just when the economy is expected to be slowing more sharply. The real policy rate has only been briefly risen above 2.0% over the last twenty years and that was just before the Global Financial Crisis.

The developments should give the Fed more confidence that it has already delivered sufficient rate hikes and can now pause its hiking cycle. In these circumstances, we believe that risks remain titled to the downside for the USD. In our latest monthly FX Outlook report, we doubled down on our bearish USD outlook for this year and now expect it to fall to deeper lows. A break above the 1.1000 level opens up the door for EUR/USD to move towards our updated forecast of 1.1500. Please see our latest FX Weekly report for more details (click here) in which we also recommended adding a new short USD/CAD trade position.

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

SZ |

09:00 |

Total Sight Deposits CHF |

Apr-14 |

-- |

532.2b |

!! |

|

IT |

09:00 |

CPI EU Harmonized YoY |

Mar F |

8.2% |

8.2% |

!! |

|

CA |

13:30 |

Int'l Securities Transactions |

Feb |

-- |

4.21b |

!! |

|

US |

13:30 |

Empire Manufacturing |

Apr |

- 18.0 |

- 24.6 |

!! |

|

US |

15:00 |

NAHB Housing Market Index |

Apr |

45.0 |

44.0 |

!! |

|

EC |

16:00 |

ECB's Lagarde Speaks |

!!! |

|||

|

US |

21:00 |

Net Long-term TIC Flows |

Feb |

-- |

$31.9b |

!! |

Source: Bloomberg