USD consolidating ahead of busy week of central bank meetings

EUR/USD: Fed policy update & German fiscal plans in focus

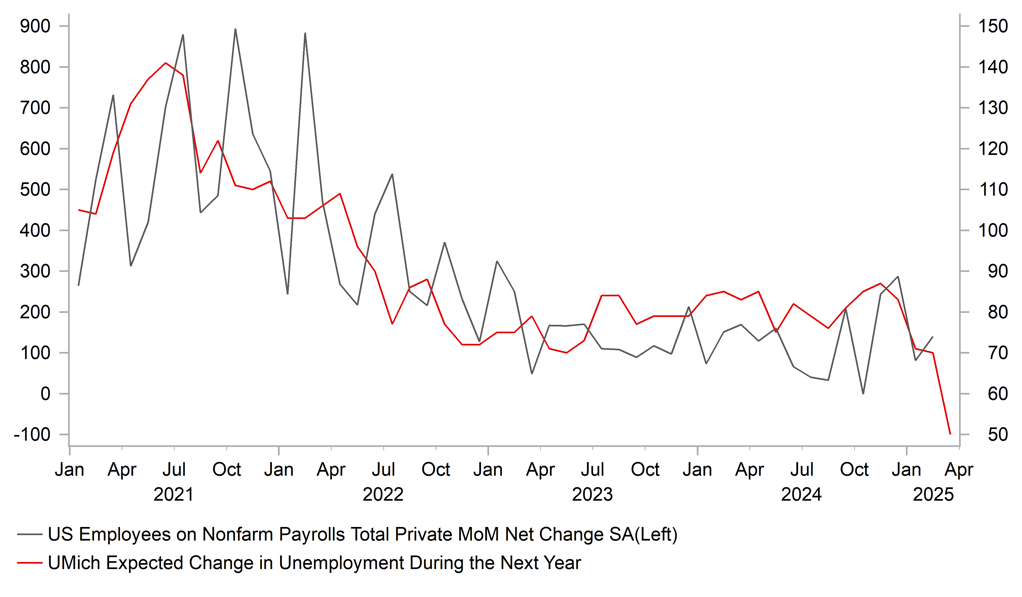

It has been a quiet start to the week for the major FX rates ahead of a busy schedule of G10 central bank meetings this week including the BoJ and Fed on Wednesday followed closely by the SNB, Riksbank and BoE on Thursday. Ahead of those policy updates the US dollar is continuing to consolidate at weaker levels against other major currencies with the dollar index trading just below the 104.00-level. The SNB is expected to be the only central bank to adjust rates this week so market participants will be mainly focusing on updated policy communication from the BoJ, Fed, Riksbank and BoE. We expect the Fed to stick to recent communication that they are not in a rush to lower rates further at the current juncture as they take more time to assess how President Trump’s economic policies are likely to affect the outlook for the US economy. The release on Friday of the latest University of Michigan consumer confidence survey revealed another worrying drop in March. The more forward looking expectations component dropped sharply 9.8 points to 54.2 in March extending its decline from the peak in November to 22.7 points. The current reading for March is the lowest since July 2022 and will heighten concerns over a more sustained slowdown in consumer spending this year. Consumer confidence has been undermined by a sharp rise in measures on inflation expectations and more concern over the health of the labour market at the start of Trump’s second term. The 5-10 year measure of inflation expectation in the UoM survey has jumped up to 3.9% reaching the highest level since the start of 1993. There has also been a sharp rise in the number of respondents who expect unemployment to be higher over the next 12 months. It has resulted in the unemployment index falling to its lowest level since the Global Financial Crisis in 2009. While we don’t think the Fed will overreact to the recent sharp deterioration in consumer confidence measures, it could encourage the Fed to adopt a more cautious tone over the outlook for the US economy this week potentially weighing on the US dollar. The US rate market has already brought forward the timing of the next Fed rate cut to the June FOMC meeting, and is weighing up whether the Fed will deliver two or three more rate cuts this year.

The US dollar has been undermined as well recently by building investor optimism over the outlook for growth outside of the US especially in Europe. There was more good news at the end of last week after it was reported that German Chancellor-in-waiting Friedrich Merz reached an agreement with the Green party on plans to significantly boost defence and infrastructure spending. He triumphantly told reporters that “Germany is back” after meeting with lawmakers. The agreement with the Greens included earmarking EUR100 billion of the proposed EUR500 billion public infrastructure fund to go to the existing climate and transformation fund. Proposed funding will also be extended to 12 years instead of the panned 10 years. Now that the parties have an agreement, the plans are expected to pass through parliament this week when the Bundestag votes on Tuesday. In the current parliament, the CDU/CSU bloc, SPD and Greens control 520 seats which is 31 more than the 489 seats needed for a supermajority. The euro and Bund yield initially rallied once more in response to the agreement with the Greens lifting EUR/USD and Bund yields to highs of 1.0912 and 2.94% respectively on Friday but they have failed to hold on to those initial gains. The price action highlights that the euro is now better priced to reflect the upcoming shift to much looser fiscal policy in Germany. The euro has already strengthened by almost 5% against the US dollar this month. Similarly, the 10-year German Bund yield has already risen by almost 50bps.

US CONSUMER CONFIDENCE REFLECTS FEARS OVER LABOUR MARKET

Source: Bloomberg, Macrobond & MUFG GMR

GBP: BoE to stick to plans for quarterly rate cuts as UK inflation picks up

The pound has outperformed alongside other European currencies this month benefitting from the significant improvement in investor sentiment towards the region. It has helped to lift cable back up towards the 1.3000-level for the first time since last year’s US election. In contrast, the pound has weakened modestly against the euro lifting EUR/GBP back above the 0.8400-level for the second time this year. The euro is expected to benefit more than the pound from Germany’s plans for looser fiscal policy (click here). The last time EUR/GBP rose above 0.8400 in January it was driven more by negative sentiment towards the pound reflecting concerns over UK government debt.

Market participants now expect monetary policies between the ECB and BoE to diverge less going forward which has helped to narrow yield spreads in favour of a stronger euro. At the ECB’s last policy meeting (click here) they left the door open for further modest rate cuts with the policy rate now closer to the neutral estimate put forward by President Lagarde between 1.75% and 2.25%. Based on our assumption that legislation is passed tomorrow to boost fiscal policy in Germany, it will ease pressure on the ECB to lower rates below neutral. The main risk to that view would be a much bigger hit to growth in Europe from President Trump’s upcoming plans for trade tariffs in early April. The EU’s decision to quickly retaliate by imposing tariff hikes from next month on EUR26 billion of US imports in response to US tariff hikes on steel and aluminium imports has angered President Trump, and he has since threatened to impose 200% tariffs on over USD10 billion of alcohol imports from the EU. In contrast, the Trump administration has praised the UK government for their decision not to retaliate. It will further encourage market expectations that the UK economy will not be hit as hard by further tariff hikes in the coming months.

Market expectations for BoE policy have recently been relatively more stable than for the ECB. The UK rate market is still expecting the BoE to stick to the current quarterly pace of rate cuts by delivering the next rate cut in May (19bps of cuts priced in) and then again in August (44bps of cuts priced in). However, there is less confidence that rates will fall further below 4.00% by the end of this year. It is helping to keep yields in the UK at higher levels than on offer in other major economies providing support for the GBP. The BoE holds their latest policy meeting on Thursday. Ahead of that meeting UK economic data has been improving with the exception of Friday’s softer UK GDP report for January. Overall it points to strengthening growth momentum since late year. At the same time the slowdown in services inflation and wage growth remains frustratingly slow. It will become more uncomfortable for the BoE to keep cutting rates heading into the summer when inflation is expected to temporarily pick up towards 4.0%. Overall, the pound remains attractive. A deeper sell-off for global equity markets that undermines financial stability poses the main downside risk for the pound. Please see our latest FX Weekly (click here) for more details.

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

IT |

09:00 |

Italian CPI (YoY) |

Feb |

1.7% |

1.5% |

! |

|

GE |

11:00 |

German Buba Monthly Report |

-- |

-- |

-- |

! |

|

CA |

12:15 |

Housing Starts |

Feb |

246.0K |

239.7K |

!! |

|

GE |

12:15 |

German Buba Mauderer Speaks |

-- |

-- |

-- |

!! |

|

US |

12:30 |

NY Empire State Manufacturing Index |

Mar |

-1.90 |

5.70 |

!! |

|

US |

12:30 |

Retail Sales (MoM) |

Feb |

0.6% |

-0.9% |

!!! |

|

GE |

13:45 |

German Current Account Balance n.s.a |

Jan |

-- |

24.0B |

! |

|

US |

14:00 |

Business Inventories (MoM) |

Jan |

0.3% |

-0.2% |

!! |

|

US |

14:00 |

NAHB Housing Market Index |

Mar |

42 |

42 |

! |

|

EC |

14:00 |

ECB President Lagarde Speaks |

-- |

-- |

-- |

!! |

|

US |

18:00 |

Atlanta Fed GDPNow |

Q1 |

-2.4% |

-2.4% |

!! |

Source: Bloomberg