Fed opens door to rate hikes & stronger USD

USD: Fed update encourages rate hike expectations despite US-Iran deal

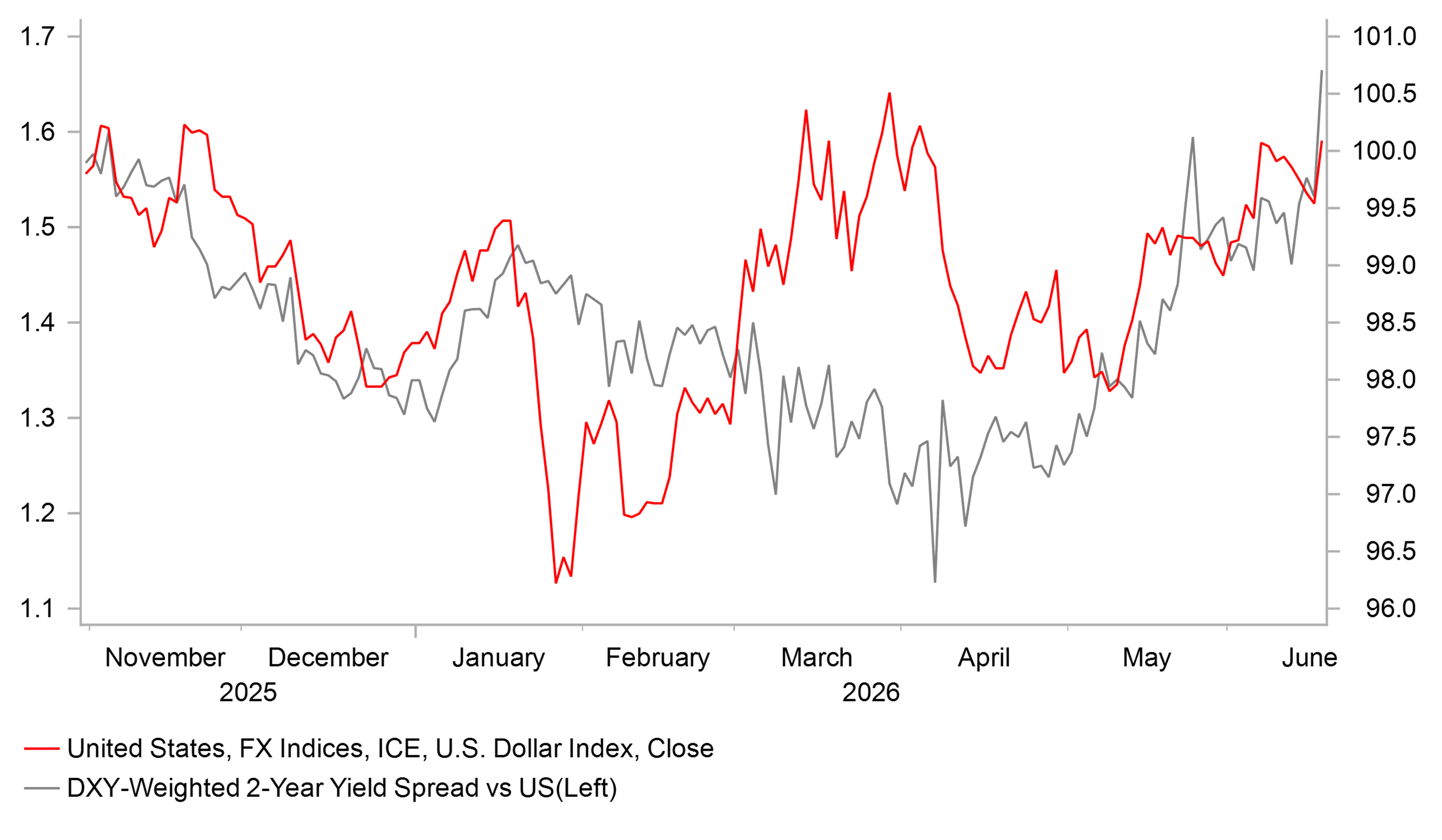

The US dollar has continued to trade at stronger levels overnight after strengthening sharply in response to yesterday’s hawkish Fed policy update. It has helped to lift the dollar index back above the 100.00-level and back closer to the year to date high of 100.643 recorded on 31st March. The Fed’s hawkish policy update is threatening to trigger a bullish break out for the US dollar more than offsetting the dampening impact from the US-Iran deal announcement over the weekend. The US dollar has derived support from the sharp adjustment higher for short-term US rates. The 2-year US Treasury yield has jumped higher by around by 10-12 basis points after yesterday’s FOMC meeting and has hit its highest rate since February of last year. Market participants have moved both to price back in multiple rate hikes from the Fed, and brought forward expectations for the timing of the first hike to September/October. A rate hike even as early as the next policy meeting in July is now judged as around a 1 in 3 probability.

The hawkish repricing of Fed rate hike expectations has mainly been driven by the update DOT plot showing that nine out of eighteen FOMC participants favoured raising rates this year. Of which three favoured hiking rates by 25bps, five favoured hiking rates by 50bps and one favoured hiking rates by 75bps. Out of the remaining nine FOMC members; eight favoured leaving rates on hold and one favoured a 25bps rate cut. There was one DOT missing as new Fed Chair Kevin Warsh chose not to participate in providing forward guidance consistent with his plan to change how the Fed communicates policy under his leadership. The updated DOT plot marks a significant shift from the last set of projections provided back in March when no FOMC participants wanted to raise rates. The change in views among FOMC participants has increased the likelihood of a modest tightening in response to the energy price shock although a rate hike is not a done deal. If the US-Iran deal leads to the Strait of Hormuz reopening soon and lower energy prices, and there is limited evidence of second round effects emerging then the Fed can still leave rates on hold this year. The price of oil is continuing to correct lower and has fallen back below USD80/barrel this week creating more scope for the Fed to look through the near-term pick-up in inflation. At the same time, the updated DOT plot continued to show that over the next two to three years the majority of FOMC members still favour lowering rates back closer to estimate of the neutral policy rate at just above 3.00%.

The hawkish message from the updated DOT plot was reinforced by the lack of pushback from new Fed Chair Kevin Warsh. In his first press conference as Fed Chair he stressed the Fed’s “commitment to deliver on our price stability objective of 2.0%” and argued that “inflation is a choice”. At the same time when asked about whether the Fed’s policy stance is currently restrictive, he described it as “uneven”. While he dd not provide a strong signal over policy direction given he is not a supporter of forward guidance, his comments on the whole indicate that he wants to create the impression that he will not be soft on above target inflation which leaves the door open to tighter policy if required. If he had indicated that he favours looking through the energy price shock and leaving rates on hold, it would have pushed back more strongly against the hawkish message from the updated DOT plot.

On top of the immediate changes to the Fed’s forward guidance including a much shorter statement which leaves the policy outlook less clear, Kevin Warsh has announced he has set up five task forces as part of a broad review of how the Federal Reserve operates. The five task forces will cover: i) communications, ii) the balance sheet, iii) data sources, iv) productivity, jobs & AI, and v) inflation framework. Early insights are expected in few months and final reviews targeted by the end of the year. The reviews will add to expectations for a bigger shake up in how the Fed operates including a shift towards running a smaller balance sheet.

Overall, the Fed’s hawkish policy update should help to keep US rates and the US dollar at higher levels heading into the summer. If the Fed follows through and hikes rates it would reinforce the Fed’s upward momentum. We are not convinced though that a rate hike will be required, but acknowledge that there is a higher risk of rate hike in the second half of this year. It poses upside risks to our forecast (click here) for a weaker US dollar heading into next year.

YIELD SPREADS MOVING IN FAVOUR OF STRONGER USD

Source: Bloomberg, Macrobond & MUFG Research

GBP: BoE rate hike expectations pared back ahead of MPC meeting & Makerfield by-election

The pound has traded on a softer footing ahead of today’s BoE policy meeting and UK by-election in Makerfield. It has resulted in cable falling to low yesterday of 1.3262, and EUR/GBP rising back above 0.8650. The weaker pound has been driven in part by lower UK rates as market participants have scaled back BoE rate hike expectations. The 2-year gilt yield has fallen by around 20bps over the past week in response to both the US-Iran deal and the softer Uk CPI report for May. Lower energy prices and little evidence so far of inflation pressures broadening out in the UK are helping to ease pressure on the BoE to response to the energy price shock by tightening policy. Today’s Uk labour market report continued to reveal that the labour market remains soft even though employment was stronger than expected. Payrolled employment increased marginally by 2k in May and the -100k drops in April was revised up to a still large drop of -53k. At the same time, the report revealed that private sector regular wage growth slowed further to 2.9% in April from 3.1%. The soft labour market should continue to dampen concerns over second round inflation effects from the energy price shock. In light of recent developments, we are less convinced that the BoE will raise rates this year. At today’s policy meeting, we expect the BoE to leave rates on hold and reiterate it still has time to assess how the economy is evolving. The vote is expected to show MPC member Megan Greene joining Chief Huw Pill in voting for a hike. If there is any indication that the BoE is closer to a hike as soon as next month, it would deliver a hawkish policy surprise similar to the Fed’s policy update overnight offering more support for the pound.

The paring back of BoE rate hike expectations and decline in inflation expectations should keep downward pressure on gilt yields, and offset upside risks from political developments in the UK. Andy Burnham’s bid to become the next leader of the labour party faces a key test today. Opinion polls show he holds a 5-12ppt lead in the by-election, although the contest could prove closer than expected. If he wins it has been reported that he would immediately put pressure on Prime Minister Starmer to lay out a plan to hand over power. If Starmer is not willing to step aside a formal leadership challenge will be required. The aim is for Burnham to be in charge by the Labour party conference in September. The gilt market is more comfortable with the idea of Burnham becoming leader after he indicated he would stick to the government's fiscal rules limiting ability to loosen fiscal policy. Nevertheless, political uncertainty could act as a headwind for gilts and the pound. Uncertainty would arguably be even higher if he loses the by election. In that scenario we still expect Starmer’s time in power to come to an end, and an alternative soft left candidate who is already an MP would rise up to mount a leadership challenge like for Deputy Prime Minister Angela Rayner. Overall, we expect any pound sell-off in response to UK politics to be modest at this stage.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

CH | 08:30 | SNB Interest Rate Decision | (Q2) | 0.00% | 0.00% | !!! |

CH | 08:30 | SNB Monetary Policy Assessment | - | - | - | !! |

NO | 09:00 | Interest Rate Decision | - | 4.25% | 4.25% | !! |

CH | 09:30 | SNB Press Conference | - | - | - | !!! |

GB | 12:00 | BoE Interest Rate Decision | (Jun) | 3.75% | 3.75% | !!! |

US | 13:30 | Initial Jobless Claims | - | 225K | 229K | !!! |

US | 21:00 | Overall Net Capital Flow | (Apr) | - | 150.70B | ! |

US | 21:30 | Fed's Balance Sheet | - | - | 6,725B | !! |

Source: Bloomberg & Investing.com