60-40 split decision – FOMC should cut by 50bps

USD: FOMC decision finely balanced

The FOMC announcement this evening remains finely balanced with the OIS market showing 40bps of cuts priced for this evening – indicating a 60% probability between 25bps and 50bps. USD/JPY has jumped 0.6% since the retail sales data yesterday while the 2-year UST note yield is 5bps higher. So some conviction on a 50bp cut has faded on the back of the data release given the limited signs of decelerating consumer spending. The Control Group Retail Sales 3mth average annualised rate picked up from 4.9% in July to 5.7% in August. In the last five months there has been a notable pick-up from a low of 1.3% underlining the still resilient US consumer.

Still, a decision on cutting rates by 25bps or 50bps must take a more forward-looking assessment of the economy and the risks to the dual-mandate. Real disposable income is currently growing at just 1.1% (July) and since February has averaged just 1.2%. This level of real disposable income coincides has been running against real consumer spending rates that have averaged 2.5% over the same period. This is unsustainable as it implies an erosion of savings that will need to be replenished going forward. A slowdown in real consumer spending very likely lies ahead.

The Summary of Economic Projections released tonight with the FOMC rate decision will likely show a more notable slowdown than what was published in June – then the FOMC forecast a slowdown from 2.1% this year to 2.0% next year. This seems highly unlikely given the probable real consumer spending slowdown. We will also likely see the PCE inflation readings for year-end come down too from a headline rate of 2.6% and a core rate of 2.8%. The unemployment rate for Q4 at 4.0% will be revised higher.

Our call remains that the FOMC will cut by 50bps tonight with a guidance and message that implies the FOMC is taking out some degree of insurance in getting the monetary stance back toward neutral in a timely fashion given the focus of the dual-mandate has shifted from too high inflation to too high unemployment. Cutting 50bps now also makes sense given the FOMC have the SEPs to outline more clearly to the markets that they are being pre-emptive rather than believing they have fallen behind the curve. That can be shown of course through a median dot profile for the 2024 fed funds rate implying 100bps of cuts in total, meaning two further 25bp cuts in November and December. The Fed was too late in starting the tightening cycle and in 2022 and the danger with cutting by 25bps is that global investors could quickly fear the Fed being behind the curve.

If our view materialises tonight we would expect to see the 2s10s curve steepen to new cyclical highs not seen since June 2022 while USD/JPY will likely break back below the 140-level and possible reach new lows quickly. A 25bp cut could see the current USD/JPY move higher extended but given the risk then of higher risk aversion and possibly increased financial market volatility we suspect any move higher will fade quickly.

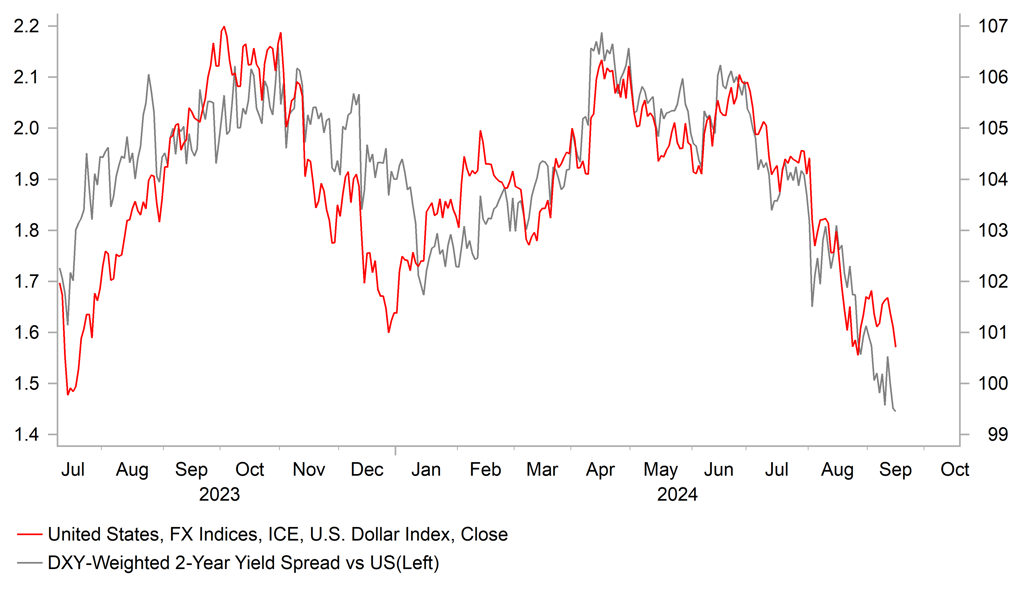

DXY VERSUS DXY-WEIGHTED 2YR YIELD SPREAD

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Inflation no signal for surprise BoE cut

A larger 50bp rate cut from the Fed tonight would likely lead to increased speculation of a rate cut from the BoE tomorrow. The OIS market currently implies a 25% probability of a 25bp cut. The UK inflation data for August has just been released and is unlikely to trigger any big shift in BoE rate cut expectations given the 0.3% m/m gain and 2.2% y/y gain were exactly in line with expectations. The core CPI y/y rate picked up as expected from 3.3% to 3.6% with services CPI y/y up from 5.2% to 5.6%. The largest upward contribution to CPI came from airfares with transport up 1.2% y/y compared to just 0.1% in July. That reflected a big swing in the annual rate of increase for airfares, from -10.4% in July to +11.9% in August. This huge swing reflected a 22.2% m/m increase in airfares and while there is usually a jump at that time of the year, the m/m increase was the second largest since the data series began in 2001.

The good news on the services side was the slide in restaurant and hotels, which in y/y terms slowed from 4.9% to 4.4%, the lowest rate since July 2021. On a m/m basis, prices fell 0.7%. In terms of contribution to the annual rate of increase, restaurant and hotels was the largest negative drag. Easing momentum could be a sign of further slowdown in services-related demand in the sector that would go some way to easing “sticky” inflation pressures further. Governor Bailey has already stated that the confidence within the MPC of “sticky” inflation subsiding is rising and in that sense this element of the data will help encourage the expected rate cut in November.

Overnight implied volatility in GBP has surged to the highest level since 2nd August last year which was the day before an MPC meeting. With the FOMC and the BoE today and tomorrow we could well see increased price action. However, we suspect the US dollar leg will drive any volatility after today’s meeting rather than the GBP leg following the BoE meeting tomorrow. Today’s inflation data does not warrant any justification for a surprise cut tomorrow.

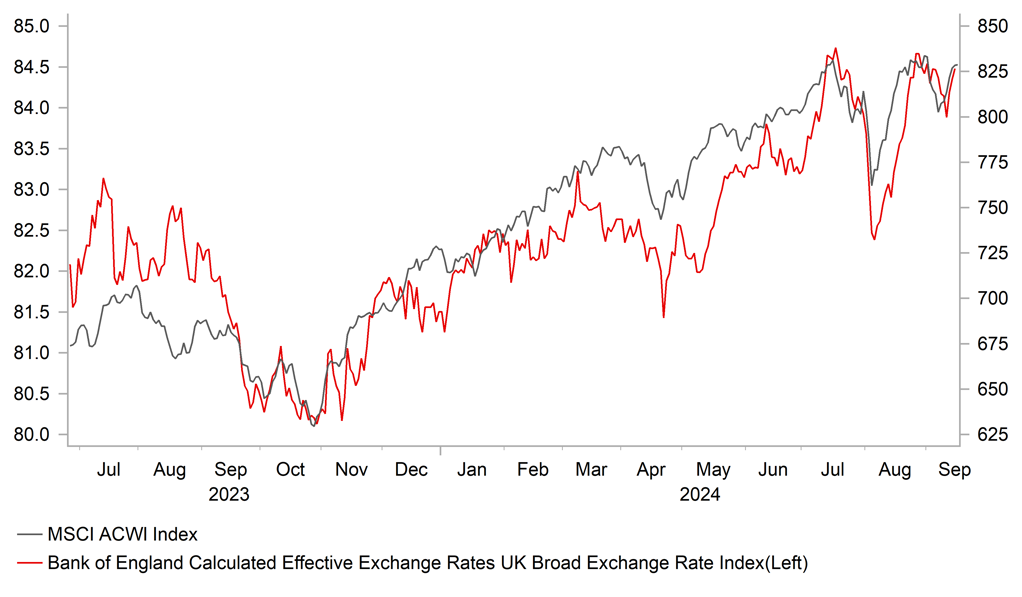

GBP LIKELY TO ADVANCE FURTHER IF POSITIVE RISK RESPONSE TO FOMC TONIGHT

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

UK |

09:30 |

House Price Index (YoY) |

-- |

2.8% |

2.7% |

! |

|

EC |

10:00 |

Core CPI (YoY) |

Aug |

2.8% |

2.9% |

!! |

|

EC |

10:00 |

Core CPI (MoM) |

Aug |

0.3% |

-0.2% |

!! |

|

EC |

10:00 |

CPI (YoY) |

Aug |

2.2% |

2.6% |

!! |

|

EC |

10:00 |

CPI (MoM) |

Aug |

0.2% |

0.0% |

!! |

|

EC |

10:00 |

HICP ex Energy & Food (YoY) |

Aug |

2.8% |

2.8% |

! |

|

EC |

10:00 |

HICP ex Energy and Food (MoM) |

Aug |

0.3% |

-0.1% |

! |

|

US |

12:00 |

MBA Mortgage Applications (WoW) |

-- |

-- |

1.4% |

! |

|

US |

13:30 |

Building Permits |

Aug |

1.410M |

1.406M |

!! |

|

US |

13:30 |

Housing Starts |

Aug |

1.310M |

1.238M |

!! |

|

CA |

13:30 |

Foreign securities Purchases |

Jul |

-- |

5.17B |

! |

|

CA |

13:30 |

For Securities Purchases by Canadians |

Jul |

-- |

16.350B |

! |

|

CA |

18:30 |

BOC Summary of Deliberations |

-- |

-- |

-- |

!! |

|

US |

19:00 |

FOMC Economic Projections |

-- |

-- |

-- |

!!!!! |

|

US |

19:00 |

FOMC Statement |

-- |

-- |

-- |

!!!!! |

|

US |

19:00 |

Fed Interest Rate Decision |

-- |

5.25% |

5.50% |

!!!!! |

|

US |

19:30 |

FOMC Press Conference |

-- |

-- |

-- |

!!!!! |

|

US |

21:00 |

US Foreign Buying, T-bonds |

Jul |

-- |

9.80B |

! |

Source: Bloomberg