Reciprocal tariff plan – uncertainties will likely persist

USD: Scope for US dollar to strengthen

President Trump’s so-called “Liberation Day” has arrived and an announcement is scheduled for the Rosa Garden at 4pm Washington time when all will be revealed in terms of the tariff actions against the US’s trading partners. President Trump stated on Sunday that the plan will cover “essentially all” countries but then on Monday stated that the plan would be “very nice, relatively speaking” and again emphasised the word “reciprocal” as “very important, what they do to us we do to them”. But that is a very difficult measure to benchmark in reality with the US free to basically do what it wants. The Office of the US Trade Representative (USTR) on Monday released its annual National Trade Estimate Report, which highlights country-by-country trade barriers amongst 40 US trading partners. As an indication of how broad trade barriers can be, the report highlights 14 different metrics that determine the extent of trade barriers for US exports into foreign markets, ranging from subsidies to tech-sector barriers to government procurement policies to labour and environment laws. These metrics will likely be cited today by President Trump as factors that were taken into account when setting country tariffs. According to White House Press Secretary Karoline Leavitt, sector-specific tariffs will not be the focus of today’s announcements with broad country-level tariffs the main tariff plan. If that’s the case, the countries given greatest focus in the USTR’s National Trade Estimate Report could very well be the countries that are hit most aggressively with tariffs – likely to be around the 20% to 25% level.

If that is the basis of action then China received greatest focus in this report (48 of the 397-page report) with the EU next (34 pages), India (16), Russia (15), Indonesia (14), Japan & Turkiye (11), the Philippines (9), Vietnam (8), South Korea and Mexico (7), and Canada and a number of other countries (6). A lot of these countries would also be included in another group referred to by Treasury Secretary Scott Bessent as the “dirty 15” – the 15% of nations that account for the bulk of US trading volumes.

We see some key aspects that will determine whether the financial markets interpret the announcements as aggressive or not. A wide blanket tariff globally capturing all the major trading partners with a 20%-25% tariff would be seen as most aggressive and likely illicit the biggest risk-off reaction. But there has been speculation that discussions on trade deals could exclude certain countries (the UK?) and the more examples of that the better the markets can take the announcements. Also, does China escape the scale of action compared to others given two 10% tariffs have already been announced? Trump may go with a smaller 10% tariff on most countries which would also be taken better by the markets and would help reduce risk aversion. Finally, does Canada and Mexico escape the same scale of action given they are in the USMCA? Again, that would be good news for investors.

All told, we believe the financial markets are under-estimating the scale of action. Global rates are falling but CAD, AUD, NOK and SEK outperformed yesterday, hardly signs of tariff concerns and rising risks of global trade disruptions. We may well be set for some reversal of these currencies outperforming if the US delivers a more aggressive plan of tariff action than the markets seem to be fearing.

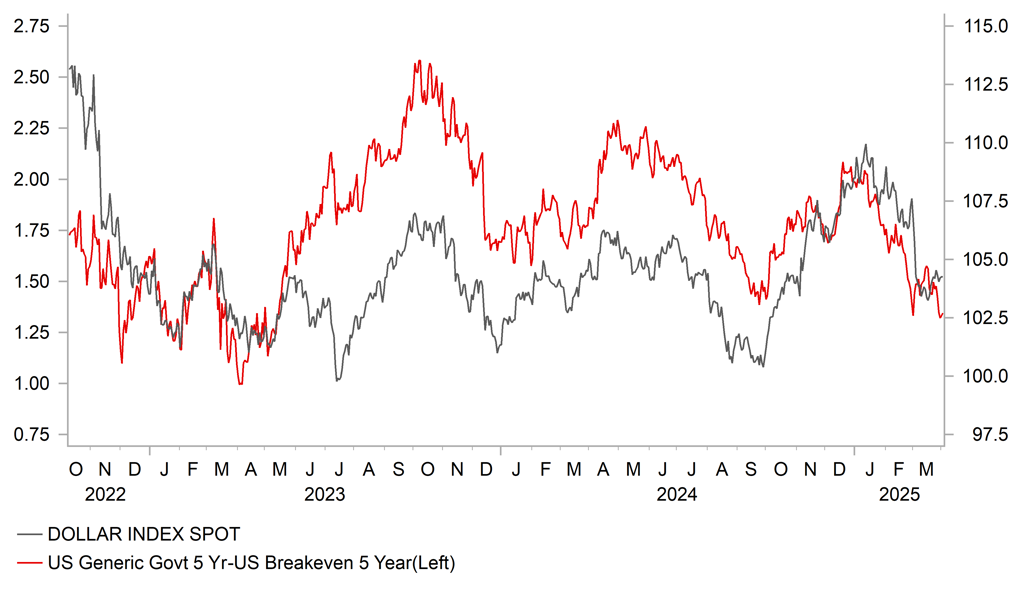

UST 5-YEAR REAL YIELD HAS DECLINED TO A NEW LOW – THE LOWEST SINCE MAY 2023 AS GROWTH FEARS ESCALATE

Source: Bloomberg, Macrobond & MUFG GMR

USD: Growth concerns may take a back seat initially

The announcement of the reciprocal tariff plan comes against a backdrop of worsening economic data which has been the key factor behind the change in financial market reaction to tariff news from US dollar supportive to dollar negative. Might President Trump come to regret the change in sequencing of policy implementation? In his first term in office, tax cuts came first, tariffs second. The economy now is certainly more vulnerable although we see that as more than just down to policy sequencing. The US economy is at a different point in the economic cycle than in 2017-19 which likely means a lot more damage for the economy from tariffs this time around.

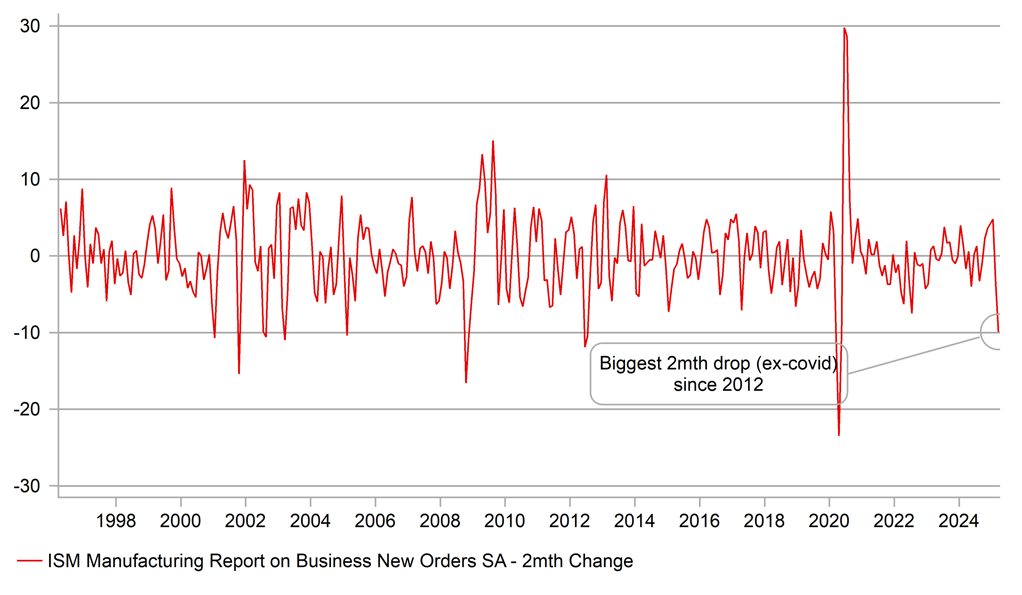

That was evident yesterday with the ISM manufacturing report underlining the deterioration in business sentiment in anticipation of tariffs being implemented. While the overall ISM manufacturing index fell modestly from 50.3 to 49.0, the New Orders index fell sharply from 48.6 to 45.2. Over a 2-month period, new orders have fallen by the most since 2012 when the covid period is excluded. The Prices Paid index surged by 7.0ppts and again over a 2-month period the jump was the largest since January 2021 ahead of the global inflation shock.

If this mix of economic data persists, what would it mean for the FOMC? There would surely be greater initial risks of the FOMC delaying a decision to cut rates again. Market pricing implies a still high degree of confidence of a rate cut in June (80% probability) but whether the FOMC will have had enough inflation info to be confident of only a temporary impact from tariffs is questionable. Chicago Fed President Goolsbee stated yesterday in an interview that tariff-related uncertainty “is tinged with fears over inflation” given it will be difficult to determine how lasting an inflation impact might be. We still expect the FOMC to cut two-to-three times this year although there are risks that the FOMC could delay longer than implied by market pricing and that could add to the potential for the dollar to recover over the coming months.

BIGGEST 2MTH CHANGE IN ISM MANUFACTURING NEW ORDERS SINCE 2012

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

GE |

10:30 |

German 10-Year Bund Auction |

-- |

-- |

2.920% |

!! |

|

EC |

11:30 |

ECB's Schnabel Speaks |

-- |

-- |

-- |

!! |

|

US |

12:00 |

MBA Mortgage Applications (WoW) |

-- |

-- |

-2.0% |

! |

|

US |

13:15 |

ADP Nonfarm Employment Change |

Mar |

118K |

77K |

!!!! |

|

US |

15:00 |

Durables Excluding Defense (MoM) |

Feb |

0.8% |

0.8% |

! |

|

US |

15:00 |

Durables Excluding Transport (MoM) |

Feb |

-- |

0.7% |

! |

|

US |

15:00 |

Factory Orders (MoM) |

Feb |

0.5% |

1.7% |

!! |

|

US |

15:00 |

Factory orders ex transportation (MoM) |

Feb |

0.7% |

0.2% |

! |

|

US |

15:00 |

Total Vehicle Sales |

Mar |

15.90M |

16.00M |

! |

|

EC |

15:05 |

ECB's Lane Speaks |

-- |

-- |

-- |

!!! |

|

IT |

17:00 |

Italian Car Registration (YoY) |

Mar |

-- |

-6.2% |

! |

|

EC |

19:45 |

ECB President Lagarde Speaks |

-- |

-- |

-- |

!!! |

|

US |

20:00 |

Reciprocal tariff plan announced |

-- |

-- |

-- |

!!!!! |

|

US |

21:30 |

FOMC Member Kugler Speaks |

-- |

-- |

-- |

!!! |

Source: Bloomberg