Market focus shifting back to inflation and away from banking concerns

NZD: RBNZ closer to rate hike pause as inflation slows further

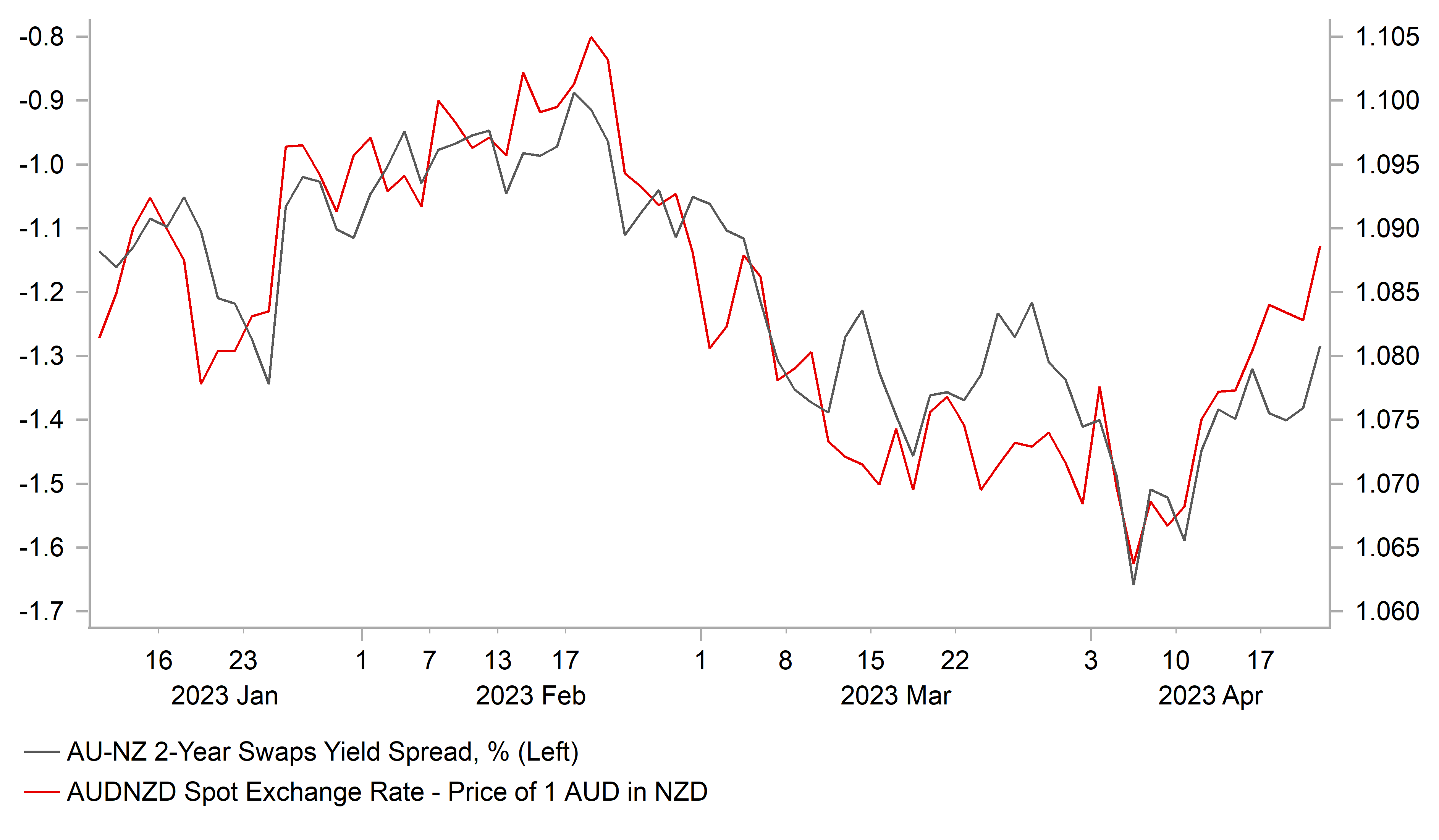

The worst performing G10 currency overnight has been the New Zealand dollar following the release of the latest CPI report from New Zealand. It has resulted in the NZD/USD rate falling back below support from the 200-day moving at around 0.6160, and the AUD/NZD rate has extended its recent advance up to the 1.0900-level. The latest CPI report revealed that the inflation slowed unexpectedly for the second consecutive quarter from 1.4%Q/Q in Q4 of last year to 1.2% in Q1 of this year. It was the slowest quarterly increase in headline inflation since Q1 2021. The annual rate of headline inflation also slowed to 6.7% in Q1 as it moved further below the peak from Q2 of last year at 7.3%. It will be a notable surprise for the RBNZ who had been expecting the annual rate of headline inflation to remain at around 7.3%. The report will give the RBNZ more confidence that inflation peaked at around the turn of the year which increases the likelihood that the RBNZ could pause their rate hike cycle at their next policy meeting on 24th May. The RBNZ has already lifted their policy rate into more restrictive territory at 5.25% after delivering a larger 50bp hike at their last meeting. The impact of past monetary tightening is already becoming more evident with New Zealand’s economy expected to fall into recession this year following on from the –0.6%Q/Q contraction in Q4 of last year. The RBNZ will still be concerned though that inflation remains uncomfortably above their 1-3% target band despite the slowdown in recent quarters, and that domestic (non-tradable) inflation picked up in Q1 to an annual rate of 6.8% in Q1. It still leaves open the possibility that the RBNZ will deliver one final smaller 25bps hike. The New Zealand dollar has been the second worst performing G10 currency this year, and developments overnight will reinforce expectations for further weakness. The AUD/NZD rate has been moving more closely in line with short-term yield spreads, and has been lifted this month by the scaling back of RBNZ rate hike expectations relative to the RBA. There is more room for the RBA’s policy rate to rise further at 3.60% in comparison to the RBNZ’s policy rate at 5.25%.

AUD/NZD VS. SHORT-TERM YIELD SPREAD

Source: Bloomberg, Macrobond & MUFG GMR

USD: Policy divergence to drive further USD weakness

Global yields have been rebounding this week as market participants’ focus continues to shift away from concerns over the health of the banking system and back to the ongoing problem of elevated inflation. In the US, the 2-year Treasury yield hit a high yesterday of 4.28% as it moved further above last month’s low of 3.55%. The US rate market is now fully discounting one final 25bps hike from the Fed, and is no longer fully discounting a 25bps cut by the end of this year. The scaling back of more dovish expectations for Fed policy has offered support for the US dollar although its recent rebound has been relatively modest. The dollar index remains around -3.7% below the peak prior to the collapse of Silicon Valley Bank.

Recent support for the US dollar from the rebound in US yields has been offset by the hawkish repricing of expectations for other major central banks. The release this week of the stronger wage and inflation data from the UK has reinforced expectations that the BoE will deliver another 25bps hike in May and lift the policy rate to a higher peak closer to 5.00%. Similarly, the euro-zone rate market continues to expect the ECB to be more active than the Fed in hiking rates through the rest of this year. ECB officials including Chief Economist Philip Lane have left the door open to another larger 50bp hike next month with the size of the hike depending on incoming data and the latest bank leading survey (2nd May). The release yesterday of the euro-zone CPI report for March confirmed that headline inflation has fallen sharply to 6.9% in March down from 9.2% at the end of last year driven primarily by the energy component that has fallen below the level from a year ago. However, other components remain uncomfortably high with core inflation hitting a fresh high of 5.7% and food inflation rising further to 17.9% in March. We see clearer evidence of disinflation pressures at work in the US than in the euro-zone and UK at the current juncture that supports our expectation that the Fed will pause their hiking cycle first. It is an important reason why we still expect the US dollar to weaken further against other major currencies year. The release of the latest Beige Book survey overnight supported expectations for a Fed pause by revealing the US economy had stalled in recent weeks with access to credit narrowing.

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

12:30 |

ECB Publishes Account of Monetary Policy Meeting |

-- |

-- |

-- |

!!! |

|

US |

13:30 |

Initial Jobless Claims |

-- |

240K |

239K |

!!! |

|

US |

15:00 |

Existing Home Sales |

Mar |

4.50M |

4.58M |

!!! |

|

CA |

16:30 |

BoC Gov Macklem Speaks |

-- |

-- |

-- |

!! |

|

US |

17:00 |

Fed Waller Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg