European central bank (SNB, Norges Bank & BoE) policy updates in focus

GBP: Will sticky services inflation delay BoE rate cut plans?

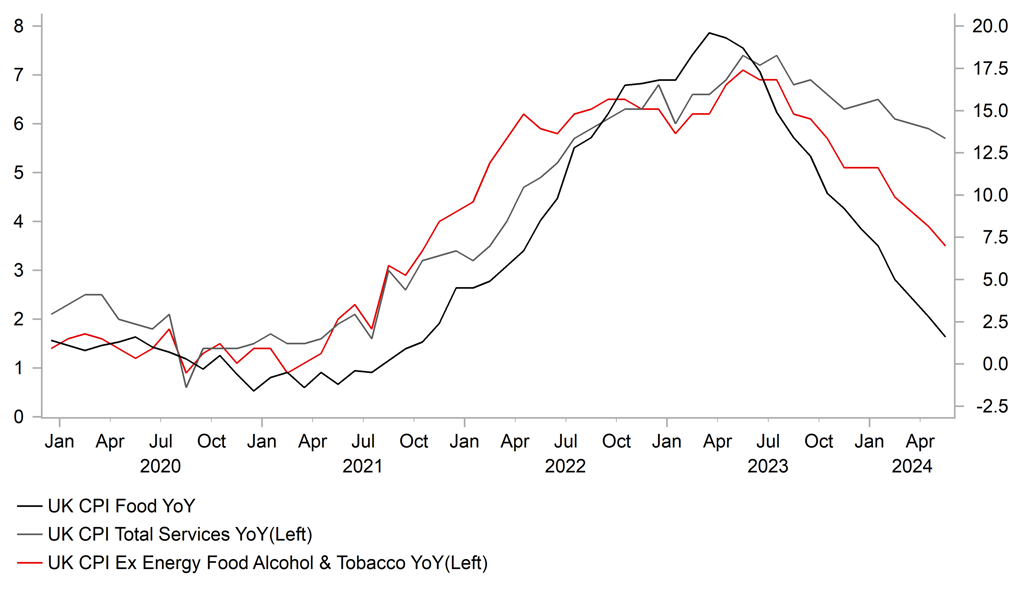

The pound has strengthened modestly ahead of today’s BoE policy meeting encouraged by the release yesterday of the latest UK CPI report for May. It helped to briefly lift cable above 1.2750. The pound has been supported by a further hawkish repricing of BoE rate cut expectations. The probability of the BoE cutting rates as soon as the August MPC meeting has fallen from around 50:50 to less than “I in 3” after the UK CPI report revealed that services inflation is continuing to prove more sticky than expected. Services inflation slowed but only marginally and remained elevated at 5.7% Y/Y in May. It was mainly driven by the volatile categories of hotel prices (+2.0%M/M) and air fares (+14.9%M/M). It leaves services inflation around 40bps higher than the BoE was forecasting back in the May Monetary Policy Report. However, it wasn’t all bad news for the BoE ahead of today’s MPC meeting. Headline inflation and core inflation continued to fall at a faster rate to 2.0% and 3.5% respectively in May. It was the first time in nearly three years that headline inflation had fallen back in line with the BoE’s target. Headline and core inflation are only marginally higher by 10bps than the BoE’s forecasts from the May MPR.

In light of these developments, there is less risk that the BoE will deliver a more dovish policy signal that strongly indicates that they will begin to cut rates at the following MPC meeting in August. We expect the voting pattern to be similar to the last policy in May when there were two dissenters (MPC members Dhingra and Broadbent) who voted for a cut. However, it does not mean that a rate cut as early as in August can be ruled out. With headline inflation set to move below target and core inflation slowing quickly as well alongside building evidence of a softening labour market in the UK, the BoE could still indicate that they are moving closer to cutting rates especially if they display more concern over keeping rates too high for too long which could result in a more marked deterioration labour market conditions. With the UK rate market expecting a largely unchanged policy message, the pound is likely to prove more sensitive to a dovish policy surprise. We doubt that the BoE would feel confident enough to rule out a rate cut in August at the current juncture.

UK INFLATION SLOWING BUT MORE SLOWLY IN SERVICES SECTOR

Source: Bloomberg & Macrobond

CHF: Recent CHF strength could tip balance in favour of back to back rate cuts

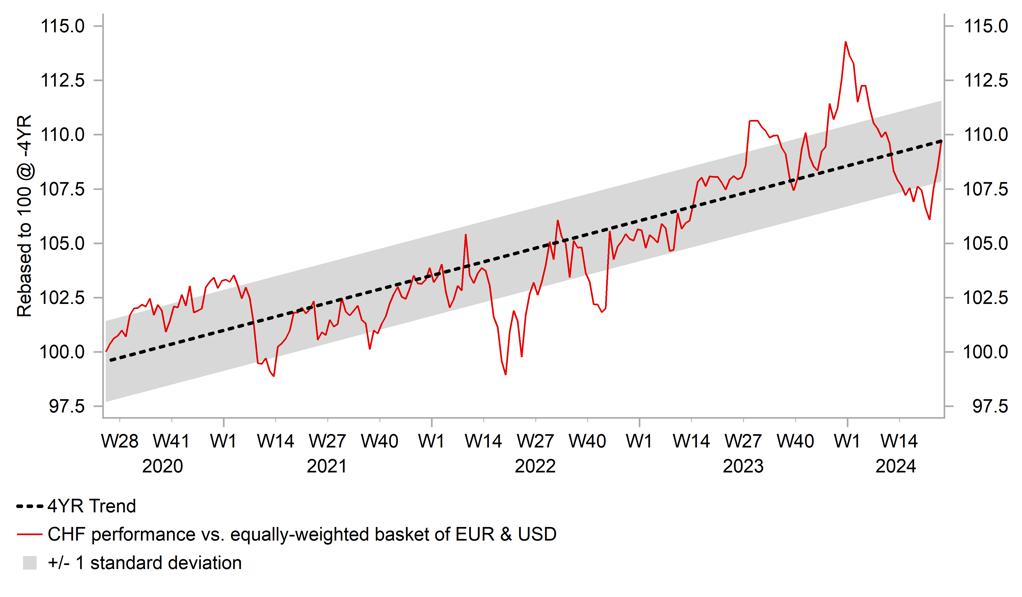

The Swiss franc has been the best performing G10 currency so far this month. It has strengthened by just over 3.0% against the euro resulting in EUR/CHF falling back below the 0.9500-level after it threatened to rise back to parity at the end of May. The sharp reversal of Swiss franc weakness from earlier this year was first triggered by comments from SNB President at the end of May which displayed more concern over upside risks to their inflation outlook from a weaker Swiss franc which he noted they could counteract by “selling foreign exchange”. Market participants also saw the comments as a signal that the SNB may decide to leave rates on hold at today’s policy meeting rather than delivering back to back 25bps rate cuts after they became the first G10 central bank to begin cutting rates in March. The ECB has since followed the SNB when it started to cut rates this month. A decision from the SNB to leave rates on hold today would reinforce the Swiss franc’s current upward momentum and encourage EUR/CHF to move closer to the lows from earlier this year at just below the 0.9300-level.

In light of recent Swiss franc strength the Swiss interest rate market has moved to price back in a higher probability of the SNB cutting rates again today. There are currently around 17bps of cuts priced in for today’s policy meeting. The Swiss franc’s upward momentum has been reinforced over the past week by heightened political risks in Europe which has boosted its regional safe haven appeal. We continue to believe that market participants will remain nervous over the potential outcome from the French elections. As a result even if the SNB decide to deliver back to back rate cuts today, it is unlikely to trigger a sharp reversal of Swiss franc strength. Inflation developments since the SNB’s last policy meeting in March have been in line with their forecasts with the headline rate coming in at 1.4% in both April and May where it is expected to remain through the rest of this year before declining to 1.2% in 2025 and 1.1% in 2026. We are not expecting any major revisions to the SNB’s inflation projections today although a rate cut today could lead to some upward revisions as their forecasts in March were based on the assumption of the policy rate remaining at 1.50%. While the Swiss franc has strengthened sharply so far this month, it is likely too soon for the SNB to make significant downward revisions to the inflation forecasts. However if the Swiss franc were to continue to strengthen sharply in the coming months, it will increase pressure on the SNB to take action by either cutting rates further and/or intervening in the currency market to sell the Swiss franc.

CHF BOUNCES BACK AFTER SHARP SELL-OFF EARLIER THIS YEAR

Source: Bloomberg & Macrobond

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

SZ |

08:30 |

SNB Interest Rate Decision |

Q2 |

1.50% |

1.50% |

!!! |

|

SZ |

08:30 |

SNB Monetary Policy Assessment |

-- |

-- |

-- |

!! |

|

NO |

09:00 |

Interest Rate Decision |

-- |

4.50% |

4.50% |

!! |

|

SZ |

09:30 |

SNB Press Conference |

-- |

-- |

-- |

!!! |

|

UK |

12:00 |

BoE Interest Rate Decision |

Jun |

5.25% |

5.25% |

!!! |

|

UK |

12:00 |

BoE MPC Meeting Minutes |

-- |

-- |

-- |

!!! |

|

US |

13:30 |

Building Permits |

May |

1.450M |

1.440M |

!! |

|

US |

13:30 |

Current Account |

Q1 |

-207.0B |

-194.8B |

!! |

|

US |

13:30 |

Housing Starts |

May |

1.370M |

1.360M |

!! |

|

US |

13:30 |

Initial Jobless Claims |

-- |

235K |

242K |

!!! |

Source: Bloomberg