Banking sector angst and recession fears intensify

USD: Stronger dollar and yen

The angst over the health of regional banks has not gone away and Fed balance sheet data has seen those concerns intensify with a modest increase in the liquidity support offered by the Fed through its discount window and the Bank Term Funding Program. Combined these two bank liquidity supports increased by USD 4.3bn – not a huge increase but enough to underline that these supports are needed and the longer they are used by banks the bigger impact it will have on NIMs given the cost of the liquidity. The S&P 500 fell 0.6% yesterday with the Bank Index down 1.2%.

Investor sentiment had already taken a hit from the data released earlier with the ‘Philly Fed’ business outlook plunging to -31.3, the lowest level since the GFC in 2009 when the covid period is excluded. The tumble is another strong signal that the US is heading for recession. The initial claims data was also signalling labour market weakness with an increase to 245k, close to recent highs and up nearly 50k from the lows recorded in January. The jobs market really is the primary economic reasoning for the Fed to continue tightening and we see the window on that reasoning closely pretty quickly from here which will mean the May FOMC will be when rates are raised for the last time. What is telling from a global growth outlook is the turnaround of crude oil prices since the OPEC+ production cut announcement. That bounce is close to fully reversed now underlining the increasing expectations of weakening growth ahead.

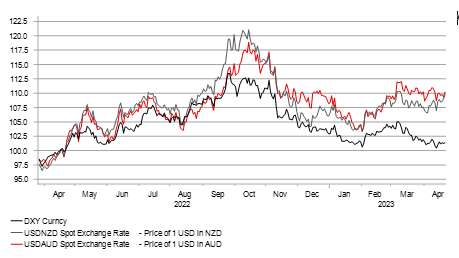

Those increased concerns over global growth has seen some of the higher beta G10 currencies underperform. A clear divergence has opened up between DXY and say for example AUD/USD. Looking at the last year of trading moves, the current level of DXY is more consistent with AUD/USD trading at levels around 0.7100-0.7200. It’s just as apparent in NZD/USD as well with DXY more consistent with NZD/USD trading between 0.6500-0.0.6600. Similarly, USD/CAD has diverged notably as well and when DXY was trading at these levels in June of last year, USD/CAD was trading below 1.2800. This underperformance is likely to remain in place in circumstances of increased recession fears in the US that weighs further on commodity prices. The best performers will continue to be in core G10 and for valuation and Japan-specific factors we continue to see the yen as having the best prospects.

CLOSE TO 8% AUD AND NZD UNDERPERFORMANCE RELATIVE TO DXY

Source: Bloomberg, Macrobond & MUFG GMR

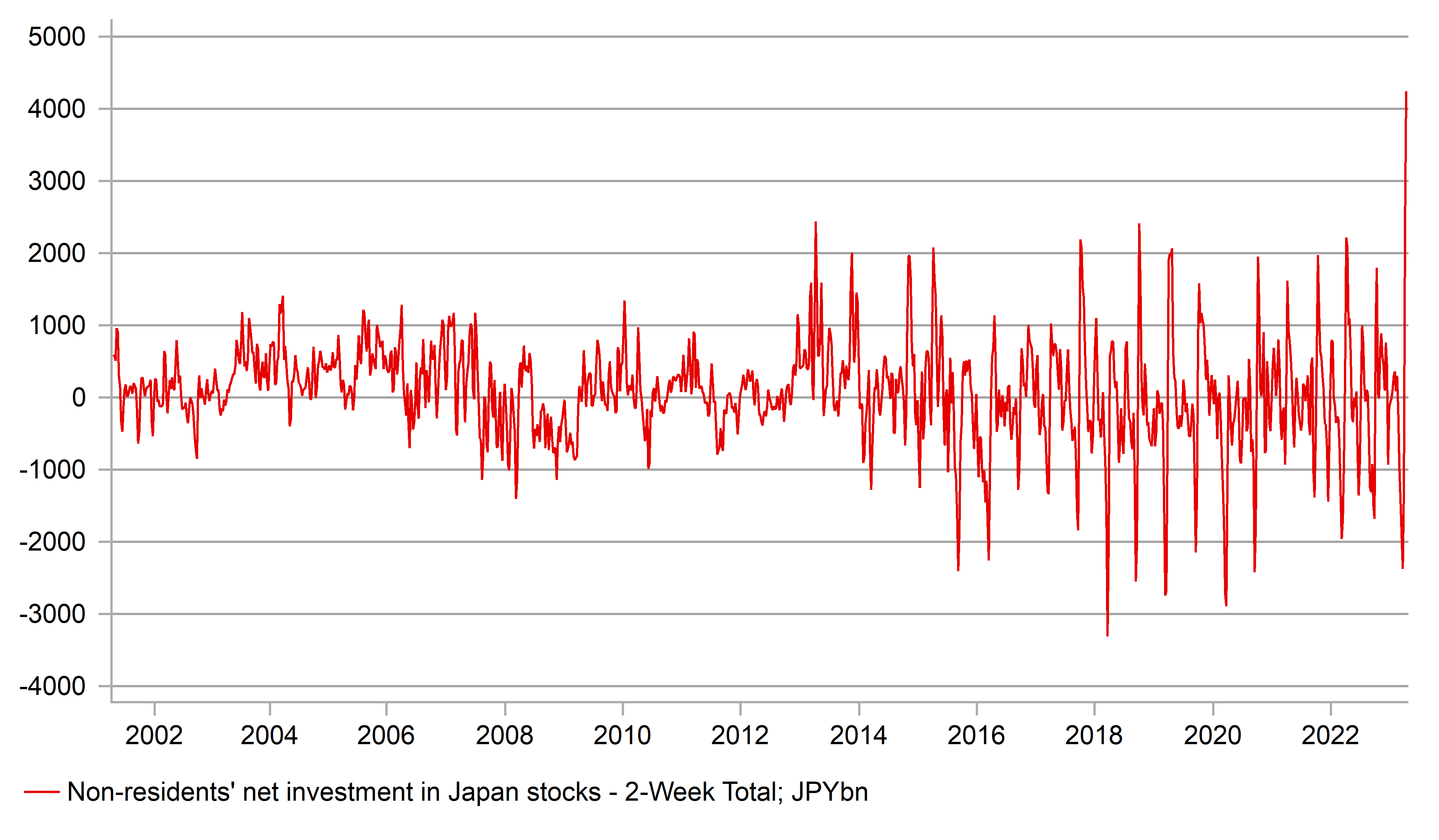

JPY: Record buying of Japan stocks

The weekly MoF cross-border flow data doesn’t get too much attention but the data released yesterday was certainly eye-popping! The data revealed exceptionally strong buying of Japan stocks by foreign investors – in the week to last Friday, purchases totalled JPY 1,876bn but followed even larger purchases the week before, totalling JPY 2,369bn. That previous week is a record in the data series back to 2001 and this week’s is the second largest total. The two-week combined purchase total was JPY 4,245bn.

Risk appetite has obviously improved of late but nonetheless, the scale of purchases is still a surprise. The Topix in USD terms has underperformed the S&P 500 but not by much; +5.4% versus 7.6%. Rates have softened a touch in Japan with expectations now for the BoJ to delay the timing of any change to YCC, possibly to beyond June if as many now expect, PM Kishida decides to call a snap election. Historically, the BoJ does not tend to make policy changes in the run-in to a general election. So the easing of policy tightening expectations coupled with the reduced fears of any further banking sector has helped drive demand for Japan stocks. The Topix Bank Index has rebounded from the March lows a little more than in the US or the UK.

Of course higher inflation in Japan would also be seen as a positive for Japan equities. Today, the nationwide CPI data was released and revealed stronger than expected underlying inflation. The core-core YoY rate accelerated from 3.5% to 3.8% in March, the highest level since 1981. In addition, the Tokyo Stock Exchange announced that member companies with a price-to-book ratio that falls consistently below one would be required to lay out plans to rectify the situation. This “naming-and-shaming” strategy could hasten companies to reform more quickly.

But equally important perhaps is the attractive costs for hedging currency exposure that could also be a draw for foreign investors. It pays handsomely to hedge JPY exposure and that would also imply that this significant two-week period of record equity purchases has had limited impact on JPY.

SURGE IN FOREIGN DEMAND FOR JAPAN STOCKS

Source: Macrobond

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

UK |

08:00 |

Retail Sales (MoM) |

Mar |

-0.5% |

1.2% |

!!! |

|

EC |

08:00 |

ECB's De Guindos Speaks |

-- |

-- |

-- |

!! |

|

FR |

08:15 |

French Manufacturing PMI |

Apr |

47.8 |

47.3 |

! |

|

FR |

08:15 |

French S&P Global Composite PMI |

Apr |

52.7 |

52.7 |

! |

|

FR |

08:15 |

French Services PMI |

Apr |

53.4 |

53.9 |

!! |

|

GE |

08:30 |

German Composite PMI |

Apr |

52.7 |

52.6 |

!! |

|

GE |

08:30 |

German Manufacturing PMI |

Apr |

45.7 |

44.7 |

!!! |

|

GE |

08:30 |

German Services PMI |

Apr |

53.3 |

53.7 |

!! |

|

EC |

09:00 |

Manufacturing PMI |

Apr |

48.0 |

47.3 |

!! |

|

EC |

09:00 |

S&P Global Composite PMI |

Apr |

53.7 |

53.7 |

!! |

|

EC |

09:00 |

Services PMI |

Apr |

54.5 |

55.0 |

!! |

|

UK |

09:30 |

Composite PMI |

-- |

52.6 |

52.2 |

!! |

|

UK |

09:30 |

Manufacturing PMI |

-- |

48.5 |

47.9 |

!! |

|

UK |

09:30 |

Services PMI |

-- |

53.0 |

52.9 |

!!! |

|

CA |

13:30 |

Core Retail Sales (MoM) |

Feb |

-0.1% |

0.9% |

!!! |

|

CA |

13:30 |

Retail Sales (MoM) |

Feb |

-0.6% |

1.4% |

!! |

|

US |

14:45 |

Manufacturing PMI |

Apr |

49.0 |

49.2 |

!! |

|

US |

14:45 |

S&P Global Composite PMI |

Apr |

52.8 |

52.3 |

!! |

|

US |

14:45 |

Services PMI |

Apr |

51.5 |

52.6 |

!! |

|

EC |

15:30 |

ECB's Elderson Speaks |

-- |

-- |

-- |

!! |

|

EC |

18:45 |

ECB's De Guindos Speaks |

-- |

-- |

-- |

!! |

|

US |

21:35 |

Fed Governor Cook Speaks |

-- |

-- |

-- |

! |

Source: Bloomberg